Home » Posts tagged 'stock market' (Page 4)

Tag Archives: stock market

ECR Minerals #ECR – Adam Jones and Alan Green talk through the upcoming Blue Moon Drilling Campaign

Adam Jones and Alan Green discuss the upcoming Blue Moon drilling campaign. We discuss the intriguing and unique style of mineralisation at Blue Moon, and the impressive grades and widths from the previous 2019 campaign assay results. Adam explains the previous soil geochemistry work undertaken at Blue Moon prior to the previous drilling campaign, before we discuss the upcoming campaign in a few weeks, with a four initial drill holes planned using ECR’s own MIDAS drill rig.

#ECR ECR Minerals – Holding(s) in Company

![]()

TR-1: Standard form for notification of major holdings

|

NOTIFICATION OF MAJOR HOLDINGS (to be sent to the relevant issuer and to the FCA in Microsoft Word format if possible)i |

||||||

|

|

||||||

|

1a. Identity of the issuer or the underlying issuer of existing shares to which voting rights are attached ii : |

ECR Minerals Plc |

|||||

|

1b. Please indicate if the issuer is a non-UK issuer (please mark with an “X” if appropriate) |

||||||

|

Non-UK issuer |

|

|||||

|

2. Reason for the notification (please mark the appropriate box or boxes with an “X”) |

||||||

|

An acquisition or disposal of voting rights |

X |

|||||

|

An acquisition or disposal of financial instruments |

|

|||||

|

An event changing the breakdown of voting rights |

|

|||||

|

Other (please specify)iii: |

|

|||||

|

3. Details of person subject to the notification obligation iv |

||||||

|

Name |

Colin Braidwood |

|||||

|

City and country of registered office (if applicable) |

|

|||||

|

4. Full name of shareholder(s) (if different from 3.)v |

||||||

|

Name |

Colin Braidwood |

|||||

|

City and country of registered office (if applicable) |

|

|||||

|

5. Date on which the threshold was crossed or reached vi : |

08/06/2022 |

|||||

|

6. Date on which issuer notified (DD/MM/YYYY): |

08/06/2022 |

|||||

|

7. Total positions of person(s) subject to the notification obligation |

||||||

|

|

% of voting rights attached to shares (total of 8. A) |

% of voting rights through financial instruments |

Total of both in % (8.A + 8.B) |

Total number of voting rights of issuervii |

||

|

Resulting situation on the date on which threshold was crossed or reached |

9.33% |

N/A |

9.33% |

1,064,464,551 |

||

|

Position of previous notification (if applicable) |

8.00% |

N/A |

8.00% |

1,018,058,551 |

||

|

8. Notified details of the resulting situation on the date on which the threshold was crossed or reached viii |

|||||||||

|

A: Voting rights attached to shares |

|||||||||

|

Class/type of ISIN code (if possible) |

Number of voting rights ix |

% of voting rights |

|||||||

|

Direct (Art 9 of Directive 2004/109/EC) (DTR5.1) |

Indirect (Art 10 of Directive 2004/109/EC) (DTR5.2.1) |

Direct (Art 9 of Directive 2004/109/EC) (DTR5.1) |

Indirect (Art 10 of Directive 2004/109/EC) (DTR5.2.1) |

||||||

|

GB00BYYDKX57 |

99,325,751 |

|

9.33% |

|

|||||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||

|

SUBTOTAL 8. A |

99,325,751 |

9.33% |

|||||||

|

|

|||||||||

|

B 1: Financial Instruments according to Art. 13(1)(a) of Directive 2004/109/EC (DTR5.3.1.1 (a)) |

|||||||||

|

Type of financial instrument |

Expiration |

Exercise/ |

Number of voting rights that may be acquired if the instrument is exercised/converted. |

% of voting rights |

|||||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||

|

|

|

SUBTOTAL 8. B 1 |

|

|

|||||

|

|

|||||||||

|

B 2: Financial Instruments with similar economic effect according to Art. 13(1)(b) of Directive 2004/109/EC (DTR5.3.1.1 (b)) |

|||||||||

|

Type of financial instrument |

Expiration |

Exercise/ |

Physical or cash settlement xii |

Number of voting rights |

% of voting rights |

||||

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||

|

|

|

|

SUBTOTAL 8.B.2 |

|

|

||||

|

|

|||||||||

|

9. Information in relation to the person subject to the notification obligation (please mark the applicable box with an “X”) |

||||

|

Person subject to the notification obligation is not controlled by any natural person or legal entity and does not control any other undertaking(s) holding directly or indirectly an interest in the (underlying) issuerxiii |

|

|||

|

Full chain of controlled undertakings through which the voting rights and/or the |

|

|||

|

Name xv |

% of voting rights if it equals or is higher than the notifiable threshold |

% of voting rights through financial instruments if it equals or is higher than the notifiable threshold |

Total of both if it equals or is higher than the notifiable threshold |

|

|

Colin Braidwood |

9.33% |

N/A |

9.33% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

10. In case of proxy voting, please identify: |

||||

|

Name of the proxy holder |

|

|||

|

The number and % of voting rights held |

|

|||

|

The date until which the voting rights will be held |

|

|||

|

|

||||

|

11. Additional information xvi |

||||

|

|

||||

|

Place of completion |

United Kingdom |

|

Date of completion |

08 June 2022

|

|

Annex: Notification of major holdings (to be filed with the FCA only) |

||

|

|

||

|

A: Identity of the person subject to the notification obligation |

||

|

Full name (including legal form for legal entities) |

|

|

|

Contact address (registered office for legal entities) |

|

|

|

|

|

|

|

Phone number / Fax number |

|

|

|

Other useful information (at least legal representative for legal persons) |

|

|

|

|

|

|

|

B: Identity of the notifier, if applicable |

||

|

Full name |

|

|

|

Contact address |

|

|

|

|

|

|

|

Phone number / Fax number |

|

|

|

Other useful information (e.g. functional relationship with the person or legal entity subject to the notification obligation) |

|

|

|

|

||

|

C: Additional information |

||

|

|

||

Please send the completed form together with this annex to the FCA at the following email

address: Majorshareholdings@fca.org.uk. Please send in Microsoft Word format if possible.

#ECR ECR Minerals – Holding(s) in Company

![]()

TR-1: Standard form for notification of major holdings

|

NOTIFICATION OF MAJOR HOLDINGS (to be sent to the relevant issuer and to the FCA in Microsoft Word format if possible)i |

||||||

|

|

||||||

|

1a. Identity of the issuer or the underlying issuer of existing shares to which voting rights are attached ii : |

ECR Minerals Plc |

|||||

|

1b. Please indicate if the issuer is a non-UK issuer (please mark with an “X” if appropriate) |

||||||

|

Non-UK issuer |

|

|||||

|

2. Reason for the notification (please mark the appropriate box or boxes with an “X”) |

||||||

|

An acquisition or disposal of voting rights |

X |

|||||

|

An acquisition or disposal of financial instruments |

|

|||||

|

An event changing the breakdown of voting rights |

|

|||||

|

Other (please specify)iii: |

|

|||||

|

3. Details of person subject to the notification obligation iv |

||||||

|

Name |

Colin Braidwood |

|||||

|

City and country of registered office (if applicable) |

|

|||||

|

4. Full name of shareholder(s) (if different from 3.)v |

||||||

|

Name |

Colin Braidwood |

|||||

|

City and country of registered office (if applicable) |

|

|||||

|

5. Date on which the threshold was crossed or reached vi : |

11/01/2022 |

|||||

|

6. Date on which issuer notified (DD/MM/YYYY): |

11/01/2022 |

|||||

|

7. Total positions of person(s) subject to the notification obligation |

||||||

|

|

% of voting rights attached to shares (total of 8. A) |

% of voting rights through financial instruments |

Total of both in % (8.A + 8.B) |

Total number of voting rights of issuervii |

||

|

Resulting situation on the date on which threshold was crossed or reached |

8.00% |

N/A |

8.00% |

1,018,058,551 |

||

|

Position of previous notification (if applicable) |

7.02% |

N/A |

7.02% |

1,018,058,551 |

||

|

8. Notified details of the resulting situation on the date on which the threshold was crossed or reached viii |

|||||||||

|

A: Voting rights attached to shares |

|||||||||

|

Class/type of ISIN code (if possible) |

Number of voting rights ix |

% of voting rights |

|||||||

|

Direct (Art 9 of Directive 2004/109/EC) (DTR5.1) |

Indirect (Art 10 of Directive 2004/109/EC) (DTR5.2.1) |

Direct (Art 9 of Directive 2004/109/EC) (DTR5.1) |

Indirect (Art 10 of Directive 2004/109/EC) (DTR5.2.1) |

||||||

|

GB00BYYDKX57 |

81,515,151 |

|

8.00% |

|

|||||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||

|

SUBTOTAL 8. A |

81,515,151 |

8.00% |

|||||||

|

|

|||||||||

|

B 1: Financial Instruments according to Art. 13(1)(a) of Directive 2004/109/EC (DTR5.3.1.1 (a)) |

|||||||||

|

Type of financial instrument |

Expiration |

Exercise/ |

Number of voting rights that may be acquired if the instrument is exercised/converted. |

% of voting rights |

|||||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||

|

|

|

SUBTOTAL 8. B 1 |

|

|

|||||

|

|

|||||||||

|

B 2: Financial Instruments with similar economic effect according to Art. 13(1)(b) of Directive 2004/109/EC (DTR5.3.1.1 (b)) |

|||||||||

|

Type of financial instrument |

Expiration |

Exercise/ |

Physical or cash settlement xii |

Number of voting rights |

% of voting rights |

||||

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||

|

|

|

|

SUBTOTAL 8.B.2 |

|

|

||||

|

|

|||||||||

|

9. Information in relation to the person subject to the notification obligation (please mark the applicable box with an “X”) |

||||

|

Person subject to the notification obligation is not controlled by any natural person or legal entity and does not control any other undertaking(s) holding directly or indirectly an interest in the (underlying) issuerxiii |

|

|||

|

Full chain of controlled undertakings through which the voting rights and/or the |

|

|||

|

Name xv |

% of voting rights if it equals or is higher than the notifiable threshold |

% of voting rights through financial instruments if it equals or is higher than the notifiable threshold |

Total of both if it equals or is higher than the notifiable threshold |

|

|

Colin Braidwood |

8.00% |

N/A |

8.00% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

10. In case of proxy voting, please identify: |

||||

|

Name of the proxy holder |

|

|||

|

The number and % of voting rights held |

|

|||

|

The date until which the voting rights will be held |

|

|||

|

|

||||

|

11. Additional information xvi |

||||

|

|

||||

|

Place of completion |

United Kingdom |

|

Date of completion |

11 January 2022

|

|

Annex: Notification of major holdings (to be filed with the FCA only) |

||

|

|

||

|

A: Identity of the person subject to the notification obligation |

||

|

Full name (including legal form for legal entities) |

|

|

|

Contact address (registered office for legal entities) |

|

|

|

|

|

|

|

Phone number / Fax number |

|

|

|

Other useful information (at least legal representative for legal persons) |

|

|

|

|

|

|

|

B: Identity of the notifier, if applicable |

||

|

Full name |

|

|

|

Contact address |

|

|

|

|

|

|

|

Phone number / Fax number |

|

|

|

Other useful information (e.g. functional relationship with the person or legal entity subject to the notification obligation) |

|

|

|

|

||

|

C: Additional information |

||

|

|

||

Please send the completed form together with this annex to the FCA at the following email

‘Crypto and Black Gold – Higher the Risk, Higher the Reward’

By Arjun Thakkar and Alan Green

Bitcoin worth more than $200bn was wiped off the crypto market on 12th of May. The crash in the BTC price accompanied a generally volatile and uncertain stock market that has seen the Dow Jones and FTSE100 down by 12.7% and 3.7% respectively from the start of the year. The core principle of the markets has always been higher the risk, higher the reward, but the current downward spiral seems to be driven by a perfect storm of events. Is this therefore the end of a bullish run for assets and the risk is too high now for any reward, or are we just seeing a major correction?

The key uncertainty spooking the markets are the high inflation rates. These are being driven by a number of factors, including supply chain problems from China, the Russia-Ukraine war and consequential 25% hike in the price of wheat. Interest rate hikes from the Fed and BoE are pushing borrowing costs higher and driving a sell-off in markets and crypto.

In these uncertain markets investors look for safe investments and the increase in interest rates in 2022 by 0.5% and 0.75% by the BoE and Fed respectively have made cash savings more attractive, leading to a massive sell off in stocks. Added to this, the hitherto stellar performances from crypto assets such as BTC and ETH have prompted well-heeled crypto investors to take their money off the table, further driving the down turn in crypto market valuations.

Supply chain issues continue to act as a drag. China accounts for around 13% of the global trade, and China’s zero tolerance approach towards Covid has led to a lockdown in the country, which has partly resulted in huge levels of shipping congestion near the Chinese ports. Companies such as Tesla have lost about a month of work because of the Shanghai lockdown, and some other companies claim that an “abnormally high” level of inventory was in transit, unavailable or held at ports, sending the stock market into a frenzy. (Bloomberg, 2022)

Image: World Bank

Along with the supply chain crisis, the Russia-Ukraine war has played a significant part in the fortunes of both stock and crypto markets. Russia previously supplied the European continent with 40% of its natural gas and 25% of its oil. The subsequent sanctions and ban on Russian imports sent the price of oil soaring to $109/barrel, driving inflation, and while some of the oil majors and smaller listed oilco’s are now trading at multi year highs, the uncertainty has weighed heavily on the markets.

The impact of higher oil prices has also impacted positively on companies at the junior end of the market. Echo Energy (AIM: ECHO) which has a license portfolio of 12 producing oil and gas fields with infrastructure in Santa Cruz Sur region of Argentina, found itself in the midst of this global demand for oil. Since the start of the Russia-Ukraine war (24th February 2022), Echo Energy shares have risen by 13.1% and at one point (22nd April) had returned its investors a 47% share price increase since the start of the war.

Source: Echo Energy

Whatever phrase you might use to describe it – end of bull run or correction – bitcoin has fallen to its lowest levels in years – $29,000. A number of factors can be attributed, but one key driver has been the collapse of so called stable coin terraUSD (UST), which as a supposedly stable asset, fell from a high of $118 (£96) to $0.4, rocking the crypto currency markets and having a knock-on effect on other stablecoins. The companies behind stablecoins try to ensure they remain in parity with assets such as the US dollar, so one token will equal $1. The collapse of a stablecoin has fundamentally weakened crypto assets for the present, but despite this, after touching $29,000, BTC rocketed 7.6% to $31,200 in one day, demonstrating that there is a chance for brave traders to turn a profit during these volatile times.

This volatility also boosted cryptocurrency transaction volumes on platforms like Binance and Hotcoin Global, which on 11th May 2022 saw 24hr trading volumes of $27.44bn and $10.27bn respectively, generating spectacular platform commission in the process.

There has also been a consequential read over for listed blockchain and crypto companies such as dual listed Coinsilium (AQX: COIN, OTCQB: CINGF), which is a blockchain, open finance, and crypto finance venture builder. Coinsilium shares fell to $0.025 on May 12th, but the next day shares rocketed to $0.039, providing a 24hr return of 56%. The drop in price for # Coinsilium can be attributed to systematic (market) risk and macro-economic factors such as inflation and the collapse in stable coin terraUSD.

While cryptocurrency continues to fluctuate, of course share price performance can be driven by stock specific issues in addition to macro factors. In the case of Coinsilium, in addition to a substantial amount of cash reserves held in crypto currency, the company is growing through its strong fundamentals and most recently a positive response to its recent seed investment in Yellow Network, the first broker clearing network for cryptocurrency exchanges, brokers and trading institutions. Yellow Network assists and develops mesh networks of crypto brokers and traders to execute ultra-high speed trading via decentralised exchanges. With such high volatility and huge transaction volumes in the crypto markets, Coinsilium’s Yellow Network investment could see it benefit from substantial, volume based commission revenues in the future.

What both Echo Energy and Coinsilium fundamentals demonstrate here, is that despite the market turmoil and highly uncertain outlook, they both depict the core principle of the markets – ‘higher the risk, higher the reward.

Power Metal Resources #POW – Selta Rare Earth Element and Uranium Project – Project Update

Power Metal Resources plc (LON:POW), the London listed exploration company seeking large-scale metal discoveries across its global project portfolio, announces an update in respect of the Selta Project (“Selta” or the “Project”) prospective for Rare Earth Element (“REE”) and Uranium (“U”) mineralisation located in the Northern Territory, Australia.

Power Metal Resources plc (LON:POW), the London listed exploration company seeking large-scale metal discoveries across its global project portfolio, announces an update in respect of the Selta Project (“Selta” or the “Project”) prospective for Rare Earth Element (“REE”) and Uranium (“U”) mineralisation located in the Northern Territory, Australia.

A map showing the location of the Selta Project may be viewed through the following link:

https://www.powermetalresources.com/selta-project-overview-map-2/

HIGHLIGHTS

– URE Metals Pty Limited (“URE”) has received notification from the Northern Territory Government’s Delegate for the Minister for Mining and Industry of their intention to imminently grant all Selta Project Mineral Exploration Licences EL 32737, EL 32738 and EL 32755 (see below for further information).

– First Development Resources Limited (“FDR”) have commenced an in-depth review of all available geological, geophysical and geochemical data associated with the Selta Project and adjacent ground. The objective of the review is to identify priority targets for further investigation.

Paul Johnson Chief Executive Officer of Power Metal Resources plc commented:

“The profile of REE and uranium exploration has increased significantly of late as the demand for critical minerals to support technological advancements in electric vehicle and alternative energy sources continues to grow.

Power Metal acquired the Selta Project to secure a strategic positioning in this highly prospective REE and uranium area in the Northern Territory of Australia. As you will see below, this acquisition looks very much to be in the right place and timely.”

Tristan Pottas Chief Executive Officer of First Development Resources Ltd commented:

“In parallel with the finalisation of the licence grant process we have now initiated an in-depth review of all relevant historical data associated with the Selta Project and the region as a whole, with the aim of identifying prospective areas of interest for further investigation.

The central Northern Territory region remains of particular interest to explorers looking to capitalise on the increase in global demand for REEs and uranium as evidenced by our listed neighbours MegaWatt Lithium and Battery Metals Corp (CSE:MEGA); who recently announced they were set to commence exploration at their nearby properties1. We look forward to updating the market on the findings of our in-depth data review as the study progresses.”

BACKGROUND

Selta is held within URE Metals Pty Limited, an Australian private company and wholly owned subsidiary of First Development Resources Limited which is planning to list on the London capital markets in Q2 2022. Power Metal currently holds a 96.15% interest in FDR.

URE was acquired by FDR in a transaction managed and funded by Power Metal and the announcement dated 19 November 2021 in respect of this transaction may be viewed through the following link:

LICENCE GRANT PROCESS

URE has received notification from the Delegate of the Minister for Mining and Industry, as provided by section 78(2) of the Mineral Titles Act 2010 of their intention to grant Mineral Exploration Licences EL 32737, EL 32738 and EL32755 which together make up the Selta Rare Earth Element and Uranium Project in the Northern Territory, Australia.

The grant will be effective from the date of payment of the rent for the first operational year which totals AU$19,190. Arrangements have been made for immediate payment and FDR expects to receive final grant notification in the coming days.

FDR through URE has commenced an in-depth review of all historical geological, geophysical and geochemical data associated with the Selta Project. The objective of the review is to identify targets for follow up investigation.

SELTA PROJECT IN-DEPTH DATA REVIEW

FDR have partnered with Mr Matthew Stephens of Luksam Consultants based in Queensland, Australia, to complete an in-depth review of all historical geological, geophysical and geochemical data associated with the Selta Project and the Central Northern Territory region as a whole.

Mr Stephens, who is a Fellow of the Australian Institute of Geoscientists (FAIG), has over 35 years of continuous industry experience which has included sound exposure to pre-feasibility, feasibility and due diligence studies as well as geotechnical Reviews, independent geologist reports, National I 43-101 reports and tenement appraisals.

In addition to compiling a review of all historical data, the desktop study will provide a comprehensive appraisal of the regional setting of Selta Project access, infrastructure and a prioritised list of exploration target areas.

SELTA PROJECT – BACKGROUND

The Selta Project, considered to be prospective for uranium and rare-earth elements, is located in Australia’s Northern Territory within the prospective but largely under-explored central Aileron Province, between the Georgia and Ngalia Basins, in a region the Northern Territory Government has declared prospective for uranium mineralisation.

The Project comprises three exploration licence applications covering a total land area of 1,574.92 km2 including EL 32737 – 780.85km2, EL 32738 – 312.17 km2 and EL 32755 – 481.90 km2.

The Northern Territory hosts some of Australia’s best known and high-grade uranium deposits and has a long history of uranium mining. In addition, the Aileron Province is a major exploration target for base metals including nickel (“Ni”) and copper (“Cu”), REEs and orogenic gold (“Au”) with numerous companies actively exploring within the region.

The Selta Project borders Prodigy Gold NL (ASX:PRX), IGO Ltd (ASX:IGO) and Canadian listed Megawatt Lithium and Battery Metals Corp (CSE:MEGA) (“Megawatt”); and is less than 70 km northwest of Arafura Resources’ (ASX:ARU) high-grade, world-class Nolans Bore REE deposit.

The Nolans Bore REE-phosphate-uranium-thorium deposit is one of the largest deposits of its kind in the world with a JORC (2012) compliant Mineral Resource of 56 million tonnes at an average grade of 2.6% total rare-earth oxides and 11% phosphate (P2O5). Commercial production is targeted for late 2024, with the Feasibility Study considering a 4,440 tonne per annum neodymium (“Nd”) – praseodymium (“Pr”) oxide producing open pit mining operation with a 38 year mine-life and an NPV8% of US$1.011B.2

The Selta Project’s southern claim boundary abuts the Megawatt landholding. Promising surface samples collected within the Megawatt property coupled with a known radiometric trend is currently postulated by the Company to link the Megawatt property with Arafura’s ground to the south-east.

MegaWatt recently announced exploration for REEs and uranium was set to commence at their adjacent Arctic Fox Project, located immediately south of Selta, and their Isbjorn Project also within the Central Northern Territory region.

The Selta Project area is currently located along strike to the northwest of the radiometric trend and future work will seek to extend that trend within the Selta Project. The underlying geology within the Selta Project is interpreted by the Company to be comparable to the Nolans Bore deposit with REE and U mineralisation at Nolans Bore being hosted within G6 granites which are postulated by the Company to be compositionally similar to the G5 granite prevalent across the Selta Project.

Notably, within 5km of the Selta Project’s eastern boundary are three REE occurrences with results up to 543ppm Nd and 148ppm praeseodymium hosted within the G5 granite. Selta’s exploration potential has been enhanced by encouraging historical surface sampling results3 of up to 3.8 ppm U in soil samples, 27.2 ppm U in stream sediment samples and up to 244 ppm U in rock chip samples, all of which led to a study by The Australian Mineral Development Laboratories3 stating:

“…the amount of uranium moved by solution or erosion is large enough for there to be several potentially economic orebodies.”

In addition to uranium the Company believe that the Selta project has significant potential for Cu, Au and silver (Ag) mineralisation.

Prodigy Gold’s Reynold Range Gold Copper Project, which borders the Selta Project’s lease area, has delivered encouraging results across four prospects for Cu, Au and Ag with reverse circulation drilling intercepts yielding 29m @ 2.32g/t Au (Falchion Prospect) and 17m @ 3.93g/t Au (Sabre Prospect) and surface samples of up to 7.5g/t Au, 783g/t Ag and 19.3% Cu (Scimitar Prospect) and 0.55g/t Au, 271g/t Ag and 20.3% Cu at the Reward Prospect.4

REFERENCES

1. Megawatt Exploration for REEs & Uranium within Central Northern Territory Properties Set to Commence and Marketing Agreement. Available at Megawatt Lithium and Battery Metals Exploration for REEs & Uranium within Central Northern Territory Properties Set to Commence … – MegaWatt (megawattmetals.com)

2. Arafura Resources Limited Annual General Meeting Presentation, 21/10/2021. Available at: https://wcsecure.weblink.com.au/pdf/ARU/02438942.pdf

3. The Australia Mineral Development Laboratories (CR 74/19) Sixth Progress Report MP 4976/73 Geochemical Survey, Arunta Area Amdel (December 1973)

4. PRX ASX Release – 20 May 2021. Available at: https://wcsecure.weblink.com.au/pdf/PRX/02376469.pdf

COMPETENT PERSON STATEMENT

The technical information contained in this disclosure has been read and approved by Mr Nick O’Reilly (MSc, DIC, MIMMM, MAusIMM, FGS), who is a qualified geologist and acts as the Competent Person under the AIM Rules – Note for Mining and Oil & Gas Companies. Mr O’Reilly is a Principal consultant working for Mining Analyst Consulting Ltd which has been retained by Power Metal Resources PLC to provide technical support.

This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 (“MAR”), and is disclosed in accordance with the Company’s obligations under Article 17 of MAR.

For further information please visit https://www.powermetalresources.com/ or contact:

|

Power Metal Resources plc |

|

|

Paul Johnson (Chief Executive Officer) |

+44 (0) 7766 465 617 |

|

|

|

|

SP Angel Corporate Finance (Nomad and Joint Broker) |

|

|

Ewan Leggat/Charlie Bouverat |

+44 (0) 20 3470 0470 |

|

|

|

|

SI Capital Limited (Joint Broker) |

|

|

Nick Emerson |

+44 (0) 1483 413 500 |

|

|

|

|

First Equity Limited (Joint Broker) |

|

|

David Cockbill/Jason Robertson |

+44 (0) 20 7330 1883 |

NOTES TO EDITORS

Power Metal Resources plc (LON:POW) is an AIM listed metals exploration company which finances and manages global resource projects and is seeking large scale metal discoveries.

The Company has a principal focus on opportunities offering district scale potential across a global portfolio including precious, base and strategic metal exploration in North America, Africa and Australia.

Project interests range from early-stage greenfield exploration to later-stage prospects currently subject to drill programmes.

Power Metal will develop projects internally or through strategic joint ventures until a project becomes ready for disposal through outright sale or separate listing on a recognised stock exchange thereby crystallising the value generated from our internal exploration and development work.

Value generated through disposals will be deployed internally to drive the Company’s growth or may be returned to shareholders through share buy backs, dividends or in-specie distributions of assets.

Power Metal Exploration Programmes Underway/Results Awaited

Power Metal has exploration programmes completed or underway, with results awaited, as outlined below:

|

Project |

Location |

POW % |

Work Completed or Underway |

Results Awaited |

|

|

|

|

|

|

|

Alamo Gold Project |

USA |

Earn-in to 75% |

Excavation of multiple test pits and mapping & sampling. |

Field and assay results from on-site work programme. |

|

Authier North Lithium |

Canada |

Earn-in to 100% |

Soil & rock sampling completed |

Interpretation of laboratory assay results of samples collected. |

|

Ditau Project |

Botswana |

50% |

Preparatory exploration work underway on target I10 leading to planned accelerated drilling targeting rare-earth elements and base metals

|

Field programme findings and defined drill targets for near term drilling. |

|

Kalahari Copper Belt |

Botswana |

50% |

Exploration programme underway across the South Ghanzi Project and further exploration at the more recently acquired South Ghanzi Extension and Mamuno licence areas |

Field programme findings and defined drill targets for near term drilling |

|

Molopo Farms |

Botswana |

53%A |

Kavango Option to acquire an interest in local project holding company. Option fee payable through defined work programme |

Results from various work activities underway as part of the Kavango Option |

|

Tati Gold/Nickel |

Botswana |

100% |

Reverse circulation drill programme completed |

Laboratory assay results awaited |

|

Haneti Project |

Tanzania |

35% |

Diamon drill programme underway |

Results from field programme including drill programme underway |

|

Victoria Goldfields |

Australia |

49.9% |

Ongoing exploration across 848km2 of granted exploration licences

|

Results from field programme including drill programme underway |

|

Wallal Gold/Copper Project |

Australia |

83.33%B |

Passive seismic and 2D seismic processing work programme completed. Ground reconnaissance work underway. |

Results awaited |

A should Kavango exercise their option to acquire Kalahari Key, Power Metal interest would reduce to 40% of the Molopo Farms Complex project

B assuming all licences held by URE Metals Pty Limited are granted as outlined in the Company’s announcement of 19.11.21 resulting in the issue of First Development Resources Ltd shares to URE vendors

#POW Power Metal Resources – Uranium Exploration Update – Athabasca Basin

Power Metal Resources PLC (LON:POW) the London listed exploration company seeking large-scale metal discoveries across its global project portfolio announces its 2021 work programme results from three of its 100% owned interests surrounding the Athabasca Basin in northern Saskatchewan, Canada.

Previously on 05/11/2021 the Power Metal announced that its Phase I work programme was complete, and that additional ground surrounding the company’s Tait Hill Property was acquired. A link to the announcement can be found below.

HIGHLIGHTS:

– Phase I exploration conducted over three of the seven Athabasca uranium properties, namely Tait Hill, Thibault Lake and Cleawater.

– 20 rock samples were collected for assay testing and the results demonstrate high grade uranium with the highest grade of 38,600ppm or 3.86% uranium oxide (“U308“).

– Multiple targets have been idenfitied for follow up exploration work in 2022.

Maps demonstrating the location of sample results across the three properties may be viewed on the Company’s website through the following links:

https://www.powermetalresources.com/tait-hill-phase-1-programme-results/

https://www.powermetalresources.com/thibaut-lake-phase-1-programme-results/

https://www.powermetalresources.com/clearwater-phase-1-programme-results/

Paul Johnson, Chief Executive Officer of Power Metal Resources plc commented:

“The confirmation of high grade uranium through assay testing of rock samples samples from the recent exploration programme is extremely positive and demonstrates the value of the diligent review work undertaken when the footprint was selected for staking earlier in the year.

There is considerable interest in the Athabasca uranium opportunity and Power Metal has, in my view and as evidenced today, built a compelling uranium exploration project portfolio in the area.

We remain of an acquisitive mindset with regard to uranium properties and are currently reviewing additional Canadian and African uranium exploration opportunities.”

EXPLORATION PROGRAMME ADDITIONAL INFORMATION:

– A total of 20 rock samples were collected as part of the Phase I programme including eight (8) from Tait Hill, seven (7) from Thibaut Lake, and five (5) from Clearwater. All samples were analysed at the Saskatchewan Research Council laboratory in Saskatoon, Saskatchewan. Power Metal employed a uranium-exploration analytical package which includes uranium, various base/trace-metals, as well as a suite of rare-earth elements (“REEs”).

– At Tait Hill, four (4) of the Properties eighteen (18) Saskatchewan Mineral Deposit Index point (“SMDI”) uranium occurences were visited by exploration crews. Several samples returned highly anomalous uranium mineralisation including rock samples up to 4,700ppm (0.47% U308). The rocks were collected along a northeast-southwest trending line of uranium-rich boulders. Tait Lake which is centrally located within the Tait Hill Property (see map), where 308,000kg of uranium with a insitu value of US$25.6 million (c. US$28 million at US$42/lb uranium) was calculated by the Saskatchewan Mining Development Corporation following a detailed lake-sediment drilling programme completed in 1980, was not visited as part of this programme.1 The historic work programme was completed solely on Tait Lake and the calculated resource is for Tait Lake and a few of the uranium-rich lakes immediately surrounding Tait Lake, which are majority held within the current Tait Hill Property.

– Power Metal has also successfuly obtained a high-resolution magnetics, electromagnetic (“EM”) and radiometric airborne survey flown Terraquest Ltd., on behalf of Canalaska Uranium Ltd., over the entire Tait Hill Property In 2008 the 4,290 line-km survey was flown at 150m-line spacing and successfully identified ten (10) radiometric anomalies at Tait Hill which were never followed up on. In addition, several magnetic and EM anomalies and lineaments were identified which will assist the Company is planning future work programmes on the Tait Hill Property.

– At Thibaut Lake, two (2) of the Properties six (6) SMDI uranium occurences were visited by exploration crews. Several samples returned highly anomalous uranium mineralisation including rock samples up to 38,600ppm (3.86% U308), as well as five (5) of the seven (7) samples which assayed >1,100ppm U308. The extremely high-grade sample was strongly mineralised with yellow carnotite and black pitchblende and displayed strong hematite alteration. The result greatly exceeds any historic samples taken within the area and represents a new exciting discovery for the Company.

– At Clearwater, three (3) of the Properties fourteen (14) SMDI uranium occurences were visited by exploration crews. Several samples returned strongly anomalous uranium mineralisation including rock samples up to 770ppm U308, including all samples which returned greater than 200ppm U308.

– Other notable rare-earth element results include thorium (Th) up to 1150ppm and zirconium up to 1,860ppm from the Tait Hill Property, as well as base-metal results including silver (Ag) up to 31.8ppm and lead (Pb) up to 8,320ppm from the Thibault Lake Property.

The Company is very pleased with the results obtained from the Phase I work programme where only one day of prospecting was spent on each of the three Properties. Several additional uranium occurrences have yet to be prospected by Power Metal, and the data obtained during this programme, as well as additional historic data acquired by the Company as part of the now completed historic data compilation, will be crucial in allowing the Company to unlock additional value from the Portfolio during the 2022 exploration season.

Table 1: 2021 Work Programme Rock Sample Assay Results

|

Title |

Property |

U3O8 wt % * |

U308 (ppm) |

|

149626 |

Tait Hill |

0.47 |

4,700 |

|

149627 |

Tait Hill |

0.02 |

200 |

|

149628 |

Tait Hill |

0.007 |

70 |

|

149629 |

Tait Hill |

0.011 |

110 |

|

149630 |

Tait Hill |

0.024 |

240 |

|

149631 |

Tait Hill |

0.105 |

1,050 |

|

149632 |

Tait Hill |

0.017 |

170 |

|

149633 |

Tait Hill |

0.006 |

60 |

|

149634 |

Thibaut Lake |

0.04 |

400 |

|

149635 |

Thibaut Lake |

0.115 |

1,150 |

|

149636 |

Thibaut Lake |

0.003 |

30 |

|

149637 |

Thibaut Lake |

0.165 |

1,650 |

|

149638 |

Thibaut Lake |

0.122 |

1,220 |

|

149639 |

Thibaut Lake |

0.267 |

2,670 |

|

149640 |

Thibaut Lake |

3.86 |

38,600 |

|

149641 |

Clearwater |

0.038 |

380 |

|

149642 |

Clearwater |

0.023 |

230 |

|

149643 |

Clearwater |

0.043 |

430 |

|

149644 |

Clearwater |

0.065 |

650 |

|

149645 |

Clearwater |

0.077 |

770 |

* U3O8 Assay by ICP, SRC Geoanalytical Laboratories, Saskatoon, Saskatchewan,

Reference Notes:

1: C. E. Roy and S. A. Earle, Saskatchewan Mineral Development Corporation Exploration – Summer 1980, Grease River-Scott Lake Project, CBS 5479, 5539, 5869 (74O09-0022). December, 1980

COMPETENT PERSON STATEMENT

The technical information contained in this disclosure has been read and approved by Mr Nick O’Reilly (MSc, DIC, MIMMM, MAusIMM, FGS), who is a qualified geologist and acts as the Competent Person under the AIM Rules – Note for Mining and Oil & Gas Companies. Mr O’Reilly is a Principal consultant working for Mining Analyst Consulting Ltd which has been retained by Power Metal Resources PLC to provide technical support.

This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 (“MAR”), and is disclosed in accordance with the Company’s obligations under Article 17 of MAR.

For further information please visit https://www.powermetalresources.com/ or contact:

|

Power Metal Resources plc |

|

|

Paul Johnson (Chief Executive Officer) |

+44 (0) 7766 465 617 |

|

|

|

|

SP Angel Corporate Finance (Nomad and Joint Broker) |

|

|

Ewan Leggat/Charlie Bouverat |

+44 (0) 20 3470 0470 |

|

|

|

|

SI Capital Limited (Joint Broker) |

|

|

Nick Emerson |

+44 (0) 1483 413 500 |

|

|

|

|

First Equity Limited (Joint Broker) |

|

|

David Cockbill/Jason Robertson |

+44 (0) 20 7330 1883 |

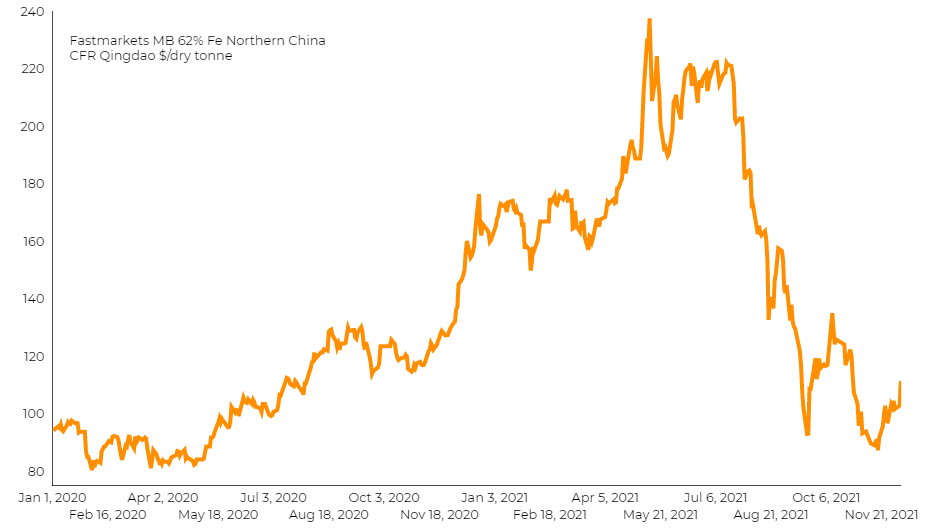

#KDNC Cadence Minerals – Iron ore price rockets as China imports hit highest in 16 months – Mining.com

Iron ore price surged on Tuesday after customs data showed China’s iron ore imports rose 14.6% in November from a month earlier to hit their highest since July 2020.

The world’s biggest consumer of iron ore brought in 104.96 million tonnes last month, up from October’s imports of 91.61 million and were also up 6.9% from November 2020, data from the General Administration of Customs showed.

According to Fastmarkets MB, benchmark 62% Fe fines imported into Northern China were changing hands for $111.34 a tonne, up 8.8% from Monday’s closing.

“November imports data could be affected by the customs clearance factor,” said Tang Binghua, an analyst with Founder CIFCO Futures in Beijing, adding that shipments and arrivals of iron ore did not change significantly in recent months.

“But it is unlikely that high levels of imports will continue, as consumption is weak after China stepped up output controls on mills during the heating season and ahead of the Winter Olympics.”

“The surprise in import growth was driven by a rebound in commodity volume, probably reflecting improving infrastructure capex demand as local governments stepped up stimulus toward the turn of the year,” said Michelle Lam, greater China economist at Societe Generale SA in Hong Kong.

Stocks of imported iron ore at Chinese ports grew for 10 straight weeks, jumping last week to 155.5 million tonnes, the highest since mid-2018, data from consultancy Mysteel showed.

In the first 11 months of the year, China imported 1.04 billion tonnes of iron ore, down 3.2% from the corresponding period a year earlier.

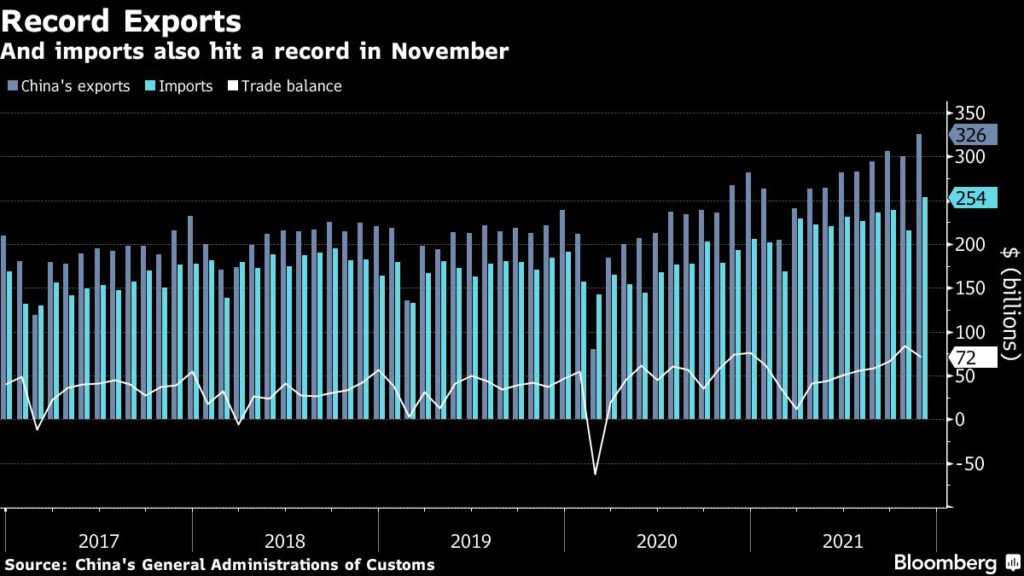

China’s total imports grew almost 32% to about $254 billion. Economists had forecast imports to increase by 21.5%.

Exports also rose 22% in dollar terms from a year earlier to almost $326 billion.

Read the article on Mining.com