Home » Posts tagged 'trading'

Tag Archives: trading

#SVML Sovereign Metals LTD – Rio Tinto Shareholding and Issue of Shares

ISSUE OF SHARES

ISSUE OF SHARES

Sovereign Metals Limited (ASX: SVM, AIM: SVML, OTCQX: SVMLF) (Sovereign or the Company) advises that it has issued 2,326,880 fully paid ordinary shares (Shares) in the capital of the Company, comprising of 1,290,392 Shares issued to Rio Tinto Mining and Exploration Limited (Rio Tinto) and 1,036,488 Shares issued to SCP Resource Finance, as an advisory fee of 3% on the amount of Rio Tinto’s option investment in July 2024 (refer to Company announcement on 3 July 2024).

An application will be made for the Shares to be admitted to trading on AIM (Admission) and it is expected that Admission will become effective on or around 19 September 2024.

RIO TINTO INCREASES ITS SHAREHOLDING TO 19.9%

Following the exercise of its unlisted options on 3 July 2024, Rio Tinto has made an additional investment of A$690,360 in Sovereign through the issue of 1,290,392 Shares (Additional Shares) pursuant to Rio Tinto’s first right of refusal on equity issues. This is in accordance with the Investment Agreement between Rio Tinto and the Company dated 16 July 2023. Following the issue of Additional Shares today, Rio Tinto has increased its shareholding in Sovereign to 19.9%.

Total Voting Rights

For the purposes of the Financial Conduct Authority’s Disclosure Guidance and Transparency Rules (DTRs), following Admission of the Shares, Sovereign will have 599,879,879 Ordinary Shares in issue with voting rights attached. The figure of 599,879,879 may be used by shareholders in the Company as the denominator for the calculations by which they will determine if they are required to notify their interest in, or a change to their interest in the Company, under the ASX Listing Rules or the DTRs.

Following the issue of Shares, Sovereign has the following securities on issue:

· 599,879,879 fully paid ordinary shares;

· 9,460,000 unlisted performance rights subject to the “Definitive Feasibility Study Milestone” expiring on or before 31 October 2025;

· 3,600,000 unlisted performance rights subject to the “Grant of a Mining Licence Milestone” expiring on or before 31 March 2026; and

· 4,800,000 unlisted performance rights subject to the “Final Investment Decision Milestone” expiring on or before 30 June 2026.

Classification: 2.5 Total number of voting rights and capital

ENQUIRIES

|

Dylan Browne +61(8) 9322 6322 |

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Brokers |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

|

|

|

|

|

Berenberg |

+44 20 3207 7800 |

|

Matthew Armitt |

|

|

Jennifer Lee |

|

|

|

|

|

Buchanan |

+ 44 20 7466 5000 |

#FCM First Class Metals PLC – Admission of Shares

First Class Metals PLC (“First Class Metals” “FCM” or the “Company”), the UK listed metals exploration company seeking economic metal discoveries across its extensive Canadian Schreiber-Hemlo, Sunbeam and Zigzag land holdings, announces that in respect of the 16,373,674 new ordinary shares (“Shares”) issued since the Company’s IPO on 29 July 2022, no applications were made for the Shares to be admitted to trading. This is a result of the Company and its Directors being given incorrect information by its former financial adviser.

First Class Metals PLC (“First Class Metals” “FCM” or the “Company”), the UK listed metals exploration company seeking economic metal discoveries across its extensive Canadian Schreiber-Hemlo, Sunbeam and Zigzag land holdings, announces that in respect of the 16,373,674 new ordinary shares (“Shares”) issued since the Company’s IPO on 29 July 2022, no applications were made for the Shares to be admitted to trading. This is a result of the Company and its Directors being given incorrect information by its former financial adviser.

In order to correct this position, the Company will now commence applications for the Shares to be admitted to trading on the Official List of the Financial Conduct Authority (“FCA”) and to trading on the Main Market of the London Stock Exchange. To ensure compliance with the Prospectus Regulation Rules, the Shares will be admitted in four tranches as follows:

i) 13,134,411 Shares will be admitted to trading on or around 23 January 2024;

ii) 2,626,882 Shares will be admitted to trading on or around 26 January 2024;

iii) 525,376 Shares will be admitted to trading on or around 31 January 2024; and

iv) 87,005 Shares will be admitted to trading on or around 5 February 2024.

For the avoidance of doubt, the Company’s issued share capital remains 82,045,729 ordinary shares of 0.1p each, with one vote per share (and no such shares are held in treasury). The total number of voting rights is therefore 82,045,729 and this figure may be used by shareholders as the denominator for the calculations to determine if they have a notifiable interest in the share capital of the Company under the FCA’s Disclosure Guidance and Transparency Rules, or if such interest has changed.

For further information, please contact:

|

James Knowles, Executive Chairman |

07488 362641 |

|

|

Marc J Sale, CEO |

07711 093532 |

Novum Securities Limited

(Financial Adviser)

|

David Coffman/Dan Harris/George Duxberry Novum Securities Limited |

|

(0)20 7399 9400 |

First Class Metals PLC – Background

First Class Metals is focussed on exploration in Ontario, Canada which has a robust and thriving junior mineral exploration sector. Specifically, the Hemlo ‘camp’ is a proven world class address for gold /VMS exploration. This geological terrane has significant production, both base / precious metals and a prolific number of exploration projects and numerous prospector’s ‘showings’.

FCM currently holds 100% ownership of seven claim blocks covering over 180km² along a 150km strike of the Hemlo-Schreiber-Dayohessarah greenstone belt which also contains the >23M oz shear hosted Hemlo gold mine operated by Barrick Gold. Late last year FCM completed the option to purchase the historical high grade (gold) Sunbeam past producing mine.

The significant potential of the properties for precious, base and battery metals relate to: ‘nearology’ insomuch that all properties lie close to identified mineral anomalism, for example Palladium One’s RJ and Smoke Lake nickel projects are close to the FCM’s West Pickle Lake drill proven Ni-Cu project. This also demonstrates the second critical asset the properties hold: vector, anomalies, be they geological, geochemical, or geophysical that have demonstrated mineral potential extend on to FCM’s properties.

The inferred shear on the Esa property is being explored by neighbours both to the west and east where it crosses into their properties. Furthermore, the properties have not been extensively explored either historically or more contemporaneously. This is attributable to the overall lack of outcrop. However, modern exploration techniques are better able to ‘see through’ the ground cover and to identify anomalies.

GreenX Metals #GRX – ASX Trading Halt

![]() GreenX Metals Limited (ASX:GRX; LSE:GRX; WSE:GRX) (GreenX or the Company) advises, that today the Company requested an immediate voluntary trading halt in its shares on the Australian Securities Exchange (ASX), pending an announcement regarding a capital raising.

GreenX Metals Limited (ASX:GRX; LSE:GRX; WSE:GRX) (GreenX or the Company) advises, that today the Company requested an immediate voluntary trading halt in its shares on the Australian Securities Exchange (ASX), pending an announcement regarding a capital raising.

The Company has requested that the trading halt remain until the earlier of an announcement to the market regarding the above or the opening of trade on ASX on 14 July 2023.

Trading in the Company’s ordinary securities will continue to trade as normal on the London and Warsaw Stock Exchanges during this period.

For further information please contact:

Dylan Browne

Company Secretary

+61 8 9322 6322

#SVML Sovereign Metals Ltd – ASX Trading Halt Update

![]() Sovereign Metals Limited (ASX:SVM; AIM:SVML) (“Sovereign” or the “Company”) announced on 27 January 2023 that following movements in its share price on the Australian Securities Exchange (“ASX”)and a price query from ASX, the Company’s ordinary shares were placed in a trading halt on the ASX. The ASX has informed Sovereign that the trading halt has been lifted and trading of the Company’s ordinary shares has resumed on the ASX.

Sovereign Metals Limited (ASX:SVM; AIM:SVML) (“Sovereign” or the “Company”) announced on 27 January 2023 that following movements in its share price on the Australian Securities Exchange (“ASX”)and a price query from ASX, the Company’s ordinary shares were placed in a trading halt on the ASX. The ASX has informed Sovereign that the trading halt has been lifted and trading of the Company’s ordinary shares has resumed on the ASX.

The trading halt did not affect trading in the Company’s shares on the AIM market of the London Stock Exchange plc, where normal trade continued.

In response to the ASX price query dated 27 January 2023 regarding an increase in the Company’s share price and in the volume of trading securities, the Company noted that it is not aware of any information that has not been announced which, if known, could be an explanation for recent trading in the securities of the Company, however it does note that:

(a) On 26 January 2023, Mkango Resources Limited (AIM/TSX-V: MKA) (“Mkango”) announced the receipt of Environmental Social Health Impact Assessment (“ESHIA”) approval from the Malawi Environmental Protection Authority (“MEPA”) for their Songwe Hill Rare Earths Project. The approval of the ESHIA is a significant milestone in the Mining Development Agreement (“MDA”) approvals process as it is fundamental requirement for obtaining a mining licence in Malawi.

(b) On 7 December 2022, the Company announced that the Company is to demerge its standalone Graphite Projects (being the Nanzeka, Malingunde, Duwi and Mabuwa Projects) into a wholly owned subsidiary, NGX Limited (“Demerger”). The Company expects to publish a Notice of Meeting for the Demerger in the coming weeks.

(c) In September 2022, the Company completed a 6,865 metre, 438-hole air-core and push-tube infill mineral resource drilling program at Kasiya Rutile Project (“Kasiya”). The infill drilling results from this program are consistent with previous announced drilling results (refer to announcements dated 08/09/2022 and 26/10/2022) and are confirmatory of these previous infill results released to the market. An updated Kasiya Mineral Resource Estimate is targeted for completion in Q1 2023.

The final infill drill hole was completed on 16/09/2022. The final batch of infill drill hole samples was sent to Australian laboratories on 9/11/2022. The final batch of assay results was received by the Company on 8/12/2022 but as stated above the results from the program are consistent with previous announced drilling results.

In any event, the Company has released the infill assay results following a request from ASX (see announcement entitled ‘Kasiya Resource Infill Drilling Results’ dated 30 January 2023).

The Company has strict procedures to maintain confidentiality of assay results with two directors and two senior management employees only having access to drill results prior to announcement drafting and circulation to the board for final approval.

The Company expects that its shares will trade as normal on ASX from opening of trade on 31 January 2023. Trading will continue as normal on the AIM market.

ENQUIRIES

|

Dylan Browne +61(8) 9322 6322 |

|

Nominated Adviser on AIM |

|

|

RFC Ambrian |

|

|

Bhavesh Patel / Andrew Thomson |

+44 20 3440 6800 |

|

|

|

|

Joint Brokers |

|

|

Berenberg |

+44 20 3207 7800 |

|

Matthew Armitt |

|

|

Jennifer Lee |

|

|

|

|

|

Optiva Securities |

+44 20 3137 1902 |

|

Daniel Ingram |

|

|

Mariela Jaho |

|

|

Christian Dennis |

|

#SVML Sovereign Metals Ltd – ASX Trading Halt

Sovereign Metals Limited advises that the Company announced a voluntary trading halt to the Company’s securities on the Australian Securities Exchange (“ASX”), pending an announcement regarding a response to an ASX price query.

Sovereign Metals Limited advises that the Company announced a voluntary trading halt to the Company’s securities on the Australian Securities Exchange (“ASX”), pending an announcement regarding a response to an ASX price query.

The Company requested that the trading halt remain until the earlier of an announcement to the market regarding the above or the opening of trade on ASX on 31 January 2023.

The Company also notes the recent share price rise in the trading of its securities on AIM, and observes that on 26 January 2023, Mkango Resources Limited (AIM/TSX-V: MKA) (“Mkango”) announced the receipt of Environmental Social Health Impact Assessment (“ESHIA”) approval from the Malawi Environmental Protection Authority (“MEPA”) for their Songwe Hill Rare Earths Project. The approval of the ESHIA is a significant milestone in the Mining Development Agreement (“MDA”) approvals process as it is a fundamental requirement for obtaining a mining licence, and while not directly associated with Sovereign’s Kasiya Rutile Project (“Kasiya”) in Malawi, could be perceived as an encouraging regulatory sign.

The Company also notes that it intends to release infill drilling results at Kasiya shortly, which would be incorporated into the next iteration of Kasiya’s Mineral Resource Estimate, and the impending release of the Notice of Meeting for the demerger of its standalone graphite projects (see RNS dated 7 December 2022).

ENQUIRIES

|

Dylan Browne +61(8) 9322 6322 |

|

Nominated Adviser on AIM |

|

|

RFC Ambrian |

|

|

Bhavesh Patel / Andrew Thomson |

+44 20 3440 6800 |

|

|

|

|

Joint Brokers |

|

|

Berenberg |

+44 20 3207 7800 |

|

Matthew Armitt |

|

|

Jennifer Lee |

|

|

|

|

|

Optiva Securities |

+44 20 3137 1902 |

|

Daniel Ingram |

|

|

Mariela Jaho |

|

|

Christian Dennis |

|

#GRX GreenX Metals Limited – Quarterly Activities Report September 2022

![]() HIGHLIGHTS

HIGHLIGHTS

· GreenX continued with its exploration work program to acquire up to 80% of the ARC copper project in Greenland:

o ARC is a significant, large-scale project (5,774km2 license area) with historical exploration results and recent analysis indicative of an extensive mineral system with potential to host world-class copper deposits.

o In August 2022, laboratory XRF analysis of native copper samples from ARC showed high purity consistently over 99% copper. Analysis also confirmed the presence of silver in one sample, and no significant deleterious elements in any of the samples.

o Despite adverse weather and ice conditions in Greenland affecting access to ARC during 2022, a site visit was made and limited samples were collected. GreenX was able to deliver the key exploration equipment into Greenland which should result in better efficiencies in the next field season.

o Results for the 2022 site visit to be released in the coming weeks.

· International arbitration claims against the Republic of Poland under both the Energy Charter Treaty and the Australia-Poland Bilateral Investment Treaty continue at pace:

o Statement of Reply for ongoing arbitration against Poland has been filed with a revised claim for compensation in the amount of £737 million (A$1.3 billion/PLN 4.0 billion) as prepared by external quantum experts.

o Claim includes an updated assessment of the value of GreenX’s lost profits and damages related to both the Jan Karski and Debiensko mines, and accrued interest related to any damages.

o Following the lodgement of final substantive filings from both parties subsequent to the end of the quarter, the next step in the arbitration process is for the hearing to be conducted in front of the Tribunal.

o GreenX notes the recent success of AIM listed, Rockhopper Exploration plc’s Energy Charter Treaty claim against the Republic of Italy in relation to oil and gas licenses including a unanimous decision against the Republic of Italy to award €190 million in damages plus interest.

· Cash balance at 30 September 2022 of A$4.2 million to fund activities at ARC plus A$7.4 million available under the litigation funding facility to continue pursuing GreenX’s dispute against the Republic of Poland.

GreenX Metals Limited (ASX:GRX, LSE:GRX) (GreenX or the Company) is pleased to present its Quarterly Activities Report for the period during and subsequent to 30 September 2022.

LABORATORY ANALYSIS OF HISTORICAL SAMPLES FROM ARC CONFIRMS UP TO 99.8% PURE NATIVE COPPER

During the quarter, GreenX and its joint-venture (JV) partner Greenfields Exploration Ltd (Greenfields) announced the results of preliminary analysis on three historical samples of native copper nodules from the ARC Project (ARC or the Project) in Greenland. The samples were obtained from a recently opened government geological storage facility in Copenhagen. Three native copper samples found at Discovery Zone, Neergaard Dal, and Neergaard South within ARC were subject to advanced micro-XRF scanning, a more precise and comprehensive technology when compared to more common portable XRFs.

The best analysis result was for a sample found immediately south of the Discovery Zone, which indicated median copper purity of 99.8%, with 255 g/t silver, 0.004% antimony and 0.000% arsenic.

The samples from Neergard Dal and Neergard South indicated copper purity of 99.7% and 99.4% respectively, with low to no deleterious elements detected in any of the samples. The high quality of the analysed samples is comparable to blister copper, a product typically produced by smelting prior to being sent to a refinery.

The results of the micro-XRF analysis are supportive of the potential quality of the mineralisation at ARC and will inform future field programs which will incorporate geochemical sampling, portable core drilling, and geophysics at high-priority targets within ARC. The Discovery Zone, where the highest-purity analysed sample was recovered, is the highest priority exploration target.

Despite adverse weather and ice conditions in Greenland affecting access to ARC during 2022, a site visit was made and limited samples were collected. GreenX was able to deliver the key exploration equipment into Greenland which should result in better efficiencies in the next field season.

ABOUT ARC

ARC is an exploration joint venture between GreenX and Greenfields. GreenX can earn 80% of ARC by spending A$10 million by October 2026. ARC is targeting large scale copper in multiple settings across a 5,774 km2 Special Exploration Licence in eastern North Greenland. The area has been historically underexplored yet is prospective for copper, forming part of the newly identified Kiffaanngissuseq metallogenic province.

GreenX and GEX consider the observed geological setting and features of ARC to be indicative of an extensive mineral system capable of hosting world-class copper deposits. The large scale of the mineral system, widespread copper anomalism, combined with dual mineralising events are analogous to the largest copper systems known worldwide. Accordingly, GreenX considers that ARC has the potential to be a globally significant metallogenic province.

Historical field programs identified widespread copper-silver occurrences at surface:

· geochemical sampling found that 80% of stream sediment samples contain native copper

· native copper is found in situ or as float, with individual clasts of native copper weighing up to 1 kg+

· high grade copper sulphides, grading up to 2.15% Cu and 35.5g/t Ag over 4.5m true width, are known from trench sampling of fault zones within sediments (see GreenX announcement dated 20 January 2022 entitled “New Copper Targets Identified at ARC”)

· assay results from individual samples are much higher grade, including:

|

o 53.8% Cu and 2,480g/t Ag |

o 7.9% Cu and 53 g/t Ag |

|

o 20.7% Cu and 488g/t Ag |

o 5.3% Cu and 112 g/t Ag |

|

o 12.5% Cu and 385g/t Ag |

o 5.0% Cu and 304 g/t Ag |

|

o 9.0% Cu and 112 g/t Ag |

o 4.0% Cu and 82 g/t Ag |

Very high-grade copper mineralisation identified at ARC is associated with the Minik Anomaly, a coincident magnetic-electromagnetic-gravity feature in an area where there is a change in oxidation state and widespread native copper in stream sediments. These features are presented as the footprint of a large-scale hydrothermal system.

The frequency and size of the native copper clasts, and the high grade of the copper-silver sulphides that are exposed at the surface, bode well for the prospectivity of copper deposits and will be a will be a key focus of the first field campaign.

There are multiple targets and favourable geological settings considered to be prospective within the ARC project area, including the following.

· The highly anomalous basalt is a high priority target that has not previously been the focus of commercial exploration. These basalts are the source of the native copper.

· The sulphide mineralised faults passing through these basalts into the overlying sediments have been subject to first pass exploration and shown to be rich in copper and silver. The high-grade sulphides in these faults will be the focus of further exploration.

· The permeable coarse-grained sandstone within the Jyske Ås Fm has high grade copper that is effectively unexplored. This stratiform mineralisation adds the potential for significant lateral extension of the known mineralisation exposed in the faults of the Discovery Zone.

As such, the extensive ARC mineral system is known to be prospective for basalt, fault, and sedimentary rock-hosted (‘sediment-hosted’) mineralisation that despite the attractive grades, is virtually unexplored.

CORPORATE

Financial Position

As at 30 September 2022, GreenX had A$4.2 million to fund activities at ARC plus A$7.4 million available under the litigation funding facility to continue pursuing GreenX’s dispute against the Republic of Poland.

DISPUTE WITH POLISH GOVERNMENT

During the quarter, the Company reported that as part of the ongoing international arbitration claims (Claim) against the Republic of Poland under both the Energy Charter Treaty (ECT) and the Australia-Poland Bilateral Investment Treaty (BIT) (together the Treaties), GreenX had filed its Statement of Reply in the BIT arbitration.

This is the final material filing that GreenX has made for the BIT arbitration, with the next step in the arbitration process, following the lodgement of Poland’s Rejoinder, is for the hearing to be conducted in front of the Tribunal.

Based upon revised external expert reports in response to Poland’s Statement of Defence, GreenX is now seeking compensation in the amount of £737 million (equivalent to A$1.3 billion or PLN 4.0 billion).

Details of the Claim

The Company’s Claim against the Republic of Poland is being prosecuted through an established and enforceable legal framework, with GreenX and Poland agreeing to apply the United Nations Commission on International Trade Law Rules (UNCITRAL) rules to the proceedings.

The claim Tribunals have been constituted, with both Claims being registered with the Permanent Court of Arbitration in the Hague. The BIT and ECT claim proceedings proceed at pace, with the Company now having filed a revised claim for damages against Poland with the Tribunal in the amount of £737 million (A$1.3 billion/PLN4.0 billion), which includes damages related to both the Jan Karski and Debiensko projects, and accrued interest related to any damages. The Claim for damages has been assessed by external quantum experts appointed by GreenX specifically for the purposes of the Claim.

In July 2020, the Company announced it had executed a Litigation Funding Agreement (LFA) for US$12.3 million with Litigation Capital Management (LCM). The facility is currently being drawn down to cover legal, tribunal and external expert costs as well as defined operating expenses associated with the Claim. The LFA is a limited recourse loan with LCM that is on a “no win – no fee” basis.

In September 2020, GreenX announced that it had formally commenced with the Claim by serving the Notices of Arbitration against the Republic of Poland. In June 2021, GreenX announced that it had formally lodged its Statement of Claim in the BIT arbitration, including the first assessed claim for compensation. The Company’s Statement of Reply, the last significant filing to be made by the Company, has now been filed in both Arbitrations. The Statement of Reply addresses various points raised by the Republic of Poland in their Statement of Defence. The Statement of Reply also contains a re-evaluation of the claim for damages based on responses to Poland’s Statement of Defence.

GreenX’s dispute alleges that the Republic of Poland has breached its obligations under the applicable Treaties through its actions to block the development of the Company’s Jan Karski and Debiensko projects in Poland which effectively deprives GreenX of the entire value of its investments in Poland.

In February 2019, GreenX formally notified the Polish Government that there exists an investment dispute between GreenX and the Polish Government. GreenX’s notification called for prompt negotiations with the Government to amicably resolve the dispute and indicated GreenX’s right to submit the dispute to international arbitration in the event of the dispute not being resolved amicably. As of the date of this report, no amicable resolution of the dispute has occurred, since the Polish Government has declined to participate in discussions related to the dispute and accordingly the Company has formally proceeded with its Claim as discussed above.

GreenX’s investment dispute with the Republic of Poland is not unique, with international media widely reporting that the political environment and investment climate in Poland has deteriorated since the change in Government in 2015. As a result, there are a significant number of International Arbitration claims being bought against Poland.

Furthermore, GreenX notes the recent success of AIM listed Rockhopper Exploration plc’s (Rockhopper) ECT claim against the Republic of Italy in relation to oil and gas licenses.

On 24 August 2022, Rockhopper announced that an ECT arbitration panel had reached a unanimous decision against the Republic of Italy to award Rockhopper €190 million in damages plus interest at EURIBOR +4% compounded annually from 2016 until the time of payment.

All costs associated with the Rockhopper arbitration were funded on a non-recourse (“no win – no fee”) basis from a specialist arbitration funder, similar to GreenX’s litigation funding arrangements. After payments due to the arbitration funder, Rockhopper expects to retain approximately 80% of the award.

#SVML Sovereign Metals – ASX Trading Halt

![]()

Sovereign Metals Limited (ASX:SVM; AIM:SVML) (Sovereign or the Company) advises that today the Company requested an immediate voluntary trading halt in its shares on the Australian Securities Exchange (ASX), pending an announcement regarding a capital raising.

The Company has requested that the trading halt remain until the earlier of an announcement to the market regarding the above or the opening of trade on ASX on 2 May 2022.

Trading in the Company’s ordinary securities will continue to trade as normal on AIM during this period.

ENQUIRIES

|

Dr Julian Stephens (Perth) +61(8) 9322 6322 |

Sam Cordin (Perth) |

Sapan Ghai (London)

|

|

Nominated Adviser on AIM |

|

|

RFC Ambrian |

|

|

Bhavesh Patel / Andrew Thomson |

+44 20 3440 6800 |

|

|

|

|

Joint Brokers |

|

|

Berenberg |

+44 20 3207 7800 |

|

Matthew Armitt |

|

|

Jennifer Lee |

|

|

Varun Talwar |

|

|

|

|

|

Optiva Securities |

+44 20 3137 1902 |

|

Daniel Ingrams |

|

|

Mariela Jaho |

|

|

Christian Dennis |

|

Open Orphan #ORPH – Proposal to purchase Poolbeg Pharma shares from distribution in specie shareholders

Open Orphan (ORPH) a rapidly growing specialist contract research organisation (CRO) and world leader in testing infectious and respiratory disease products using human challenge clinical trials, notes the announcement dated 11 April 2022 from Poolbeg Pharma plc (“Poolbeg”), regarding a number of new investors (“New Investors”) having expressed interest in acquiring up to £1.6m of Poolbeg which are currently locked-up and held in trust by Croft Nominees Limited as a result of the distribution in specie from Open Orphan on 18 June 2021.

Open Orphan (ORPH) a rapidly growing specialist contract research organisation (CRO) and world leader in testing infectious and respiratory disease products using human challenge clinical trials, notes the announcement dated 11 April 2022 from Poolbeg Pharma plc (“Poolbeg”), regarding a number of new investors (“New Investors”) having expressed interest in acquiring up to £1.6m of Poolbeg which are currently locked-up and held in trust by Croft Nominees Limited as a result of the distribution in specie from Open Orphan on 18 June 2021.

As part of these proposals, the New Investors have committed to purchase up to £1.6m of the distribution in specie shares on or around 26 April 2022 at a price of 5.9 pence per share, the closing market price on Friday 8 April 2022. The New Investors have shown great interest in the Poolbeg story, its significant progress since IPO in July 2021, and its capabilities in developing novel products utilising its unique cost-effective model in the fast-growing infectious disease market which is expected to be worth in excess of $250bn by 2025. This is a clear vote of confidence in Poolbeg’s prospects as it enters an extremely exciting phase of its development with its first LPS human challenge clinical trial due to commence in June 2022 with multiple value inflection points expected in 2022 and beyond.

This process will allow the locked-up distribution in specie shareholders in Poolbeg the opportunity to sell part or all of their shareholding, should they wish to do so, prior to receiving the shares once the lock-up period ends on 20 April 2022. The distribution in specie shareholders will receive a letter setting out the New Investors’ proposal and a Form of Election informing them how to participate should they wish to sell some or all of their shares prior to the lock-up ending on 20 April 2022. These proposals are open to all distribution in specie shareholders but participation is at each distribution in specie shareholder’s discretion. For those shareholders who do not participate, the title to their distribution in specie shares will be transferred to them on or around 26 April 2022. If more than £1.6m is offered by way of valid Forms of Election, then the distribution in specie shareholders will be scaled back on a pro-rata basis.

The distribution in specie shares are exempt from income tax for UK resident shareholders due to the advance clearance obtained by the Company from HMRC for a statutory demerger. As such, there should be no UK income tax liabilities for UK resident shareholders on receipt of these shares. The only time that UK resident shareholder will be subject to tax on these shares will be in the event that the shareholder sells them, and in that event there will be a capital gains tax payment due on any chargeable gain. The base cost for capital gains calculation purposes will be 1% of the original cost base of the Open Orphan shares which will be close to nil (0), therefore nearly the full consideration will be subject to capital gains tax. The above comments are intended only as a general guide, shareholders are encouraged and recommended to seek their own financial and tax advice.

Open Orphan plc and Poolbeg Pharma plc ordinary shares are ISA qualifying investments. Open Orphan understands that any distribution in specie shares held in an ISA should be treated in a similar way to any other income generated from ISA qualifying investments.

A copy of the letter to distribution in specie shareholders can be found on Poolbeg’s website here and an FAQ is available here.

Cathal Friel, Executive Chairman of Open Orphan, said: “We were delighted to see that despite the presently turbulent market that Poolbeg has successfully managed to bring in fresh investors to purchase up to £1.6m at 5.9p, the market price on Friday 8 April 2022. The new investors have shown great interest in the Poolbeg story and its significant progress since IPO, its capabilities in developing novel infectious disease products utilising its unique cost-effective model. Poolbeg is well capitalised, with c. £20.9m at year end 2021, so importantly it is not raising any new funds as part of this process and, as such, there will be no dilution of existing shareholders.

“This arrangement has followed significant efforts to help widen the Poolbeg investor base and increase future liquidity, in order to ensure that the dividend in specie remains as beneficial as possible to shareholders of both Open Orphan and Poolbeg in the long-term.

“Due to the nature of the lock-up period, which was designed to allow for an orderly market following Poolbeg’s admission to AIM, prospective investors looking to build more substantial stakes were unable to do so. These proposals ensure that any potential shares sold will be going to quality, long-term holders, whilst giving distribution in specie shareholders the option to sell shares prior to the end of the lock-up period, if they choose to do so. In addition, there will be substantially greater liquidity in our shares once the distribution in specie shares have been distributed after 26 April 2022 and we believe this will certainly help us to attract in even more new shareholders.”

Footnote

The distribution in specie shares were issued to all Open Orphan shareholders on the share register at close of business on 17 June 2021, following this, Poolbeg successfully listed on the London Stock Exchange AIM market on 19 July 2021. While the underlying shareholders retain the beneficial ownership of the shares, the distribution in specie shares are currently held in trust by Croft during a lock-up period of nine calendar months from Poolbeg’s admission to AIM, to contribute to the creation of an orderly market. This lock-up period will end on 20 April 2022 and on or around 26 April 2022, shareholders will be sent a share certificate for the distribution in specie shares. Shareholders will then have the option to dematerialise and hold the shares via CREST. If any Open Orphan shares that gave rise to the entitlement to the distribution in specie shares are held in a nominee account, the share certificate will be sent to the shareholders’ broker.

The New Investors’ proposals are not open for participation by persons interested in shares who are residents or citizens of or who have an address in, or who otherwise appear to the Company or SLC Registrars to be connected to, the United States (or any of its territories or possessions), Canada, Australia, Japan, Belarus or Russia.

For further information please contact:

|

Open Orphan plc |

+353 (0) 1 644 0007 |

||

|

Cathal Friel, Executive Chairman Yamin Khan, Chief Executive Officer |

|||

|

Arden Partners plc (Nominated Adviser and Joint Broker) |

+44 (0) 20 7614 5900 |

||

|

John Llewellyn-Lloyd / Louisa Waddell |

|||

|

finnCap plc (Joint Broker) |

+44 (0) 20 7220 0500 |

||

|

Geoff Nash / James Thompson / Richard Chambers |

|||

|

Davy (Euronext Growth Adviser and Joint Broker) |

+353 (0) 1 679 6363 |

||

|

Anthony Farrell |

|||

|

Walbrook PR (Financial PR & IR) Paul McManus / Sam Allen / Louis Ashe-Jepson |

+44 (0)20 7933 8780 or openorphan@walbrookpr.com +44 (0)7980 541 893 / +44 (0) 7502 558 258 / +44 (0) 7747 515393 |

||

Notes to Editors

Open Orphan plc

Open Orphan plc (London and Euronext: ORPH) is a rapidly growing contract research company that is a world leader in testing infectious and respiratory disease products using human challenge clinical trials. The Company provides services to Big Pharma, biotech, and government/public health organisations.

The Company has a leading portfolio of human challenge study models for infectious and respiratory diseases, including the recently established COVID-19 model, and is developing a number of new models, such as Malaria, to address the dramatic growth of the global infectious disease market. The Paris and Breda offices have over 25 years of experience providing drug development services such as biometry, data management, statistics CMC, PK and medical writing to third party clients as well as supporting the London-based challenge studies.

Open Orphan runs challenge studies in London from its Whitechapel quarantine clinic, its state-of-the-art QMB clinic with its highly specialised on-site virology and immunology laboratory, and its newly opened clinic in Plumbers Row. To recruit volunteers / patients for its studies, the Company leverages its unique clinical trial recruitment capacity via its FluCamp volunteer screening facilities in London and Manchester. The newly opened facilities have expanded the scope of the business to enable the offering of Phase I and Phase II vaccine field trials, PK studies, bridging studies, and patient trials as part of large international multi-centre studies.

Building upon its many years of challenge studies and virology research, the Company is developing an in-depth database of infectious disease progression data. Based on the Company’s Disease in Motion® platform, this unique dataset includes clinical, immunological, virological, and digital (wearable) biomarkers.

About Poolbeg Pharma

Poolbeg Pharma is a clinical stage infectious disease pharmaceutical company, with a capital light clinical model which aims to develop multiple products faster and more cost effectively than the conventional biotech model. The Company, headquartered in London, is led by a team with a track record of creation and delivery of shareholder value and aspires to become a “one-stop shop” for Big Pharma seeking mid-stage products to license or acquire.

The Company is targeting the growing infectious disease market. In the wake of the COVID-19 pandemic, infectious disease has become one of the fastest growing pharma markets and is expected to exceed $250bn by 2025.

With its initial assets from Open Orphan plc , an industry leading infectious disease and human challenge trials business, Poolbeg has access to knowledge, experience, and clinical data from over 20 years of human challenge trials. The Company is using these insights to acquire new assets as well as reposition clinical stage products, reducing spend and risk. Amongst its portfolio of exciting assets, Poolbeg has a small molecule immunomodulator for severe influenza (POLB 001); a first-in-class, intranasally administered RNA-based immunotherapy for respiratory virus infections (POLB 002); and a vaccine for Melioidosis (POLB 003). The Company is also developing an oral vaccine delivery platform and is progressing two artificial intelligence (AI) drug discovery programmes to accelerate the power of its human challenge model data and biobank.

For more information, please go to www.poolbegpharma.com or follow us @PoolbegPharma

#ORPH Open Orphan – Open Orphan plc distribution in specie of Poolbeg Pharma plc shares – FAQ

When will I receive my share certificate?

The Poolbeg Pharma shares received are subject to a lock-up period that ends on 19 April 2022. Within 14 days of that date, shareholders will be sent a certificate for their distribution in specie shares. Shareholders will then have the option to dematerialise the shares and hold via CREST.

If your Open Orphan plc shares that gave rise to the entitlement to the distribution in specie shares are held in a nominee account, the share certificate will be sent to your broker who can add these to your account.

There has been some confusion among some investors enquiring whether these locked-up distribution in specie shares can currently be traded. Please note that these shares cannot yet be traded because they have not yet been transferred from the nominee (Croft Nominees Ltd) where they are being held in trust during the lock-up period. After the end of the lock-up period when the shares have been transferred, they will then be fully tradeable like any other public company share.

Why aren’t the shares in my online trading account?

As explained above, during the lock-up period the legal title to the shares are held by Croft Nominees Limited. The underlying shareholders retain the beneficial ownership of the shares. Shareholders with online trading accounts should see their future entitlement on their online platform but they cannot be traded and will show no value until after the end of the lock-up period when the shares will be transferred.

Therefore, as per above, you cannot trade shares that you are not yet in receipt of, but after the end of the lock-up period when the shares have been transferred, they will be fully tradeable like any other public company share.

Who are Croft Nominees Limited?

Croft Nominees Limited, is an entity controlled by the lawyers to Open Orphan and Poolbeg Pharma, DAC Beachcroft. DAC Beachcroft were appointed by Open Orphan and Poolbeg Pharma to act as custodian for the nine-month post IPO lock-up of Poolbeg Pharma shares. This appointment is to help facilitate the practical enforcement of the lock-up restrictions.

Within 14 days post the end of the lock-up, Croft Nominees will no longer hold any of these shares, as their sole function was to act as a holding nominee which is standard practice in these types of transactions.

Why is there a lock-up period?

The lock-up period is intended to contribute to the creation of an orderly market for a period after Poolbeg Pharma’s admission to trading on AIM. Poolbeg Pharma’s admission to AIM took place on 19 July 2021. Such lock-up periods can vary from 3, 6, 9, or 12 months in length and the Company took the decision to lock-up shareholders for a 9-month period.

Will there be tax on the distribution in specie shares?

The following comments are intended only as a general guide, shareholders are encouraged and recommended to seek their own financial tax advice.

A. UK resident shareholders: The distribution in specie shares issued to shareholders as part of the demerger from Open Orphan are treated as a distribution for UK tax purposes, which could be taxable as dividend income. However, as advance clearance for a statutory demerger was obtained from HMRC, the distribution is exempt for UK income tax purposes, and hence there should be no UK income tax liabilities for UK resident shareholders upon receipt of these distribution in specie shares.

Disposal of the distribution in specie shares by UK resident shareholders will be subject to capital gains tax if a chargeable gain is made. The capital gains tax base cost is close to nil (0), therefore nearly the full consideration will be subject to capital gains tax.

There has been some confusion around the base cost and some shareholders thought that the base cost for these shares might be 6p, however, we can clarify that the base cost for capital gains purposes is close to nil because no consideration was paid for the receipt of these shares.

B. UK resident shareholders with shares held in an ISA:

Open Orphan plc and Poolbeg Pharma plc ordinary shares are ISA qualifying investments.

The Company can confirm based on advice received that if a shareholder held Open Orphan plc shares in an ISA account on the ex-dividend date (17 June 2021), the resulting Poolbeg Pharma distribution in specie shares should be directed to and held in your ISA account after 19 April 2022 when they are released from lock-up. This dividend income received into your ISA is treated the same way as any other exempt income that was generated from your ISA qualifying investment.

As with all ISA held shares, should you sell your dividend in specie Poolbeg shares, there will be no tax payable if the proceeds remain within your ISA account.

In addition, if these distribution in specie Poolbeg shares remain within the ISA, they do not form part of the £20k annual ISA allowance as they result from a distribution from an existing ISA shareholding.

We fully understand that there had been some confusion among some of our investors and also potentially among some of the ISA online account managers, but we can confirm that shareholders should have no issue retaining Poolbeg Pharma dividend in specie shares within a qualifying ISA account.

C. Ireland resident shareholders: Advice has been obtained from professional advisors in Ireland who have confirmed that there should be no Irish income tax liabilities as a result of the issue of the distribution in specie shares as part of the demerger. The receipt of dividends could be subject to Irish income tax, and independent advice should be sought.

Disposal of the distribution in specie shares by Irish resident shareholders will be subject to capital gains tax if a chargeable gain is made. The capital gains tax base cost is close to nil, therefore nearly the full consideration will be subject to capital gains tax. There has been some confusion around the base cost and some shareholders thought that the base cost for these shares might be 6p, however, we can clarify that the base cost for capital gains purposes is close to nil because no consideration was paid for the receipt of these shares.

D. Non-UK and Non-Irish resident shareholders: May be subject to tax on dividend income under any law to which they are subject to outside the UK. In addition, they may be subject to tax on a future disposal of shares under any law to which they are subject to outside the UK. Such shareholders should consult their own tax advisers concerning their tax liabilities.

What is the base cost for tax purposes if distribution in speice Poolbeg Pharma shares which are not held in an ISA?

If a UK resident shareholder sells their Poolbeg Pharma distribution in specie shares there will be capital gains tax payable, however as stated above, there will be no income tax due on receipt on these shares. The base cost for capital gains calculation purposes will close to nil (0), therefore nearly the full consideration will be subject to capital gains tax.

There has been some confusion around the base cost and some shareholders thought that the base cost for these shares might be 6p, however, we can clarify that the base cost for capital gains purposes is close to nil because no consideration was paid for the receipt of these shares.

Please note, no capital gains or other tax will be due until the taxpayer sells the Poolbeg Pharma shares in the first instance.

How does general meeting voting work for distribution in speice shareholders?

Poolbeg Pharma and Croft Nominees Limited have organised for distribution in specie shareholders to vote in its upcoming AGM via Poolbeg Pharma’s share registrars, SLC Registrars Limited. Shareholders have been sent a Form of Direction to vote which should be returned to the registrars. This document and all other documents relating to the AGM can be found here: https://www.poolbegpharma.com/investors/documents/

How many shares are received for holdings in Open Orphan?

Open Orphan shareholders who were on the register at close of business on 17 June 2021 were allocated shares using a ratio of 1 Poolbeg Pharma share for every 2.98 ordinary shares held in Open Orphan.

What is the ongoing relationship between Open Orphan and Poolbeg Pharma?

Open Orphan and Poolbeg Pharma are non associated companies that are run independently of each other, both are listed on the AIM market of the London Stock Exchange with independent boards and management teams. There is a number of cost synergies including shared office space and shared staff costs.

For further information, please read the following demerger update announced by Open Orphan on 17 June 2021:

https://www.investegate.co.uk/open-orphan-plc–orph-/rns/demerger-update/202106170700091713C/

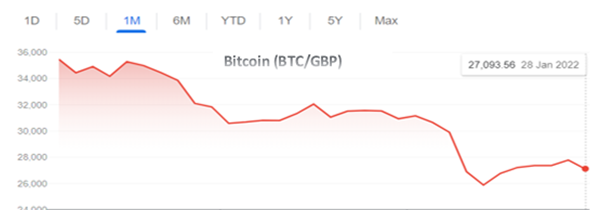

Is the hype finally over for Bitcoin, Altcoins and NFTs?

By Arjun Thakkar and Alan Green

Crypto volatility is back…and then some! Some investors called it downtrend others call it a cryptocurrency reset. The recent cryptocurrency crash wiped out nearly $1 trillion of wealth; Bitcoin fell by 30% while Ethereum dropped by 45% between Dec 2021 – Jan 2022. Although data shows 70% of crypto investors joined the market in 2021, the question everyone is asking is whether crypto market dilution and the uninitiated selling out is the reason for the downtrend, or rathermore is it due to new and better Initial Coin Offerings (ICOs) offering better value? It could of course be nothing more than a normal market correction? Let’s discover!

Theoretically, there is an inverse relationship between interest rates and the prices of opportunity costs such as stock prices, commodity prices and crypto valuation. Moves by central banks such as the Federal Reserve and Bank of England over the past few weeks have had a major influence on the financial markets. We now know that Russia is considering a ban on cryptocurrency and China has announced fresh regulations that include the banning of mining, a massive clamp down on ICOs, all of which has contributed to the huge sell-off.

Despite the fact that monetary policies and interest rates will affect prices in the short-term, the manner in which blockchain or cryptocurrency will be utilized in the future will largely determine its longevity and relevance. Financial institutions such as JP Morgan have started using blockchain technology for the security, speed and privacy of end-to-end transactions. It is already widely accepted that blockchain can be used to verify documents and speed up process with the help of smart contracts in industries like real estate or insurance.

Put simply blockchain and crypto currencies are here to stay. Governments and sovereignties including El Salvador have already adopted Bitcoin as legal tender, so the gradual recognition and acceptance of blockchain and cryptocurrency as legal tender seems almost inevitable despite the recent moves by the Chinese government and the Russian central bank to enforce regulations. But even the latest developments in Russia suggest that President Vladimir Putin and the Russian Finance ministry have changed tack and backed blockchain and crypto mining, albeit with measures to tax and regulate the crypto mining industry.

Altcoins

Despite the recent price correction and downturn affecting all cryptocurrencies, our view is that this is little more than a systemic risk and ‘healthy’ market correction. It is worth considering the individual performances (pre correction) of many altcoins such as Solana and Cardano, which have blasted onto the scene giving higher returns than well-known cryptos like Bitcoin and Ethereum. This despite both Solana and Cardano being built on Ethereum and relying on the Ethereum Blockchain to function.

The rising popularity of these altcoins is due to their improved functionality and their ability to facilitate smart contracts and host decentralized applications at a lower cost than giant rivals like Ethereum. Not only do they offer lower transaction costs but altcoins like Solana are faster and can handle around 50,000 more transactions per second.

Although Solana, Cardano and Ethereum can be used to deliver smart contracts, there are still questions over Bitcoin’s use and functionality going forward? Currently the primary purpose of Bitcoin is to facilitate the transfer of funds via a secure network, although it is worth noting that companies like Coinsilium (AQSE: COIN) (OTCQB: CINGF), are engaged in partnerships to build a Bitcoin marketplace for NFTs and to enable transition of RSK blockchain standard NFTs to other blockchain standard NFTs including Ethereum.

NFTs

Another burgeoning sector in the crypto and blockchain space is of course Non-Fungible Tokens (NFTs). These were hugely popular a few months back, and some were created by celebrities including William Shatner, Leonardo Messi and Justin Bieber. It does seem at the moment that some of the initial hype has waned so the question remains; are NFTs still a relevant asset class or were they just a flash in the pan?

Our belief is that although interest has waned in the short term, this has largely come about as a result of other major global events and developments taking centre stage as already outlined. Omicron, followed by a stock market and crypto market crash in January 2022 due to Russia and China moves against crypto currency have seen many less experienced investors sell up and get out. These events may have combined to move focus away from the NFT hype in the short term, but we believe longer term the hype and demand for NFTs will return. The size of the NFT market passed $40 billion in 2021 and is expected to double by 2025.

Our belief is that although interest has waned in the short term, this has largely come about as a result of other major global events and developments taking centre stage as already outlined. Omicron, followed by a stock market and crypto market crash in January 2022 due to Russia and China moves against crypto currency have seen many less experienced investors sell up and get out. These events may have combined to move focus away from the NFT hype in the short term, but we believe longer term the hype and demand for NFTs will return. The size of the NFT market passed $40 billion in 2021 and is expected to double by 2025.

And NFTs are still catching the headlines too. Celebrities Kevin Hart and Paris Hilton recently bought a Bored Ape Yacht Club NFT for over $300,000.

Apart from the traditional use of NFTs as a form of art, they also offer the potential to buy digital lands in virtual worlds like the metaverse, and the potential to license and publish music ownership. Interest and hype may ebb and flow, but NFTs are definitely here to stay.

Stick or Twist

In summary, we believe that while the sharp price movements in cryptocurrency will continue, altcoins like Solana and Cardano with their higher transaction speeds and lower gas fees offer great potential from here on. Alternative uses for Bitcoin – the king of crypto, such as a Bitcoin marketplace for NFTs adds a new dimension and functionality to the original cryptocurrency and a potential target price of $100k in a couple of years.

All in all, for investors able to cope with the sharp price movements, investing into Bitcoin, Altcoins and NFTs looks likely to deliver an increase in portfolio value over the longer term, and always the potential to deliver spectacular quick gains for short term traders. In pontoon parlance – Twist!