Home » Posts tagged 'Parys Mountain'

Tag Archives: Parys Mountain

#AYM Anglesey Mining Plc – Anglesey and RheEnergise Partner to Explore Underground Energy Storage at Parys Mountain Mine, through the Rehabilitation of the Existing 300m Deep Morris Shaft.

Anglesey Mining plc and RheEnergise Partner to Explore Underground Energy Storage at Parys Mountain Mine, through the Rehabilitation of the Existing 300m Deep Morris Shaft

Anglesey Mining and RheEnergise are pleased to announce the signing of a memorandum of understanding (MOU) to explore the potential deployment of RheEnergise’s innovative High-Density Hydro® (HD Hydro) energy storage technology at the Parys Mountain mine site. The collaboration aims to provide an energy storage solution to support existing and planned renewable energy projects on the Isle of Anglesey and also a reliable source of clean energy for future mining and mineral processing operations. High-Density Hydro® (HD Hydro) energy storage is based on traditional pumped energy storage technology but rather than using water, a high-density fluid which is 2.5 x more dense than water is used in a closed loop. This technology requires 2.5 x less elevation than water-based systems for a given output and installations would also be correspondingly smaller and cheaper.

The MOU outlines the two companies’ intention to jointly investigate the feasibility of utilising the modern 300-meter-deep Parys Mountain Morris Shaft to host a hydro-energy storage project. This initiative would not only demonstrate the capabilities of RheEnergise’s HD Hydro technology in an operational environment but also facilitate the redevelopment of the underground mine at Parys Mountain.

The initial focus of the collaboration will be on conducting a comprehensive scoping study to assess the technical and economic viability of the proposed project. This will involve evaluating the potential environmental impacts and identifying any necessary permits or regulatory approvals.

The parties have agreed to work together to secure non-dilutive funding to support the project through the various stages of development, from feasibility study to construction and commissioning, including de-watering of the Morris shaft.

” RheEnergise has shown that it is able to deliver demonstration projects here in the UK,” said Rob Marsden, Chief Executive of Anglesey Mining. “The infrastructure and mothballed assets at Parys Mountain provide an ideal site at which to place a commercial scale plant. Anglesey Mining is focused on delivering a polymetallic underground mine at Parys Mountain. Securing a source of consistent green power on site while benefiting from the synergies between deployment of the technology and establishing a presence back underground at Parys Mountain is key to the strategy of de-risking the incremental development of the mine.”

“We are delighted to have the opportunity to work with Anglesey Mining on this groundbreaking project,” said Stephen Crosher, Chief Executive of RheEnergise. “The Parys Mountain site presents a unique opportunity to demonstrate the versatility and scalability of our HD Hydro technology. We believe that this project will serve as a model for future deployments of energy storage solutions at mine sites around the world.”

About Anglesey Mining

Anglesey Mining is a leading mineral exploration company focused on the development of the Parys Mountain polymetallic deposit in Wales. The company is committed to sustainable mining practices and seeks to minimize its environmental impact while maximizing the economic benefits of its operations.

Anglesey Mining is traded on the AIM market of the London Stock Exchange and currently has 461,593,017 ordinary shares in issue.

Anglesey Mining is developing the 100% owned Parys Mountain Cu-Zn-Pb-Ag-Au VMS deposit in North Wales, UK with a reported resource of 5.3 million tonnes at over 4.0% combined base metals in the Measured and Indicated categories and 10.8 million tonnes at over 2.5% combined base metals in the Inferred category.

Anglesey Mining also holds a 49.8% interest in the Grängesberg iron ore project in Sweden and 11.9% of Labrador Iron Mines Holdings Limited, which through its 52% owned subsidiaries, is engaged in the exploration and development of direct shipping iron ore deposits in Labrador and Quebec.

About RheEnergise

RheEnergise is an innovative energy storage company pioneering the development of High-Density Hydro® technology. The company’s mission is to provide cost-effective and sustainable energy storage solutions that can help accelerate the transition to a low-carbon economy.

How the HD Hydro system works: at times of low energy demand, with associated low costs, the High-Density Fluid R-19™ is pumped uphill between storage tanks (buried underground). The storage tanks are connected by underground pipes. As energy prices rise, the benign fluid is released downhill and passes through turbines, generating electricity to supply power to the grid. Projects will range from 5MW to 100MW of power and can work with vertical elevations as low as 100m or less. It means that, unlike conventional pumped hydro energy storage, a RheEnergise HD Hydro system can operate beneath small hills rather than mountains; the system requires 2½ times less vertical elevation. It also means that there are many more sites suitable for RheEnergise projects – in the UK and across the world.

RheEnergise’s analysis of potential project opportunities has indicated that there are c6500 site opportunities in the UK, c115,000 in Europe, c345,000 in North America and c500,000 in Africa and the Middle East.

In November 2022, RheEnergise was awarded a UK £8.25m small business research initiative (SBRI) contract from the UK Government’s Net Zero Innovation Portfolio (NZIP) to deploy a first-of-a-kind demonstrator at a site near Plymouth, Devon.

For further information

RheEnergise – www.rheenergise.com / LinkedIn @rheenergise

Stephen Crosher, Chief Executive: sc@rheenergise.com

Philippa Rogers, Communications Manager: 07971 269559 / pr@rheenergise.com

Anglesey Mining plc – www.angleseymining.co.uk

Rob Marsden, CEO: 07531 475111 / rob.marsden@angleseymining.co.uk

Anglesey Mining plc

Rob Marsden, Chief Executive Officer – Tel: +44 (0)7531 475111

Andrew King, Chairman – Tel: +44 (0)7825 963700

Davy – Nominated Adviser & Joint Corporate Broker

Brian Garrahy / Daragh O’Reilly – Tel: +353 1 679 6363

Zeus Capital Limited – Joint Corporate Broker

Katy Mitchell / Harry Ansell – Tel: +44 (0)161 831 1512

Anglesey Mining #AYM – Information received from statutory and specialist consultees regarding the Parys Mountain Mine Environmental Impact Assessment Scoping Report

![]() Further to the Company’s announcement on 16 August 2024, Anglesey Mining plc (AIM:AYM), is pleased to announce that it has recently received reports from statutory and specialist consultees in response to the Parys Mountain Mine Environmental Impact Assessment (EIA) Scoping Report. The Company is pleased to note that the responses received are broadly in line with the company’s expectations.

Further to the Company’s announcement on 16 August 2024, Anglesey Mining plc (AIM:AYM), is pleased to announce that it has recently received reports from statutory and specialist consultees in response to the Parys Mountain Mine Environmental Impact Assessment (EIA) Scoping Report. The Company is pleased to note that the responses received are broadly in line with the company’s expectations.

The responses from the statutory consultees will be taken into account by the North Wales Minerals and Waste Planning Service, who assess mineral planning applications on behalf of the Isle of Anglesey County Council, for the purposes of their formal Scoping Opinion which the Company expects to be released in due course.

As previously noted, the Anglesey Mining team are committed to close collaboration with stakeholders, communities, industry and supply chain, particularly around minimising potential environmental impacts and maximising economic development opportunities for local communities.

The Scoping Report and appendices can be accessed and downloaded from the Parys Mountain section of our web site by clicking this link:

https://www.angleseymining.co.uk/environmental-impact-assessment-eia-scoping-report/

or from the Anglesey County Council and North Wales Minerals and Waste Planning Service websites by clicking the following link:

If you wish to submit comments through the formal scoping processes, please send your comments directly to the North Wales Minerals and Waste Planning Service.

In the meantime, if you wish to provide comments regarding the proposal to the Anglesey Mining Team directly, please address them to mail@angleseymining.co.uk with the subject “Scoping Report Comments.”

Rob Marsden, CEO of Anglesey Mining, commented: “We encourage stakeholders to comment and ask questions, so that a highly considered EIA submission can be made. [We also welcome the opportunity to engage constructively with the North Wales Minerals and Waste Planning Service as it progresses with the Scoping Opinion.] The objective of Anglesey Mining is to make a planning application, that when enacted, will be seen to provide economic returns to investors, job opportunities, mitigation of the impacts to the environment and enhanced respect for, and appreciation of, the mining heritage of Parys Mountain, thus earning us a social licence to operate.”

About Anglesey Mining plc:

Anglesey Mining is traded on the AIM market of the London Stock Exchange and currently has 461,593,017 ordinary shares in issue.

Anglesey is developing the 100% owned Parys Mountain Cu-Zn-Pb-Ag-Au VMS deposit in North Wales, UK with a reported resource of 5.3 million tonnes at over 4.0% combined base metals in the Measured and Indicated categories and 10.8 million tonnes at over 2.5% combined base metals in the Inferred category.

Anglesey also holds a 49.75% interest in the Grängesberg iron ore project in Sweden and 12% of Labrador Iron Mines Holdings Limited, which through its 52% owned subsidiaries, is engaged in the exploration and development of direct shipping iron ore deposits in Labrador and Quebec.

For further information, please contact:

Anglesey Mining plc

Rob Marsden, Chief Executive Officer – Tel: +44 (0)7531 475111

Andrew King, Interim-Chairman – Tel: +44 (0)7825 963700

Davy

Nominated Adviser & Joint Corporate Broker

Brian Garrahy / Daragh O’Reilly – Tel: +353 1 679 6363

Zeus Capital Limited

Joint Corporate Broker

Katy Mitchell / Harry Ansell – Tel: +44 (0)161 831 1512

Copper works reopening hits ‘significant milestone’ – BBC Anglesey Mining article

Gareth Wyn Williams

Gareth Wyn WilliamsDevelopers hoping to restart mining an Anglesey copper works say they’ve reached a “significant milestone” after submitting the first necessary steps for plans that could create 120 jobs.

Tests show the area around Parys Mountain to contain deposits rich in copper, zinc, lead, silver and gold “worth around $1bn [£755m]”, according to Anglesey Mining PLC.

The company has now prepared the first phase of an environmental impact assessment with the ambition of new underground works at the site.

Anglesey councillor Aled Morris Jones said he welcomed “the potential to create jobs but while adhering to concrete guidelines to protect the environment”.

Link here to read the full article

Anglesey Mining #AYM and Parys Mountain featured in a report by Rob Shelley on ITV Wales

https://x.com/Brand_UK/status/1828693057845268553

A #copper rush on Anglesey? It is 120 years since the last miners left… but history could be about to come full circle at #ParysMountain #Anglesey

![]() CEO Rob Marsden and Site Manager Don McCallum talk through the history of the mine and the drill samples in the core shed

CEO Rob Marsden and Site Manager Don McCallum talk through the history of the mine and the drill samples in the core shed

Everything from #copper #gold #zinc #lead and #silver could be mined from a new section of Parys Mountain

Daily Telegraph – Bid to reopen 3,500-year-old Welsh mine after gold found in hills – Anglesey Mining #AYM

Anglesey Mining #AYM feature in the The Daily Telegraph by Jonathan Leake – Bid to reopen 3,500-year-old Welsh mine after gold found in hills.

Anglesey Mining #AYM feature in the The Daily Telegraph by Jonathan Leake – Bid to reopen 3,500-year-old Welsh mine after gold found in hills.

Bronze Age site on Anglesey could also hold copper, zinc & other precious metals

Anglesey Mining has unveiled plans to build new 630-metre shafts into Parys Mountain….

Rob Marsden chief executive of Anglesey Mining, said the mine also contained deposits of silver and lead.

He said: “Parys Mountain is demonstrably the largest and most advanced project for mining copper, gold, silver, lead and zinc in the UK.

“The project is favourably located on a previously permitted development site with significant existing infrastructure already in place…..”

Read full article here: https://www.telegraph.co.uk/business/2024/08/16/push-to-reopen-disused-welsh-mine-after-gold-found-in-hills/

Anglesey Mining #AYM – Proposed Placing and Subscription to raise approximately £415,000

![]() Anglesey Mining Plc (AIM:AYM) is pleased to announce its intention to raise gross proceeds of approximately £325,000 by means of a proposed placing (the “Placing”) of approximately 32,500,000 new ordinary shares of nominal value £0.01 (“Ordinary Shares”) each in the capital of the Company (the “Placing Shares”), to certain institutional and other investors, and a direct subscription of 9,000,000 new ordinary shares, to raise approximately £90,000 (the “Subscription”) (together the “Fundraising”), in each case at a price of 1p pence per share (the “Issue Price”).

Anglesey Mining Plc (AIM:AYM) is pleased to announce its intention to raise gross proceeds of approximately £325,000 by means of a proposed placing (the “Placing”) of approximately 32,500,000 new ordinary shares of nominal value £0.01 (“Ordinary Shares”) each in the capital of the Company (the “Placing Shares”), to certain institutional and other investors, and a direct subscription of 9,000,000 new ordinary shares, to raise approximately £90,000 (the “Subscription”) (together the “Fundraising”), in each case at a price of 1p pence per share (the “Issue Price”).

Rob Marsden and Andrew King are directors of the Company and have indicated their intention to subscribe for new Ordinary Shares as part of a subscription. Energold Minerals Inc. has also indicated its intention to subscribe for new Ordinary Shares as part of a subscription.

The Issue Price represents a discount of approximately 16.67 per cent. to the Closing Price of 1.2 pence per Ordinary Share on 27 June 2024 being the latest practicable business day prior to the publication of this Announcement.

The Placing is to be conducted by way of an accelerated bookbuild (the “Bookbuild”) process which will commence immediately following this Announcement and will be subject to the terms and conditions set out in the Appendix to this Announcement.

The Placing and Subscription is conditional on, amongst other matters, admission of the Placing Shares and the Subscription Shares to trading on AIM.

A further announcement confirming the closing of the Bookbuild and the number of Placing Shares and Subscription Shares to be issued pursuant to the Placing and Subscription is expected to be made in due course.

WH Ireland Limited (“WH Ireland”) is acting as bookrunner in relation to the Placing.

Capitalised terms used but not otherwise defined in this Announcement shall have the meanings ascribed to such terms at the end of the Appendix to this Announcement, unless the context requires otherwise.

Fundraising Highlights

- Placing and Subscription to raise approximately £415,000 (before expenses) from certain existing shareholders and other institutional investors.

- Placing to be conducted via an accelerated bookbuild process launching today.

- Issue Price of 1 pence per share represents a discount of 16.67 per cent. to the closing mid-market price of the Company’s existing Ordinary Shares on 27 June 2024, being the latest practicable business day prior to the publication of this Announcement.

- Certain directors of the Company have also indicated their intention to participate in the Subscription at the Issue Price.

Reasons for the Fundraise, Use of Proceeds and Transaction Summary

The Company is undertaking the Fundraise to progress its corporate and operational strategy and the net proceeds will therefore be applied towards:

- Developmental work at Parys Mountain

- Advancing development options at Grängesberg Iron Ore Mine

- Debt repayment; and

- General working capital purposes

The Company is advancing a number of initiatives with a view to supporting its cash position, however if these are not successful the Company will need to raise further funds towards the end of the calendar year to continue to progress its activities.

The Placing and Subscription

The Company intends to raise gross proceeds of up to £415,000 (before expenses) from participants in the Placing and Subscription.

WH Ireland is acting as Bookrunner (“Bookrunner”) in connection with the Placing. The Placing Shares are being offered by way of an accelerated bookbuild (the “Bookbuild”), which will be launched immediately following this Announcement, in accordance with the terms and conditions set out in the Appendix to this Announcement.

Admission of the Placing Shares is conditional, inter alia, upon the placing agreement dated 27 June 2024 between the Company and the Bookrunner (the “Placing Agreement”) not having been terminated and becoming unconditional prior to 04 July 2024 (or such later time and / or date as the Company and Bookrunner shall agree, not being later than 28 July 2024).

The Placing is also conditional upon, amongst other things:

- admission of the Placing Shares becoming effective by no later than 8.00 a.m. on 04 July 2024 (or such later time and / or date as the Company and Bookrunner shall agree, not being later than 28 July 2024);

• the delivery by the Company to the Bookrunner of certain documents required under the Placing Agreement;

• the Company having fully performed its obligations under the Placing Agreement to the extent that such obligations fall to be performed prior to admission of the Placing Shares;

• the Placing Agreement not having been terminated by the Bookrunner in accordance with its terms.

The timing of the closure of the Bookbuild and the allocation of the Placing Shares to be issued at the Issue Price are to be determined at the discretion of the Company and the Bookrunner.

Admission to trading

Application will be made to the London Stock Exchange for admission of the Placing Shares and the Subscription Shares to trading on AIM. It is expected that admission will become effective and dealings in the Placing Shares and Subscription Shares will commence at 8.00 a.m. on or around 04 July 2024.

The Placing Shares and Subscription Shares will be issued fully paid and will rank pari passu in all respects with the Company’s existing Ordinary Shares.

A further announcement will be made following the closure of the Bookbuild, confirming final details of the Placing.

The Placing is not being underwritten and the Placing is not conditional on a minimum amount being raised.

The person responsible for arranging for the release of this announcement on behalf of Anglesey is Rob Marsden.

For further information on the Company, please visit www.angleseymining.co.uk or contact:

Enquiries:

Anglesey Mining Plc www.angleseymining.co.uk

Rob Marsden, Chief Executive Officer Tel: +44 (0)7531 475111

Andrew King, Interim-Chairman Tel: +44 (0)7825 963700

Davy (Nominated Adviser & Joint Broker)

Brian Garrahy / Daragh O’Reilly Tel: +353 1 679 6363

WH Ireland Limited (Joint Broker and Bookrunner)

Harry Ansell / Daniel Bristowe Tel: +44 (0) 207 220 1666

Katy Mitchell / Andrew de Andrade

Anglesey Mining #AYM – Alan Green talks to CEO Rob Marsden at Parys Mountain

Alan Green talks to recently appointed Anglesey Mining #AYM CEO Rob Marsden direct from the Company’s flagship Parys Mountain mine. Rob discusses his career, in particular the years he spent working at Rio Tinto and also the 3 years he spent heading up the Rio investment committee, charged with seeking new investment opportunities for the mining giant. Rob then covers his work as a consultant, working around the world and then the time he spent with former CEO Jo Battershill at Parys Mountain a few years ago, which led up to his joining the board. Rob provides his overview of the latest assay results from hole NCZ003, and explains how he believes the previous drilling in the 1960’s and 1970’s can give the team ‘incredible confidence’ going forward. We then look at how the team plan to approach the pre feasibility study, via both divergent and convergent phases leading to a robust PFS ahead of the move to feasibility study. Rob then maps out what investors can expect in the coming weeks and months, and how this week he has assembled a team of colleagues including a longstanding veteran Rio Tinto geologist who will bring ‘fresh eyes’ to the project.

Anglesey Mining #AYM – Following assay results for hole NCZ003, WH Ireland maintains fair value at 5.4p per share

The Northern Copper Zone is shaping up to underpin enhanced mine plans and project economics for Parys Mountain Anglesey recently reported the assay results for the third drill hole completed at its’ Parys Mountain project. Drilling has confirmed the continuity and scale of the Northern Copper Zone (NCZ) which we believe is likely to contribute significant volumes of high-grade ore to mine plans in on-going feasibility studies. Surging metal prices and increased volumes will, we believe, contribute to significantly enhanced project economics once feasibility studies are reported.

The Northern Copper Zone is shaping up to underpin enhanced mine plans and project economics for Parys Mountain Anglesey recently reported the assay results for the third drill hole completed at its’ Parys Mountain project. Drilling has confirmed the continuity and scale of the Northern Copper Zone (NCZ) which we believe is likely to contribute significant volumes of high-grade ore to mine plans in on-going feasibility studies. Surging metal prices and increased volumes will, we believe, contribute to significantly enhanced project economics once feasibility studies are reported.

The Parys Mountain drill programme has successfully demonstrated the continuity of mineralisation at the NCZ, and it has improved confidence in the Garth Daniel and Central zones. Drilled intervals from the NCZ extend over at least 700m of strike and 400m down-dip, mineralisation is recorded in intervals over 10’s of meters. It is our belief that the drilled intervals lend themselves to low-cost bulk-mining methods and that this will significantly enhance the economic projections for Parys Mountain once feasibility studies are reported. We expect Anglesey will report an updated resource for Parys Mountain that we anticipate will include higher confidence resource categories as well as boosting contained metal. We maintain our fair value at 5.4p per share.

Introduction from new Anglesey Mining #AYM CEO Rob Marsden

An introduction from new Anglesey Mining #AYM CEO Rob Marsden from Parys Mountain

- Rob provides an overview of his CV, along with a brief overview of Parys Mountain mine and the surrounding area

- A brief overview of today’s assay results that “demonstrate good continuity, supporting the integrity of the geological model”

- Litho geochemical results from all three holes due in the coming weeks

- Targeting a resource update on the Northern Copper Zone

Anglesey Mining #AYM – Further drilling results confirm scale of Northern Copper Zone at Parys Mountain

![]() Anglesey Mining plc (AIM:AYM), is pleased to announce that assay results have been received for the recently completed drill hole NCZ003. Drill hole NCZ003 was the third hole to be completed from the infill drilling program of the Northern Copper Zone (NCZ) and Garth Daniel Zone (GDZ) at the Company’s Parys Mountain Cu-Zn-Pb-Ag-Au VMS project on the Isle of Anglesey in North West Wales.

Anglesey Mining plc (AIM:AYM), is pleased to announce that assay results have been received for the recently completed drill hole NCZ003. Drill hole NCZ003 was the third hole to be completed from the infill drilling program of the Northern Copper Zone (NCZ) and Garth Daniel Zone (GDZ) at the Company’s Parys Mountain Cu-Zn-Pb-Ag-Au VMS project on the Isle of Anglesey in North West Wales.

Consistent both with historical drilling and the recently completed NCZ001 and NCZ002 holes, the assays confirm NCZ003 intersected a significant zone of mineralisation across the NCZ with 90m @ 0.57% CuEq (including internal dilution). Drill hole NCZ003 was terminated prematurely at a depth of 535m due to a large, potentially fault-related void. The last 6 metres of core prior to the 4m void assayed 1.16% CuEq and coincides with previous high-grade assays from historic drilling.

As with the previous two holes in the program, NCZ003 intersected both broad zones of mineralisation and multiple higher-grade zones. Importantly, the drilling is demonstrating good continuity and further supports the integrity of the geological model and drill targeting, with indications of greater mineralised volumes overall.

Key intersections within the broad zone of mineralisation are detailed below:

Northern Copper Zone – Hole NCZ003

- 0m @ 0.51% Cu, 0.06% Zn, 0.03% Pb, 2.16g/t Ag and 0.14g/t Au (0.57% CuEq) from a depth of 389m, including:

- 0m @ 0.80% Cu, 2.19g/t Ag and 0.16g/t Au (0.82% CuEq) from 427.0m

- 0m @ 0.99% Cu, 4.33g/t Ag and 0.15g/t Au (1.08% CuEq) from 449.0m

- 0m @ 0.47% Cu, 1.53g/t Ag and 0.07g/t Au (0.49% CuEq) from 490.0m, including 4.0m @ 0.48% Cu, 2.48g/t Ag and 0.13g/t Au (0.53% CuEq)

- 0m @ 1.20% Cu, 1.10g/t Ag and 0.01g/t Au (1.16% CuEq) from 529m (hole stopped in mineralisation)

***CuEq grades are based on recovery factors and commodity prices as detailed after the tabulated reported assays of this release***

The third drill hole, NCZ003, concludes the on-site portion of the current exploration and infill drilling program and we are expecting litho-geochemical analysis results, from each of the three holes, to be back from the laboratory in Canada in the coming weeks. Subsequently, on the strength of all the data collected and the interpretation thereof, the Company is targeting a resource update on the NCZ, with the aim of converting a significant portion of the Inferred Resource into the higher confidence Indicated category. Based on the Joint Ore Reserve Committee (JORC) guidelines, only Indicated and Measured category Mineral Resources can be converted into Ore Reserves.

Andrew King, Interim Chairman of Anglesey Mining, commented: “Once again, we are very pleased to see the Parys Mountain project delivering some very strong drilling results. It is worth reminding investors that Parys Mountain is demonstrably the largest and most advanced copper project in the UK with substantial resource upside still evident. In addition, the project is favourably located on a previously permitted, brownfield development site with significant existing infrastructure already in place.“

“All three holes in the current program; NCZ001 NCZ002 and NCZ003 have delivered some exceptional high-grade copper intersections within broad thicknesses of mineralisation up to 100m wide. The results continue to support our view that the NCZ provides significant upside for the Parys Mountain project, over and above the 5 million tonne contribution included within the 2021 Preliminary Economic Assessment.”

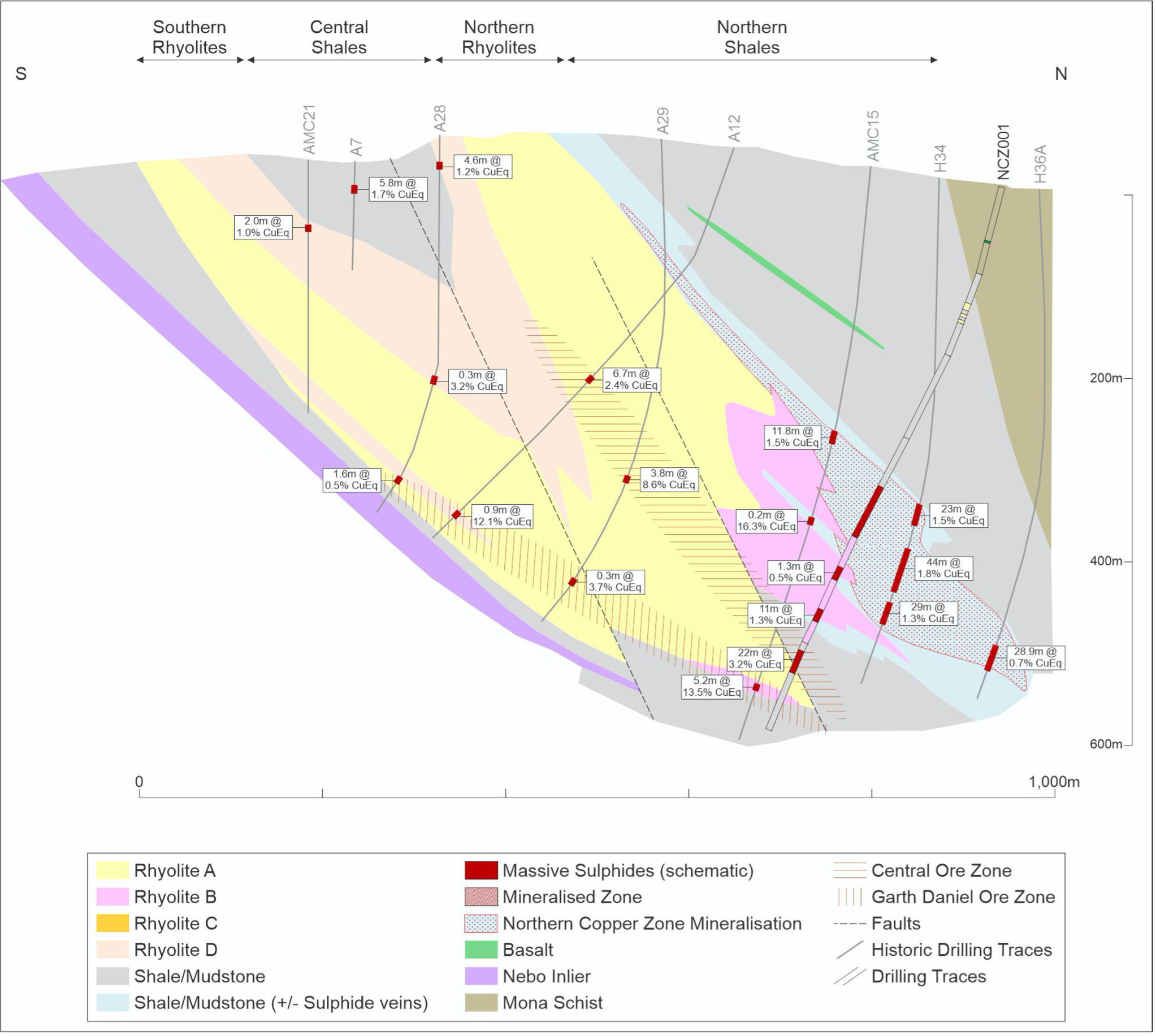

NCZ – Cross Section 4600mE

Section 4600mE below highlights the position of the recently completed drill hole NCZ002 and NCZ003.

The interpreted outline of the NCZ in the cross-section does not imply an economic outcome, it simply highlights where sulphides have been identified within the Northern Shales with a 0.5% CuEq cut-off. A significant number of the drill holes within this zone have returned consistent zones of higher-grade material, which was a key target of the program. The recognition of a shear zone along the hanging wall of the NCZ could imply a structural emplacement, or thickening of the sequence within the mine environment and will greatly assist with future targeting and drilling.

Importantly, every hole drilled into the interpreted position of the NCZ has intersected broad zones of sulphides; the drilling has demonstrated the predictability of the mineralised zone from the detailed geological model that has been constructed and refined over several years.

The most recent drill hole, NCZ003, targeted the up-dip area above historical hole H17A and has provided important additional information relating to the key lithology Rhyolite B – the emplacement of this unit is closely associated to the mineralising event. This additional information will now be incorporated into the geological model and the resource block model of the NCZ.

Drill hole NCZ003 ended prematurely at a depth of 535m due to faulted ground conditions and the intersection of a 4m void. The last metre of core prior to the void assayed 1.3% Cu and 1.22% CuEq. The location of the void correlates to the contact position of Rhyolite B and the host northern shale unit, which has traditionally been a zone related to higher grade intersections – drill hole A15 intersected 1.6m @ 3.7% CuEq approximately 100m up-dip from NCZ003 and NCZ001 intersected 22.0m @ 3.2% CuEq on section 4800mE (200m along strike).

NCZ – Cross Section 4800mE

Section 4800mE below highlights the position of drill hole NCZ001.

As per section 4600mE, this section also highlights the continuity of sulphide mineralisation across the NCZ. With the completion of NCZ003, the Company has gained a greater understanding of the influence from Rhyolite B on the higher-grade zones of mineralisation.

Section 4800mE also highlights the potential related to the Central Zone with significant intersections from historical 1970’s drilling, including 3.8m @ 8,6% Cu and 6.7m @ 2.4% Cu. The Company believes potential exists for these intersections to link to the 22m @ 3.2 % CuEq (including 4.0m @ 5.2% Cu) in NCZ001.

Drill hole details:

| Hole ID | Co-ordinates

(E) (N) |

Elevation

(m) |

Azimuth

(°) |

Dip (°) | End of Hole (m) | |

| NCZ003 | 243806.92 | 390948.57 | 73.09 | 165 | -72 | 535 |

Reported Assays (results >0.5 CuEq in bold):

| Hole Number | From | To | Sample Length | Assays | |||||

| (m) | (m) | (m) | Cu

(%) |

Zn

(%) |

Pb

(%) |

Ag (g/t) | Au (g/t) | CuEq

(%)* |

|

| NCZ003 | 264.4 | 264.8 | 0.4 | 0.02 | 1.34 | 0.26 | 3.6 | 0.11 | 0.42% |

| NCZ003 | 339.8 | 340.3 | 0.5 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 340.3 | 340.8 | 0.5 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 340.8 | 341.3 | 0.5 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 385 | 386 | 1 | 0.12 | 0.00 | 0.01 | 0.5 | 0.02 | 0.12% |

| NCZ003 | 386 | 387 | 1 | 0.38 | 0.00 | 0.01 | 0.7 | 0.02 | 0.37% |

| NCZ003 | 387 | 388 | 1 | 0.50 | 0.02 | 0.05 | 1.9 | 0.12 | 0.54% |

| NCZ003 | 388 | 389 | 1 | 0.36 | 0.01 | 0.09 | 1.1 | 0.12 | 0.42% |

| NCZ003 | 389 | 390 | 1 | 0.50 | 0.01 | 0.05 | 1.4 | 0.11 | 0.53% |

| NCZ003 | 390 | 391 | 1 | 0.25 | 0.00 | 0.03 | 1.0 | 0.18 | 0.32% |

| NCZ003 | 391 | 392 | 1 | 0.27 | 0.01 | 0.05 | 1.0 | 0.05 | 0.29% |

| NCZ003 | 392 | 393 | 1 | 0.44 | 0.01 | 0.04 | 1.5 | 0.41 | 0.60% |

| NCZ003 | 393 | 394 | 1 | 1.90 | 0.00 | 0.09 | 2.2 | 0.12 | 1.85% |

| NCZ003 | 394 | 395 | 1 | 0.04 | 0.00 | 0.01 | 0.5 | 0.06 | 0.07% |

| NCZ003 | 395 | 396 | 1 | 0.67 | 0.00 | 0.01 | 1.1 | 0.11 | 0.68% |

| NCZ003 | 396 | 397 | 1 | 0.33 | 0.00 | 0.00 | 1.1 | 0.32 | 0.45% |

| NCZ003 | 397 | 398 | 1 | 0.10 | 0.02 | 0.06 | 0.8 | 0.16 | 0.18% |

| NCZ003 | 398 | 399 | 1 | 0.18 | 0.01 | 0.02 | 0.8 | 0.06 | 0.20% |

| NCZ003 | 399 | 400 | 1 | 0.02 | 0.00 | 0.01 | 0.5 | 0.06 | 0.05% |

| NCZ003 | 400 | 401 | 1 | 0.32 | 0.01 | 0.01 | 1.2 | 0.18 | 0.38% |

| NCZ003 | 401 | 402 | 1 | 0.33 | 0.01 | 0.01 | 1.7 | 0.20 | 0.40% |

| NCZ003 | 402 | 403 | 1 | 0.34 | 0.00 | 0.01 | 1.1 | 0.10 | 0.37% |

| NCZ003 | 403 | 404 | 1 | 0.29 | 0.01 | 0.01 | 1.2 | 0.08 | 0.31% |

| NCZ003 | 404 | 405 | 1 | 2.80 | 0.02 | 0.01 | 4.2 | 0.28 | 2.75% |

| NCZ003 | 405 | 406 | 1 | 0.26 | 0.02 | 0.01 | 1.5 | 0.10 | 0.30% |

| NCZ003 | 406 | 407 | 1 | 0.27 | 0.01 | 0.01 | 2.6 | 0.25 | 0.37% |

| NCZ003 | 407 | 408 | 1 | 0.32 | 0.00 | 0.01 | 1.0 | 0.07 | 0.33% |

| NCZ003 | 408 | 409 | 1 | 0.23 | 0.00 | 0.01 | 0.8 | 0.14 | 0.28% |

| NCZ003 | 409 | 410 | 1 | 0.08 | 0.00 | 0.01 | 0.5 | 0.11 | 0.13% |

| NCZ003 | 410 | 411 | 1 | 0.62 | 0.01 | 0.01 | 2.0 | 0.49 | 0.79% |

| NCZ003 | 411 | 412 | 1 | 0.11 | 0.00 | 0.01 | 0.5 | 0.03 | 0.11% |

| NCZ003 | 412 | 413 | 1 | 0.19 | 0.01 | 0.01 | 0.9 | 0.12 | 0.24% |

| NCZ003 | 413 | 414 | 1 | 0.17 | 0.02 | 0.01 | 1.3 | 0.16 | 0.24% |

| NCZ003 | 414 | 415 | 1 | 0.29 | 0.00 | 0.00 | 0.8 | 0.10 | 0.31% |

| NCZ003 | 415 | 416 | 1 | 0.33 | 0.00 | 0.01 | 0.7 | 0.15 | 0.37% |

| NCZ003 | 416 | 417 | 1 | 1.14 | 0.01 | 0.02 | 1.8 | 0.15 | 1.14% |

| NCZ003 | 417 | 418 | 1 | 0.09 | 0.01 | 0.01 | 0.5 | 0.09 | 0.12% |

| NCZ003 | 418 | 419 | 1 | 0.50 | 0.01 | 0.01 | 1.8 | 0.09 | 0.52% |

| NCZ003 | 419 | 420 | 1 | 0.66 | 0.02 | 0.01 | 2.4 | 0.18 | 0.70% |

| NCZ003 | 420 | 421 | 1 | 0.25 | 0.01 | 0.01 | 1.0 | 0.08 | 0.28% |

| NCZ003 | 421 | 422 | 1 | 0.56 | 0.01 | 0.01 | 2.4 | 0.19 | 0.61% |

| NCZ003 | 422 | 423 | 1 | 0.76 | 0.01 | 0.01 | 2.6 | 0.24 | 0.83% |

| NCZ003 | 423 | 424 | 1 | 0.16 | 0.01 | 0.01 | 1.5 | 0.06 | 0.19% |

| NCZ003 | 424 | 425 | 1 | 0.05 | 0.01 | 0.01 | 1.2 | 0.11 | 0.10% |

| NCZ003 | 425 | 426 | 1 | 0.41 | 0.01 | 0.04 | 1.1 | 0.05 | 0.43% |

| NCZ003 | 426 | 427 | 1 | 0.17 | 0.00 | 0.01 | 0.7 | 0.08 | 0.20% |

| NCZ003 | 427 | 428 | 1 | 0.92 | 0.02 | 0.01 | 2.8 | 0.13 | 0.93% |

| NCZ003 | 428 | 429 | 1 | 0.86 | 0.00 | 0.01 | 1.5 | 0.10 | 0.86% |

| NCZ003 | 429 | 430 | 1 | 1.82 | 0.01 | 0.01 | 2.8 | 0.13 | 1.77% |

| NCZ003 | 430 | 431 | 1 | 1.41 | 0.04 | 0.01 | 4.2 | 0.19 | 1.43% |

| NCZ003 | 431 | 432 | 1 | 0.48 | 0.01 | 0.01 | 1.5 | 0.10 | 0.50% |

| NCZ003 | 432 | 433 | 1 | 0.07 | 0.00 | 0.00 | 0.6 | 0.05 | 0.09% |

| NCZ003 | 433 | 434 | 1 | 0.27 | 0.01 | 0.01 | 2.0 | 0.43 | 0.44% |

| NCZ003 | 434 | 435 | 1 | 0.53 | 0.01 | 0.00 | 2.1 | 0.15 | 0.57% |

| NCZ003 | 435 | 436 | 1 | 0.29 | 0.06 | 0.21 | 4.5 | 0.30 | 0.49% |

| NCZ003 | 436 | 437 | 1 | 0.12 | 0.01 | 0.01 | 2.2 | 0.15 | 0.19% |

| NCZ003 | 437 | 438 | 1 | 0.11 | 0.00 | 0.01 | 1.1 | 0.14 | 0.17% |

| NCZ003 | 438 | 439 | 1 | 0.21 | 0.02 | 0.00 | 1.7 | 0.09 | 0.25% |

| NCZ003 | 439 | 440 | 1 | 0.04 | 0.01 | 0.01 | 1.4 | 0.10 | 0.09% |

| NCZ003 | 440 | 441 | 1 | 0.05 | 0.00 | 0.00 | 0.9 | 0.08 | 0.09% |

| NCZ003 | 441 | 442 | 1 | 0.09 | 0.00 | 0.00 | 1.0 | 0.07 | 0.12% |

| NCZ003 | 442 | 443 | 1 | 0.80 | 0.01 | 0.00 | 2.4 | 0.19 | 0.84% |

| NCZ003 | 443 | 444 | 1 | 0.37 | 0.01 | 0.00 | 2.0 | 0.19 | 0.43% |

| NCZ003 | 444 | 445 | 1 | 0.38 | 0.04 | 0.04 | 4.3 | 0.36 | 0.55% |

| NCZ003 | 445 | 446 | 1 | 0.18 | 0.01 | 0.01 | 1.6 | 0.13 | 0.24% |

| NCZ003 | 446 | 447 | 1 | 0.31 | 0.01 | 0.00 | 2.0 | 0.14 | 0.36% |

| NCZ003 | 447 | 448 | 1 | 0.53 | 0.09 | 0.27 | 4.8 | 0.16 | 0.68% |

| NCZ003 | 448 | 449 | 1 | 0.24 | 0.01 | 0.17 | 1.6 | 0.10 | 0.32% |

| NCZ003 | 449 | 450 | 1 | 2.10 | 0.02 | 0.03 | 7.1 | 0.40 | 2.17% |

| NCZ003 | 450 | 451 | 1 | 0.51 | 0.01 | 0.02 | 2.3 | 0.18 | 0.57% |

| NCZ003 | 451 | 452 | 1 | 1.60 | 0.28 | 0.80 | 7.1 | 0.13 | 1.87% |

| NCZ003 | 452 | 453 | 1 | 0.95 | 0.03 | 0.26 | 5.3 | 0.21 | 1.08% |

| NCZ003 | 453 | 454 | 1 | 0.49 | 0.06 | 0.20 | 3.1 | 0.08 | 0.58% |

| NCZ003 | 454 | 455 | 1 | 0.14 | 0.01 | 0.02 | 1.0 | 0.06 | 0.16% |

| NCZ003 | 455 | 456 | 1 | 0.29 | 0.12 | 0.22 | 5.9 | 0.06 | 0.42% |

| NCZ003 | 456 | 457 | 1 | 0.30 | 0.08 | 0.08 | 2.1 | 0.13 | 0.38% |

| NCZ003 | 457 | 458 | 1 | 2.55 | 0.07 | 0.16 | 5.1 | 0.09 | 2.50% |

| NCZ003 | 458 | 459 | 1 | 0.28 | 0.06 | 0.12 | 3.0 | 0.16 | 0.39% |

| NCZ003 | 459 | 460 | 1 | 0.70 | 0.04 | 0.09 | 5.4 | 0.19 | 0.79% |

| NCZ003 | 460 | 461 | 1 | 0.76 | 0.03 | 0.02 | 3.5 | 0.17 | 0.80% |

| NCZ003 | 461 | 462 | 1 | 0.64 | 0.01 | 0.01 | 1.7 | 0.14 | 0.67% |

| NCZ003 | 462 | 463 | 1 | 0.39 | 0.01 | 0.01 | 1.7 | 0.08 | 0.40% |

| NCZ003 | 463 | 464 | 1 | 0.13 | 0.26 | 0.53 | 2.9 | 0.06 | 0.36% |

| NCZ003 | 464 | 465 | 1 | 0.13 | 0.06 | 0.19 | 1.8 | 0.03 | 0.21% |

| NCZ003 | 465 | 466 | 1 | 1.10 | 0.12 | 0.04 | 5.4 | 0.10 | 1.13% |

| NCZ003 | 466 | 467 | 1 | 0.42 | 0.04 | 0.08 | 3.9 | 0.10 | 0.48% |

| NCZ003 | 467 | 468 | 1 | 0.18 | 0.00 | 0.07 | 0.7 | 0.02 | 0.20% |

| NCZ003 | 468 | 469 | 1 | 0.31 | 0.02 | 0.05 | 1.9 | 0.03 | 0.33% |

| NCZ003 | 469 | 470 | 1 | 0.14 | 0.09 | 0.18 | 1.9 | 0.08 | 0.24% |

| NCZ003 | 470 | 471 | 1 | 0.10 | 0.03 | 0.14 | 1.1 | 0.02 | 0.16% |

| NCZ003 | 471 | 472 | 1 | 1.71 | 0.05 | 0.09 | 6.4 | 0.05 | 1.68% |

| NCZ003 | 472 | 473 | 1 | 0.12 | 0.01 | 0.01 | 0.8 | 0.06 | 0.14% |

| NCZ003 | 473 | 474 | 1 | 0.15 | 0.01 | 0.01 | 0.9 | 0.04 | 0.16% |

| NCZ003 | 474 | 475 | 1 | 0.71 | 0.02 | 0.05 | 1.7 | 0.13 | 0.74% |

| NCZ003 | 475 | 476 | 1 | 0.58 | 0.02 | 0.01 | 3.2 | 0.17 | 0.63% |

| NCZ003 | 476 | 477 | 1 | 0.07 | 0.01 | 0.06 | 0.8 | 0.04 | 0.11% |

| NCZ003 | 477 | 478 | 1 | 0.82 | 0.04 | 0.05 | 3.5 | 0.16 | 0.87% |

| NCZ003 | 478 | 479 | 1 | 1.37 | 0.02 | 0.04 | 3.5 | 0.08 | 1.34% |

| NCZ003 | 479 | 480 | 1 | 0.10 | 0.01 | 0.05 | 0.8 | 0.04 | 0.12% |

| NCZ003 | 480 | 481 | 1 | 0.04 | 0.03 | 0.06 | 0.7 | 0.03 | 0.07% |

| NCZ003 | 481 | 482 | 1 | 0.13 | 0.01 | 0.02 | 0.5 | 0.03 | 0.14% |

| NCZ003 | 482 | 483 | 1 | 0.38 | 0.01 | 0.02 | 1.3 | 0.05 | 0.39% |

| NCZ003 | 483 | 484 | 1 | 0.07 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 484 | 485 | 1 | 0.02 | 0.00 | 0.01 | 0.5 | 0.01 | 0.03% |

| NCZ003 | 485 | 486 | 1 | 0.40 | 0.00 | 0.01 | 0.6 | 0.03 | 0.39% |

| NCZ003 | 486 | 487 | 1 | 0.03 | 0.00 | 0.01 | 0.5 | 0.02 | 0.04% |

| NCZ003 | 487 | 488 | 1 | 0.02 | 0.13 | 0.06 | 0.8 | 0.02 | 0.07% |

| NCZ003 | 488 | 489 | 1 | 0.19 | 0.01 | 0.02 | 0.5 | 0.03 | 0.19% |

| NCZ003 | 489 | 490 | 1 | 0.15 | 0.00 | 0.01 | 0.5 | 0.02 | 0.15% |

| NCZ003 | 490 | 491 | 1 | 0.63 | 0.03 | 0.01 | 4.1 | 0.19 | 0.69% |

| NCZ003 | 491 | 492 | 1 | 0.51 | 0.07 | 0.02 | 4.0 | 0.26 | 0.63% |

| NCZ003 | 492 | 493 | 1 | 0.13 | 0.01 | 0.07 | 0.9 | 0.04 | 0.16% |

| NCZ003 | 493 | 494 | 1 | 0.66 | 0.00 | 0.01 | 0.9 | 0.02 | 0.63% |

| NCZ003 | 494 | 495 | 1 | 0.09 | 0.06 | 0.05 | 1.0 | 0.04 | 0.13% |

| NCZ003 | 495 | 496 | 1 | 0.01 | 0.01 | 0.01 | 0.5 | 0.02 | 0.03% |

| NCZ003 | 496 | 497 | 1 | 0.31 | 0.01 | 0.01 | 1.2 | 0.06 | 0.32% |

| NCZ003 | 497 | 498 | 1 | 0.83 | 0.02 | 0.01 | 1.7 | 0.04 | 0.81% |

| NCZ003 | 498 | 499 | 1 | 0.63 | 0.01 | 0.01 | 1.1 | 0.05 | 0.61% |

| NCZ003 | 499 | 500 | 1 | 0.03 | 0.00 | 0.01 | 0.5 | 0.01 | 0.04% |

| NCZ003 | 500 | 501 | 1 | 0.47 | 0.00 | 0.01 | 1.2 | 0.03 | 0.46% |

| NCZ003 | 501 | 504 | 3 | 0.64 | 0.04 | 0.14 | 1.5 | 0.08 | 0.69% |

| NCZ003 | 504 | 505 | 1 | 0.78 | 0.09 | 0.15 | 1.4 | 0.03 | 0.81% |

| NCZ003 | 505 | 506 | 1 | 0.08 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 506 | 507 | 1 | 0.04 | 0.00 | 0.01 | 0.5 | 0.01 | 0.05% |

| NCZ003 | 507 | 508 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 508 | 509 | 1 | 0.00 | 0.00 | 0.02 | 0.5 | 0.01 | 0.02% |

| NCZ003 | 509 | 510 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 510 | 511 | 1 | 0.02 | 0.00 | 0.01 | 0.5 | 0.02 | 0.03% |

| NCZ003 | 511 | 512 | 1 | 0.19 | 0.00 | 0.05 | 0.5 | 0.01 | 0.20% |

| NCZ003 | 512 | 513 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 513 | 514 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 514 | 515 | 1 | 0.01 | 0.00 | 0.01 | 0.6 | 0.03 | 0.03% |

| NCZ003 | 515 | 516 | 1 | 0.07 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 516 | 517 | 1 | 0.04 | 0.01 | 0.02 | 0.5 | 0.01 | 0.05% |

| NCZ003 | 517 | 518 | 1 | 0.83 | 0.00 | 0.01 | 0.8 | 0.01 | 0.78% |

| NCZ003 | 518 | 519 | 1 | 0.14 | 0.01 | 0.02 | 0.8 | 0.01 | 0.14% |

| NCZ003 | 519 | 520 | 1 | 0.15 | 0.00 | 0.02 | 0.5 | 0.01 | 0.15% |

| NCZ003 | 520 | 521 | 1 | 0.06 | 0.00 | 0.02 | 0.5 | 0.01 | 0.07% |

| NCZ003 | 521 | 522 | 1 | 0.10 | 0.00 | 0.02 | 0.5 | 0.01 | 0.11% |

| NCZ003 | 522 | 523 | 1 | 0.03 | 0.00 | 0.01 | 0.5 | 0.01 | 0.04% |

| NCZ003 | 523 | 524 | 1 | 0.25 | 0.00 | 0.02 | 0.5 | 0.01 | 0.24% |

| NCZ003 | 524 | 525 | 1 | 0.01 | 0.00 | 0.01 | 0.5 | 0.01 | 0.02% |

| NCZ003 | 525 | 526 | 1 | 0.21 | 0.00 | 0.01 | 0.5 | 0.01 | 0.20% |

| NCZ003 | 526 | 527 | 1 | 0.08 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 527 | 528 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 528 | 529 | 1 | 0.24 | 0.00 | 0.01 | 0.5 | 0.01 | 0.23% |

| NCZ003 | 529 | 531 | 2 | 1.15 | 0.01 | 0.19 | 1.2 | 0.01 | 1.13% |

| NCZ003 | 534 | 535 | 1 | 1.30 | 0.01 | 0.02 | 0.9 | 0.01 | 1.22% |

| Total | 148.90 | ||||||||

* Copper Equivalent (CuEq %) = Cu grade % * Cu Recovery + (Zn grade % * Zn Recovery * (Zn price $/t /Cu price $/t)) + (Pb grade % * Pb Recovery * (Pb price $/t /Cu price $/t)) + (Ag grade g/t / 31.103 * Ag recovery * (Ag price $/oz /Cu price $/t)) + (Au grade g/t / 31.103 * Au recovery * (Au price $/oz /Cu price $/t))

Cu Equivalent calculated using following commodity prices: Zn – US$3350/t, Cu – US$9523/t, Pb – US$2292/t, Ag – US$25.50/oz and

Au – US$1850/oz

Cu Equivalent calculated using following recovery assumptions for Northern Copper Zone: Zn – 82%, Cu – 93%, Pb – 78%, Ag – 72% and Au – 65%

Sample analysis and QA/QC

All samples generated from the drilling were dispatched to ALS Loughrea, Ireland.

Samples were assayed for multi-element data analysis using their ME-ICP61 package, which includes Ag, Cu, Pb and Zn. The samples were also assayed for gold using their Au-AA23 analysis package. Overlimit assays were then analysed using their Ag-OG62, Cu-OG62, Pb-OG62, Zn-OG62 and ME-OG62 analysis packages.

For QA/QC purposes, Anglesey Mining used the industry standard of inserting 5% Certified Reference Material (CRM) samples, 2.5% Certified Blank Samples (Blanks) and 5% duplicate samples at source. The CRMs were sourced from OREAS Australia.

Competent Person

The information in this announcement which relates to Drilling Results has been approved by Mrs. Liz de Klerk, M.Sc., Pr.Sci.Nat., FIMMM who is a professional registered with the South African Council for Natural Scientific Professionals (SACNASP: 400090/08) and independent consultant to the Company. Mrs. de Klerk is the Senior Geologist & Managing Director of Micon International Co Limited and has over 20 continuous years of exploration and mining experience in a variety of mineral deposit styles. Mrs. de Klerk has sufficient experience which is relevant to the style of exploration, mineralisation and type of deposit under consideration and to the activity which she is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the “Australasian Code for reporting of Exploration Results, Exploration Targets, Mineral Resources and Ore Reserves” (JORC Code). Mrs. de Klerk consents to inclusion in the announcement of the matters based on this information in the form and context in which it appears.

About Anglesey Mining plc:

Anglesey is traded on the AIM market of the London Stock Exchange and currently has 420,093,017 ordinary shares in issue.

Anglesey is developing the 100% owned Parys Mountain Cu-Zn-Pb-Ag-Au VMS deposit in North Wales, UK with a reported resource of 5.3 million tonnes at over 4.0% combined base metals in the Measured and Indicated categories and 10.8 million tonnes at over 2.5% combined base metals in the Inferred category.

Anglesey also holds a 49.75% interest in the Grängesberg iron ore project in Sweden and 12% of Labrador Iron Mines Holdings Limited, which through its 52% owned subsidiaries, is engaged in the exploration and development of direct shipping iron ore deposits in Labrador and Quebec.

For further information, please contact:

Anglesey Mining plc

Rob Marsden, Chief Executive Officer – Tel: +44 (0)7531 475111

Andrew King, Interim-Chairman – Tel: +44 (0)7825 963700

Davy

Nominated Adviser & Joint Corporate Broker

Brian Garrahy / Daragh O’Reilly – Tel: +353 1 679 6363

WH Ireland

Joint Corporate Broker

Katy Mitchell / Harry Ansell – Tel: +44 (0)207 220 1666

Brand Communications

Public & Investor Relations

Alan Green – Tel: +44 (0)7976 431608