Home » Posts tagged 'lithium' (Page 6)

Tag Archives: lithium

#TM1 Technology Minerals – Q&A: Building battery recycling capabilities

![]()

Technology Minerals is a London-based, LSE-listed company creating a circular economy for battery metals. The company, which is also engaged in extracting raw materials required for lithium-ion (Li-ion) battery cathodes, plans to increase its lead-acid battery recycling capability to 16,000 tonnes per annum by 2022, and 5,000 tonnes per annum for Li-ion batteries in the same time frame.

Robin Brundle, chairman of Technology Minerals plc, outlines TM’s plans to recycle batteries on an industrial scale.

We start full industrial-scale production in early 2022 with two plants, the first, which is currently being installed and will be ready for commissioning in January, is focused on lead-acid battery recycling. The second on lithium-ion battery recycling is now in a manufacture test phase and will be ready for commissioning in February 2022. The sites are both located in the Midlands.

Our recently announced partnership with Slicker Recycling provides a full UK footprint for safe custodianship of collection, of all types of li-ion batteries to our processing plants as we start to build front end inventory during 2022 and grow production. In addition, the wider Slicker group is also very strong in Europe offering a mirror image of the services they offer in the UK. So that could be, at the appropriate time, important for us as we build commercial relationships in Europe.

Can you explain how your recycling process works? How do you get the value out of the so-called ‘black mass’?

The process, for both lead-acid and li-ion, starts through our nationwide collection process and the safe delivery of the batteries to our processing plants in the Midlands.

The li-ion process is industry-leading, and we own the IP on both the process and the plant design. Our process safely deals with all five types of li-ion battery sciences and in any mix or combination at the same time. The plant is modular in design and thus cost effective and each plant can process 5,000 tones per year on a single shift basis. The plant is UK designed, UK manufactured and serviced by a UK company. What sets us apart is that our process does not use pyrolysis or saline solution, and this removes risk to the working environment.

On the lead-acid side, we are industrialising and mechanising a long-established industry that has traditionally been very labour intensive. The efficiencies of the plant combined with our processes really does modernise the sector and will assist in reducing the number of batteries that are either incinerated or worse still sent to landfill.

With regard to black mass, we are working on an end solution for the UK market – it is notable that as it stands – the UK doesn’t currently have the capability to process the black mass back to its constituent parts.

Until the UK has this capability, we have global offtake partners with whom we have already shared testing samples from our process. We already have these offtake partners in place as we build black mass production through 2022.

Are your processes patented and do you intend to license them?

On the li-ion plant, we are currently reviewing our patent applications for both the plant and the process. We are focused on retaining our early to market advantage and will take the necessary steps to do so. The final design and build of the plant have taken nearly two years and is testament to the engineering innovation that we have to hand in such depth in the UK.

UK set for industrial scale battery recycling

On the lead-acid side, we are currently writing a new process to surpass any previous patents that exist. The plant has been sourced from the UK, Europe and Brazil and takes circa eight months from order to completion.

What relationship do you have with Gigafactories?

We have a number of ongoing discussions with the battery OEMs which are at various stages of maturity, and also the tier one auto manufacturers to become their respective partners of choice. Certainly, we aim to build out our plants in line with customer requirements and, where appropriate, creating a bespoke recycling capability on-site which utilises the benefits of our modular processing plant and technology.

You are currently looking at Li-ion batteries from EVs. Do you plan on using other sources (laptops, tablets etc) of battery?

This proprietary process enables us to put all five sciences of lithium-ion batteries through our process, whether that is from portable devices, laptops, e-bikes, through to the heavier end of automotive and energy stations. Each battery type has a slightly different science, and our process allows us to safely recycle any combination through to the output of the ‘black mass’ material, which is rich in a number of the key metals which goes onto the final process of refining back to their respective form.

What markets are you targeting?

Because of the ability of the process to handle all five sciences in lithium-ion batteries we are not restricted as to sector or industry, from the perspective of local authorities looking for safe handling and recycling, through to the automotive OEMs, fleet management and auto dealership networks we have the logistic solution and the re-purposing and then recycling engineering process that really does embrace a circular economy solution for end-of-use and end-of-life batteries.

More broadly, what percentage of your mined products do you expect to introduce into the mix over time?

Our whole strategy is focused on the circular economy, and specifically in the battery sector, and as such we are targeting 100 per cent of all materials being used, be that mined or recycled.

The focus for our recycling operation longer term is on the UK and European markets with a view to grow to 20,000 tonnes of lithium-ion batteries and 60,000 tonnes of lead-acid batteries respectively per annum over the next decade.

The largest market opportunity is in the automotive industry, with 800,000 tonnes of battery per year, equating to ~70 per cent of the battery market in Europe

Lead-acid is the largest battery type with 831,000 tonnes, comprising over 72 per cent of the battery market in Europe.

#TM1 Technology Minerals – UK EV battery recycling hots up with Technology Minerals

15 years from now, it is estimated there will be some 250,000 tones of spent EV battery packs, and they all have to go somewhere.

Thankfully, EV batteries aren’t nuclear waste; we can recycle them to extract raw materials and reuse those materials to make more batteries.

Like the plastic trays and milk bottles you throw in the bin, used EV batteries are recycled to separate the useful minerals from the chaff. This not only reduces our dependency on virgin materials but slashes carbon emissions in the supply chain.

The recycling process shreds the EV batteries, creating a black mass, which consists of high amounts of lithium, manganese, cobalt, and nickel metals. Those metals are refined further to create a fresh supply of rare and uncommon metals.

Battery recycling for electric vehicles includes both the main battery pack and the 12V battery, which can be lead-acid or lithium-ion.

The ultimate goal is to create a closed-loop manufacturing process. In November, Northvolt announced the world’s first 100% recycled EV battery.

UK EV battery recycling

In the UK, battery recycling facilities are relatively common, but facilities that recycle EV batteries are not. You see, EV batteries are enormous, and they have a different chemical composition to the batteries in your smartphone, requiring different recycling and refinement processes. The process is expensive and difficult.

Technology Minerals PLC, a British company, aims to change this as the UK’s first listed company to create a circular economy in the battery metals sector.

They aim to achieve this with proprietary recycling technology and a partnership agreement with a leading hazardous waste company, working closely with them to design and develop recycling facilities that can recycle EV batteries at scale.

The deal will see Recyclus Group, a 49% Technology Minerals owned company, partner with hazardous waste management and service delivery provider Slicker Recycling. The partnership will boost recycling output for lithium-ion batteries with a high level of refinement, preserving the quality of the extracted metals with great efficiency.

“There is a clear demand building as a result of this quantum shift to electrification,” says Alex Stanbury, CEO of Technology Minerals.

“We are focused on extracting raw materials required for lithium-ion batteries, whilst solving the ecological issue of spent Li-ion batteries, by recycling them for re-use by battery manufacturers.”

The demand for electrification is only going to increase, and we have to come to terms with the battery waste this will create.

The move by Technology Minerals is the first of its kind in the UK and a welcome step in the right direction for EV battery recycling.

Cadence Minerals #KDNC – European Metals #EMH Resource Upgrade at Cinovec Lithium Project.

Cadence Minerals (AIM/AQX: KDNC; OTC: KDNCY) is pleased to note that European Metals Holdings Limited (“European Metals” “EMH”) has announced final drill results and an upgraded mineral resource estimate for the lithium and tin resources in the Cinovec Lithium-Tin deposit in the Czech Republic.

EMH has recently completed a drilling campaign at Cinovec South, comprising 22 diamond drill core holes for 6,622 metres, with the goal of increasing resource certainty in the existing resource model in and around the initial planned mining areas and upgrading part of the resource from the Indicated category to the higher confidence Measured category.

Highlights

- Re-classification of 53.3 million tonnes ( MT ) into Measured resource category grading 0.47% Li2O and 0.08% Sn.

- 5 MT of Inferred resource upgraded to Indicated resource category

- The Measured and Indicated resource has increased from 372.4 to 413.4 MT @ 0.47% Li2O and 0.05%Sn .

- The total Measured, Indicated and Inferred resources have increased by 12.3MT to 708.2MT @ 0.43% Li2O and 0.05% Sn (0.1% Li (0.2153% Li2O) Cut-off).

- Increase in overall resource to 7.39 MT LCE

- Analysis received for final 10 diamond core holes in the Geomet s.r.o. drilling program including:

- Hole CIS-16 returned 101.7m averaging 0.59% Li2O, incl. 11.35m @ 0.85% Li2O

- Hole CIS-32 returned 61m averaging 0.66% Li2O and 0.17% Sn, incl. 30.5m @ 0.30% Sn

- Hole CIS-33 returned 113.3m averaging 0.54% Li2O, incl. 14.7m @ 0.60% Li2O

- Hole CIS-34 returned 111.4m averaging 0.54% Li2O and 0.13% Sn, incl. 21.15m @ 0.71% Li2O and 0.57% Sn

Link here for the full EMH announcement: https://www.londonstockexchange.com/news-article/EMH/resource-upgrade-at-cinovec-lithium-project/15171030

European Metals Executive Chairman Keith Coughlan commented; “The primary stated aim of this drilling program was to convert a larger portion of the resource to the measured category to provide greater certainty of the financial model and security to financiers. The results clearly indicate that the program has been successful and the robustness and consistency of the Cinovec resource further demonstrated. As we move closer to ultimate financing and offtake discussions, this higher degree of certainty provides more funding options for the project. Results from the final drill holes of the program have been in line with or better than expected.

“As we have reported previously, because zinnwaldite is paramagnetic, wet magnetic separation, the first stage of the ore processing has the effect of greatly increasing the grade of lithium oxide in the concentrate to approximately 2.85%. The zinnwaldite concentrate produced from Cinovec requires only roasting, compared to the calcination and roasting required of processing spodumene. This not only improves the economics, it will also have the effect of considerably reducing greenhouse gas emissions of the Project when compared to spodumene projects.”

Cadence CEO Kiran Morzaria added; “Today’s resource upgrade for total Measured, Indicated and Inferred resources adds greater value to Cinovec’s already exceptional potential as a future battery grade lithium supply hub for Europe and the rest of the world. Cadence are pleased to remain shareholders and supporters of EMH, and we look forward to further developments.”

Cadence Minerals Holding in EMH

Cadence holds approximately 9.7% percent of the equity in European Metals, which, through its wholly owned Subsidiary, Geomet s.r.o. (“Geomet”), controls the mineral exploration licenses awarded by the Czech State over Cinovec.

– Ends –

For further information:

| Cadence Minerals plc | +44 (0) 7879 584153 |

| Andrew Suckling | |

| Kiran Morzaria | |

| WH Ireland Limited (NOMAD & Broker) | +44 (0) 207 220 1666 |

| James Joyce | |

| Darshan Patel | |

| Novum Securities Limited (Joint Broker) | +44 (0) 207 399 9400 |

| Jon Belliss |

Qualified Person

Kiran Morzaria B.Eng. (ACSM), MBA, has reviewed and approved the information contained in this announcement. Kiran holds a Bachelor of Engineering (Industrial Geology) from the Camborne School of Mines and an MBA (Finance) from CASS Business School.

Forward-Looking Statements:

Certain statements in this announcement are or may be deemed to be forward-looking statements. Forward-looking statements are identified by their use of terms and phrases such as ‘‘believe’’ ‘‘could’’ “should” ‘‘envisage’’ ‘‘estimate’’ ‘‘intend’’ ‘‘may’’ ‘‘plan’’ ‘‘will’’ or the negative of those variations or comparable expressions including references to assumptions. These forward-looking statements are not based on historical facts but rather on the Directors’ current expectations and assumptions regarding the Company’s future growth results of operations performance future capital and other expenditures (including the amount. nature and sources of funding thereof) competitive advantages business prospects and opportunities. Such forward-looking statements reflect the Directors’ current beliefs and assumptions and are based on information currently available to the Directors. Many factors could cause actual results to differ materially from the results discussed in the forward-looking statements including risks associated with vulnerability to general economic and business conditions competition environmental and other regulatory changes actions by governmental authorities the availability of capital markets reliance on key personnel uninsured and underinsured losses and other factors many of which are beyond the control of the Company. Although any forward-looking statements contained in this announcement are based upon what the Directors believe to be reasonable assumptions. The Company cannot assure investors that actual results will be consistent with such forward-lookingstatements.

Cadence Minerals #KDNC – Option Granted to Castillo Copper (ASX/LON: CCZ) to Acquire the Litchfield and Picasso Lithium Projects in Australia.

Cadence Minerals (AIM/NEX: KDNC; OTC: KDNCY) is pleased to announce that Castillo Copper (ASX/LON: CCZ) (“Castillo”) has entered into a 90-day option agreement with Lithium Technologies Pty Ltd (“LT”) and Lithium Supplies Pty Ltd (“LS”), in which Cadence owns a 29% shareholding, to acquire – subject to due diligence – the Litchfield and Picasso Lithium Projects in the Northern Territory (NT) and Western Australia (WA) respectively.

Cadence Minerals (AIM/NEX: KDNC; OTC: KDNCY) is pleased to announce that Castillo Copper (ASX/LON: CCZ) (“Castillo”) has entered into a 90-day option agreement with Lithium Technologies Pty Ltd (“LT”) and Lithium Supplies Pty Ltd (“LS”), in which Cadence owns a 29% shareholding, to acquire – subject to due diligence – the Litchfield and Picasso Lithium Projects in the Northern Territory (NT) and Western Australia (WA) respectively.

Highlights:

- ASX and London listed Castillo has a 90-day option to acquire – subject to due diligence – the Litchfield and Picasso Lithium Projects.

- Consideration for 100% of the holding companies which hold these assets (plus others) is up to AUS$ 3 million in equity of Castillo.

- Castillo is an Australian-based explorer primarily focused on copper across Australia and Zambia. The group is embarking on a strategic transformation to morph into a mid-tier copper group underpinned by its core projects.

- The Litchfield Lithium Project is contiguous to Core Lithium’s (ASX: CXO) strategic Finniss Lithium Project which has JORC compliant ore reserves (7.4Mt @ 1.3% Li2O), with production slated to start in 2H 20221. There is potential for lithium pegmatite bodies along Litchfield’s north-west boundary.

- The Picasso Lithium Project in WA is proximal to Liontown’s Resources’ (ASX: LTR) Buldania Project, with a JORC compliant resource at 14.9Mt @ 0.97% Li2O3 and has mapped pegmatites that potentially host lithium mineralisation.

Cadence CEO Kiran Morzaria added: “The potential acquisition by Castillo provides Cadence with an exposure to developing copper assets which complements our already substantial lithium portfolio. Moreover, given Castillo’s established in country leadership and cash position we see this potential acquisition by Castillo as the best strategic approach to maximize returns for our shareholders. We look forward to seeing Castillo develop these assets further.”

Castillo’s Managing Director Simon Paull commented: “Acquiring prospective lithium projects, which complement the copper assets, arguably provides Castillo with a strong comparative advantage moving forward. In focusing on developing copper and lithium projects, the Board is positioning Castillo to potentially create significant incremental value from the transition towards renewable energy sources and accelerating demand for electric vehicles globally.”

Overview

LT and LS each own 50% of Synergy Prospecting Pty Ltd (“Synergy”) and have granted Castillo a 90-day option to acquire 100% of the outstanding shares of LT and LS and by implication 100% of Synergy.

During this 90-day period, Castillo will be conducting due diligence on all three entities to ensure the underlying assets are in good standing and there are no material adverse issues. Under the terms of the option agreement, Castillo can exercise its right to acquire LT, LS, and Synergy at any time during the 90-day period.

Castillo Copper Limited is an Australian-based explorer primarily focused on copper across Australia and Zambia. The group is embarking on a strategic transformation to morph into a mid-tier copper group underpinned by its core projects:

- A large footprint in the in the Mt Isa copper-belt district, north-west Queensland, which delivers significant exploration upside through having several high-grade targets and a sizeable untested anomaly within its boundaries in a copper-rich region.

- Four high-quality prospective assets across Zambia’s copper-belt which is the second largest copper producer in Africa.

- A large tenure footprint proximal to Broken Hill’s world-class deposit that is prospective for zinc-silver-lead-copper-gold.

- Cangai Copper Mine in northern New South Wales, which is one of Australia’s highest grading historic copper mines.

The primary assets of Synergy, which are wholly owned, comprise the Litchfield Lithium Project (EL31774) in NT and Picasso Lithium Project (E63/1888) in WA. In addition, Synergy has an application in NT – EL31828 – known as the Alcoota Lithium Project, which comprises ground proximal to Alice Springs. Castillo will need to undertake further geological due diligence on this application.

LT and LS also hold applications for six lithium properties in San Luis Province, Central Argentina. Again, Castillo will need to undertake further geological due diligence on these applications.

Further details on these assets and all the applications and permits are contained on our website here

Option terms & consideration

The terms of the 90-day option are as follows:

- A$50,000 non-refundable deposit in cash on formally granting the option that will go directly to Synergy for working capital purposes.

Upon exercising the option within the 90-day period, the binding consideration terms are as follows:

- A$1m script payment in CCZ shares will become payable to the Vendor Group based on the 14-day WVAP calculated from the date of which the option agreement is announced to the ASX. Note, the Vendor Group will be subject to a 6-month voluntary escrow period for 50% of the shares and 12-months for the 50% balance from the date of settlement. In addition, both parties agree to sign off on a binding term sheet.

Incremental consideration terms are applicable if the following milestones are achieved:

- A$1m script payment in CCZ’s shares to the Vendor Group based on the 14-day WVAP if two drill-holes produce assayed intercepts greater or equal to a true width of at least 10m @ 1.3% Li2O.Note, the two holes will be at least 100m apart, but not greater than 200m.

- A$1m script payment in CCZ’s shares to the Vendor Group based on the 14-day WVAP if a JORC compliant total inferred resource of at least 7Mt @ 1.3% Li2O is modelled by SRK Consulting.

- In the event of commercial mining operations commencing a 2% NSR will be payable to the nominees of the facilitator.

– Ends –

|

For further information: Cadence Minerals plc |

+44 (0) 7879 584153 |

|

Andrew Suckling |

|

|

Kiran Morzaria |

|

|

WH Ireland Limited (NOMAD & Broker) James Joyce |

+44 (0) 207 220 1666 |

|

Darshan Patel |

|

|

Novum Securities Limited (Joint Broker) Jon Belliss |

+44 (0) 207 399 9400 |

Qualified Person

Kiran Morzaria B.Eng. (ACSM), MBA, has reviewed and approved the information contained in this announcement. Kiran holds a Bachelor of Engineering (Industrial Geology) from the Camborne School of Mines and an MBA (Finance) from CASS Business School.

Forward-Looking Statements:

Certain statements in this announcement are or may be deemed to be forward-looking statements. Forward-looking statements are identified by their use of terms and phrases such as ”believe” ”could” “should” ”envisage” ”estimate” ”intend” ”may” ”plan” ”will” or the negative of those variations or comparable expressions including references to assumptions. These forward-looking statements are not based on historical facts but rather on the Directors’ current expectations and assumptions regarding Cadence Minerals Plc’s future growth results of operations performance future capital and other expenditures (including the amount. nature and sources of funding thereof) competitive advantages business prospects and opportunities. Such forward-looking statements reflect the Directors’ current beliefs and assumptions and are based on information currently available to the Directors. Many factors could cause actual results to differ materially from the results discussed in the forward-looking statements including risks associated with vulnerability to general economic and business conditions competition environmental and other regulatory changes actions by governmental authorities the availability of capital markets reliance on key personnel uninsured and underinsured losses and other factors many of which are beyond the control of Cadence Minerals Plc. Although any forward-looking statements contained in this announcement are based upon what the Directors

believe to be reasonable assumptions. Cadence Minerals Plc cannot assure investors that actual results will be consistent with such forward-looking statements.

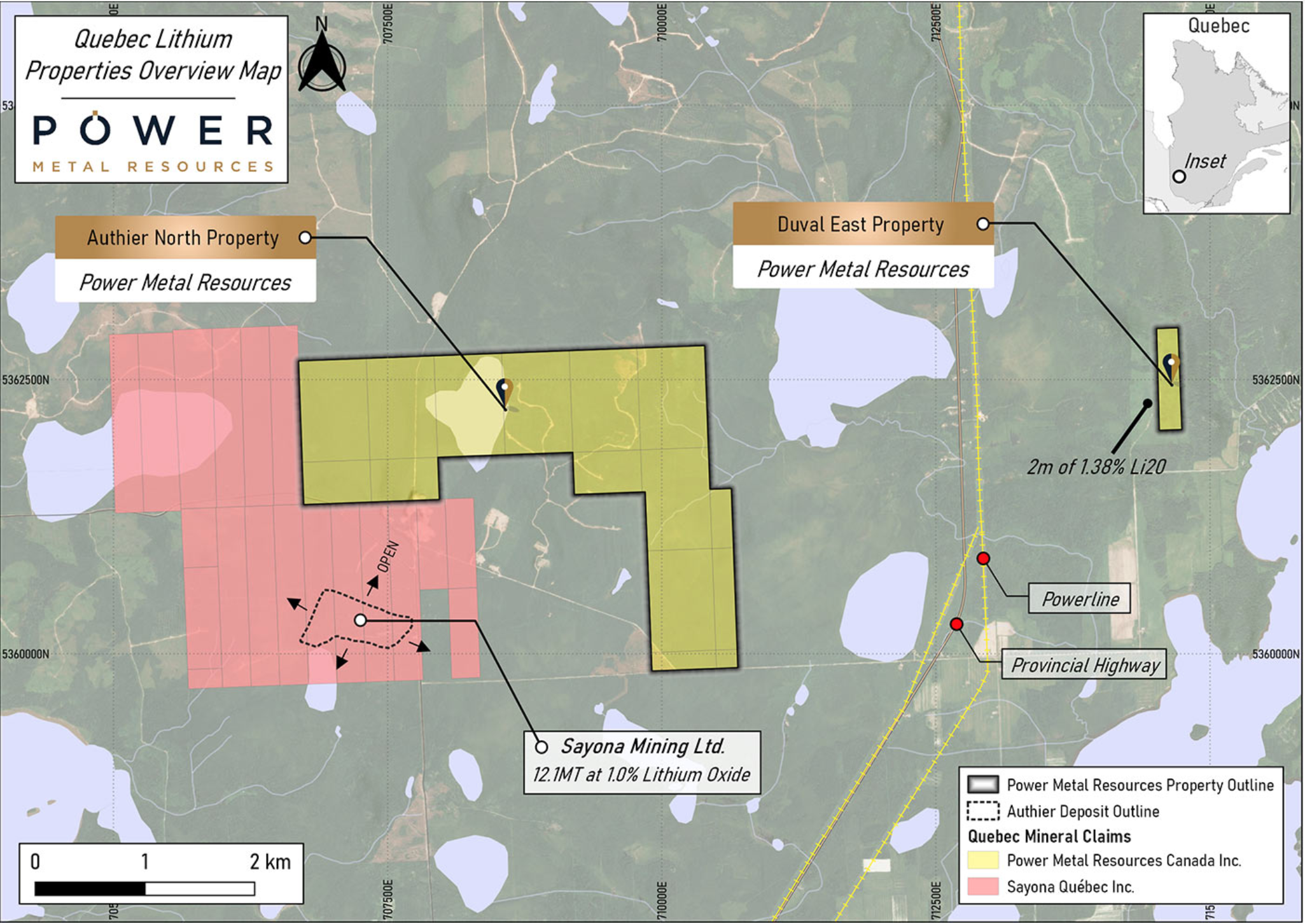

Power Metal Resources #POW – Canadian Lithium Project – Exploration Update

Power Metal Resources PLC (LON:POW) the London listed exploration company seeking large-scale metal discoveries across its global project portfolio announces the commencement of its Phase I work programme on the Authier North Lithium Property, located in the prolific Val D’Or mining camp in Quebec, Canada (“Authier North” or the “Property”).

The Authier North Lithium Property interest is held by Power Metal’s wholly-owned Canadian subsidiary Power Metal Resources Canada Inc. (“Power Canada”) which is focused on strategic energy metal opportunities within Canada’s top mining jurisdictions.

Power Canada is earning-in to a 100% interest in Authier North and further information in respect of this earn-in transaction is provided in the Company’s announcement dated 16 July 2021 in the link below:

https://www.londonstockexchange.com/news-article/POW/agreement-canadian-lithium-properties/15061434

Paul Johnson, Chief Executive Officer of Power Metal Resources plc, commented:

“Following on from yesterday’s news marking Power Canada’s move into uranium exploration, today we confirm the launch of inaugural exploration on the Authier North lithium property.

Authier North is a strategic lithium interest situated adjacent to Sayona Mining’s Authier Lithium Project in Quebec, Canada, where a substantial Lithium Oxide Reserve has been delineated.

The geological proposition is that the lithium mineralisation may potentailly extend into the Power Canada Authier North Property, and if so, that there is potential for a lithium discovery.

Because of this geological potential Power Metal have been eager to accelerate exploration and so we announce this first programme today, only two months after the Authier North transaction was originally announced to the Market.

We look forward to updating the market with the findings from this important work.”

Authier North Property Location

The Authier North Property is highlighted on a map held on the Company’s website which may be viewed on the following link:

https://www.powermetalresources.com/quebec-lithium-properties/

The Phase 1 Exploration Work Programme

Very little historic work has been completed on the Property, including no known work completed since the discovery and resource declaration at the nearby Authier Lithium Project held by Sayona Mining Limited (“Sayona”).

During the 2021 Phase I programme, prospecting and mapping will be completed by a senior geologist with extensive Quebec lithium-pegmatite exploration experience.

As part of the programme at least 180 soil samples will be collected from four separate grids within the Property.

Geological Rationale for the Work Programme

The soil sampling grids have been oriented within strategic areas of the Property, including high-resolution coverage over the east-west oriented volcanic rock packages which hosts Sayona Mining’s Authier Lithium Project less than 2.5km to the west along strike.

Soil sampling will also be completed to the north of the Authier Lithium Project where the extension of the lithium-bearing pegmatite is postulated to continue at depth under cover.

Programme Outcomes/Deliverables

The work programme currently underway will satisfy the first year work requirements as outlined in the Authier North earn-in agreement.

The final deliverable by the in-country geological consultants will also include a technical fieldwork report delivered in a NI43-101 compliant form.

Lithium Commodity Attractiveness

The price of spodumene (lithium bearing mineral found on neighbouring Authier Lithium Project) has surged over 140% this year to $990/t USD on the back of stronger than expected electric vehicle demand.1

Authier North Property – Background

The Authier North Property consists of fifteen (15) mineral claims covering an area of approximately 560-hectares and is considered to be prospective for lithium-pegmatites and base metal mineralisation.

Very little historic exploration has been completed on the Authier North Property, with reports of five short boreholes (four of which returned elevated lithium and nickel assays) and only 4 rock samples which returned strongly anomalous chromium and nickel results (up to 0.42% Cr203 (Chromium (III) Oxide), and 0.21% nickel). The reports related to drilling conducted in 19551 and 19742 undertaken by Lyndhurst Mining Limited and Cominco Limited. No reliance should be placed on this historical exploration as it is not known whether the historical exploration results noted above are reliable.

The Authier North Property shares an extended claim border with Sayona’s Authier Lithium Project which hosts a JORC (Joint Ore Reserves Committee) compliant Total Reserve of 12.1Mt at 1.0% Li2O (Lithium Oxide). The deposit is less than 700m from the shared claim boundary.

Sayona published a Definitive Feasibility Study (“DFS” reported 11 November 2019) on their flagship Authier Lithium Project. This DFS highlighted a net present value (discount factor 8%) of CAD$216 million and a pre-tax internal rate of return at 33.9%.

Additionally, in January 2021, Soyona announced a strategic partnership and offtake agreement with Piedmont Lithium Limited (ASX:PLL, Nasdaq:PLL) which includes a 25% ownership stake in Sayona Quebec (a wholly owned subsidiary of Sayona Mining), as well as 50% (60,000 tpa) offtake agreement for future production from the Authier lithium project. Sayona expects full commercial production of spodumene concentrate to commence in 2023.

Soyona Mining’s Authier lithium project consists of a spodumene pegamatitic intrusion which dips to the north and the Company believe that this may extend into the Authier North Property.

References:

1:

https://gq.mines.gouv.qc.ca/documents/EXAMINE/GM03267/GM03267.pdf

COMPETENT PERSON STATEMENT

The technical information contained in this disclosure has been read and approved by Mr Nick O’Reilly (MSc, DIC, MIMMM, MAusIMM, FGS), who is a qualified geologist and acts as the Competent Person under the AIM Rules – Note for Mining and Oil & Gas Companies. Mr O’Reilly is a Principal consultant working for Mining Analyst Consulting Ltd which has been retained by Power Metal Resources PLC to provide technical support.

This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 (“MAR”), and is disclosed in accordance with the Company’s obligations under Article 17 of MAR.

For further information please visit https://www.powermetalresources.com/ or contact:

|

Power Metal Resources plc |

|

|

Paul Johnson (Chief Executive Officer) |

+44 (0) 7766 465 617 |

|

|

|

|

SP Angel Corporate Finance (Nomad and Joint Broker) |

|

|

Ewan Leggat/Charlie Bouverat |

+44 (0) 20 3470 0470 |

|

|

|

|

SI Capital Limited (Joint Broker) |

|

|

Nick Emerson |

+44 (0) 1483 413 500 |

|

|

|

|

First Equity Limited (Joint Broker) |

|

|

David Cockbill/Jason Robertson |

+44 (0) 20 7330 1883 |

Cadence Minerals #KDNC – European Metals #EMH – Confirmation of Refining Process – Strong results from Locked-Cycle Tests.

Cadence Minerals (AIM/NEX: KDNC; OTC: KDNCY) is pleased to note that European Metals Holdings Limited (“European Metals” “EMH”) has today announced results of locked-cycle testwork, a metallurgical processing assessment conducted on ore concentrate extracted from the Company’s flagship Cinovec lithium project.

Highlights:

- Successful locked-cycle test (“LCT”) results further support the Cinovec project’s credentials to initially produce battery-grade lithium carbonate.

- European Metals has demonstrated that Cinovec battery grade lithium carbonate can be easily converted into lithium hydroxide monohydrate with a commonly utilised liming plant process.

- Six LCTs were planned but testwork was stopped after four cycles as the main process stream compositions had successfully stabilised.

- Battery grade lithium carbonate was produced in every LCT with lithium recoveries of up to 92.0% achieved in the four LCTs performed.

- The LCTs tested zinnwaldite concentrate from the southern part of Cinovec, representative of the first five years of mining.

- Improved fluoride removal process step further enhances project’s economic outcomes as a result of the regeneration and reuse of the ion exchange resins.

- Further optimisation work in hydrometallurgy processing steps expected to improve lithium recoveries from concentrate to >92.0%.

The Cinovec project, located on the German border of the Czech Republic, is the largest hard-rock lithium resource in Europe, containing lithium-bearing mica known as zinnwaldite which the Company intends to refine using a number of processes initially outlined in a Pre-Feasibility Study (“PFS”) (see ASX Announcement dated: 17 June 2019).

Link here for the full EMH announcement and detailed background on the locked-cycle tests: https://www.londonstockexchange.com/news-article/EMH/strong-results-from-locked-cycle-tests/14983163

European Metals Executive Chairman Keith Coughlan commented; “In a significant vote of confidence for our Pre-Feasibility Study, the proposed process methodology has been confirmed by excellent locked-cycle test results which also include new processes involving recycle streams. The robustness of the process was further confirmed by the stabilisation of the process streams, enabling the work to stop after only four of the six test cycles were completed. The recovery of up to 92% of the lithium in the zinnwaldite concentrate at this early stage of DFS testwork is very promising for increased recoveries during the planned process optimisation work. Further, an improved fluoride removal step which is cheaper and cleaner represents only the beginning of further optimisation work which we expect will result in greater lithium recoveries and even stronger economics for the Cinovec Project.

It is also encouraging to note that the process was as successful as that conducted during the 2019 PFS on the Central/NW part of the orebody, further underlying the consistency of the Cinovec ore body.

We look forward to providing further updates on the Definitive Feasibility Study work as it unfolds.”

Cadence CEO Kiran Morzaria added; “These locked-cycle test results further highlight Cinovec’s potential as a future battery grade lithium supply hub for Europe and the rest of the world. Cadence are pleased to remain shareholders and supporters of EMH, and we look forward to further developments.”

Cadence Minerals Holding in EMH

Cadence holds approximately 11% percent of the equity in European Metals, which, through its wholly owned Subsidiary, Geomet s.r.o. (“Geomet”), controls the mineral exploration licenses awarded by the Czech State over Cinovec.

– Ends –

For further information:

| Cadence Minerals plc | +44 (0) 7879 584153 |

| Andrew Suckling | |

| Kiran Morzaria | |

| WH Ireland Limited (NOMAD & Broker) | +44 (0) 207 220 1666 |

| James Joyce | |

| James Sinclair-Ford | |

| Novum Securities Limited (Joint Broker) | +44 (0) 207 399 9400 |

| Jon Belliss |

Qualified Person

Kiran Morzaria B.Eng. (ACSM), MBA, has reviewed and approved the information contained in this announcement. Kiran holds a Bachelor of Engineering (Industrial Geology) from the Camborne School of Mines and an MBA (Finance) from CASS Business School.

Forward-Looking Statements:

Certain statements in this announcement are or may be deemed to be forward-looking statements. Forward-looking statements are identified by their use of terms and phrases such as ‘‘believe’’ ‘‘could’’ “should” ‘‘envisage’’ ‘‘estimate’’ ‘‘intend’’ ‘‘may’’ ‘‘plan’’ ‘‘will’’ or the negative of those variations or comparable expressions including references to assumptions. These forward-looking statements are not based on historical facts but rather on the Directors’ current expectations and assumptions regarding the Company’s future growth results of operations performance future capital and other expenditures (including the amount. nature and sources of funding thereof) competitive advantages business prospects and opportunities. Such forward-looking statements reflect the Directors’ current beliefs and assumptions and are based on information currently available to the Directors. Many factors could cause actual results to differ materially from the results discussed in the forward-looking statements including risks associated with vulnerability to general economic and business conditions competition environmental and other regulatory changes actions by governmental authorities the availability of capital markets reliance on key personnel uninsured and underinsured losses and other factors many of which are beyond the control of the Company. Although any forward-looking statements contained in this announcement are based upon what the Directors believe to be reasonable assumptions. The Company cannot assure investors that actual results will be consistent with such forward-lookingstatements.

Cadence Minerals and the next Commodity Supercycle

There is little doubt that historians will conclude that the global impact of COVID-19 represents the worst crisis since the Great Depression. The pandemic is leaving deep and enduring scars on the global economy, taxing health and medical services to the limit, depriving children of education, while decimating sectors of commerce and industry and in particular leisure and travel.

But history has shown on numerous occasions that the indomitable human spirit has a remarkable capacity for survival and evolution amidst existential crises. As areas such as traditional High St retail and seem to be drawing to a close, sectors such as commodities and mining are booming thanks to a near perfect storm created in part by the COVID crisis.

In October 2020, the IMF stated that the total bill for the global pandemic would reach some $28tn (£21.5tn) in lost output. The rapid intervention by global Governments with rate cuts, looser monetary policies and fiscal stimulus have certainly avoided a financial catastrophe, but at the same time these actions have effectively weakened fiat currencies and increased demand for commodities.

Historically the consequences of such events invariably see a strong recovery in commodity markets. This factor was clearly in evidence as 2020 progressed, and as the COVID noose tightened, prices of commodities such as Iron Ore, Copper and Nickel, along with precious metals including Gold and Silver, all increased in value.

As a consequence, as 2020 progressed prices of commodities such as Iron Ore, Copper and Nickel, along with precious metals including Gold and Silver, all increased in value.

As a consequence, as 2020 progressed prices of commodities such as Iron Ore, Copper and Nickel, along with precious metals including Gold and Silver, all increased in value.

In the wake of the sharp economic contractions in 2020, the IMF forecast that only China was expected to emerge with any economic growth during the year. 2021 is set to be a different story however, and with the vaccine rollout accelerating globally, there are expectations for sharp recoveries across most of the leading economies. Added to this, the new $1.9tn stimulus package in the US from the Biden administration will see heavy investment into ageing US infrastructure. These factors should ensure sustained demand and pricing for iron ore and base metals.

There is also the revolution taking place within the automotive industry to consider. The move towards EV’s is accelerating rapidly, with a plethora of commitments from key automotive manufacturers such as Ford, Volvo, BMW and Jaguar to switch to electric only production in the next few years. This move of course sounds the death knell for the internal combustion engine, but at the same time is driving the cost of battery metals and component commodities such as lithium, nickel, cobalt and graphite

The net effect is that mining, specific commodities and minerals, along with the sector’s nebulous support service industries are undergoing a significant global resurgence. Projects considered uneconomical to develop, and that have remained dormant for years are returning to life, newly financed and fast tracked thanks to the array of modern desktop technologies, data and modelling tools.

Iron Ore

In a note published last December, Goldman Sachs outlined their expectations for another substantial deficit next year (27Mt, GSe), supported by a combination of gradually decelerating China steel demand growth, sharply re-accelerating demand for Western steel and tepid supply growth. GS added that the weighting of the 2021 deficit to the front half of the year points to fundamental support for a sustained price path higher over Q1 and Q2, revising near-term targets for the benchmark 62% iron ore price to 3M $140/t and 6M $150/t.

These numbers of course imply material upside longer term, and GS have also upgraded full year forecasts for 2021 to $120/t ($90/t previously) and for 2022 to $95/t ($75/t previously).

GS sees four core drivers supporting this bullish view:

- Chinese steel production has remained strong & production in 2021 remains supported by a healthy infrastructure and property project pipeline, alongside a resurgence in China’s manufacturing capex cycle and steel exports.

- With construction and heavy industry remaining relatively less affected by second-wave lockdowns, Western steel demand is also recovering ahead of expectations. Significant regional price strength in the US and Europe is likely to spur further blast furnace restarts (and hence iron demand) after an aggressive suspensions phase in 2020 contributed to the current steel supply shortfalls as demand recovers.

- Iron ore supply growth is likely to stagnate in 2021. The limited growth that exists next year is concentrated with Vale Brazil operations, which is why their recent substantive downgrade to production guidance has had such an outsized positive impact on price.

- Chinese mill iron ore inventories remain low, raising the prospect of restocking bursts through the year.

For Cadence Minerals, this bullish outlook for iron ore puts two very firm ticks in the box, firstly for what is widely regarded as the company’s flagship Amapa Iron Ore project in Brazil, and secondly the investment in ASX and TSX listed Macarthur Minerals, with whom Amapa shares numerous infrastructural and evolutionary similarities.

Amapa Project

Bringing a project the size and scale of Amapa back to life has as expected proved to be a complex and challenging process. Nonetheless, DEV Mineração, Cadence and Indo Sino Pty Ltd are reaching a legal settlement with the project creditors, and with the ruling in February by the Commercial Court of São Paulo that port operations and the shipment of iron ore stockpiles can begin, the company is set to take the first practical step towards bringing the project back to life, which will in turn bring benefits to the Amapa region in terms of employment, health and education.

Once the creditor settlement agreement has been signed, an initial $2.5m investment will be released from escrow, meaning that the Pedra Branca Alliance (Cadence & Indo Sino JV co) will own 99.9% of DEV, the owner of the entire Amapa mining and processing assets,. At this point Cadence will proportionately own 20% of Amapa. The next step will involve a further $3.5m investment following the granting of the necessary environmental licenses required to operate the mine, which will see Cadence move to a 27% stake, with an option to increase to 49% once project financing has been raised to complete recommissioning and commence production.

Last November Cadence completed an updated Mineral Resource Estimate for Amapa, which increased the 2012 Anglo American MRE estimate by 21% to 176.7 million tonnes (“Mt”) grading 39.7% Fe in the Indicated category. With a production capacity of 5.3Mt per annum, the survey also noted there was significant potential to increase the resource base after the completion of metallurgical and optimisation studies.

Lake Giles Iron Project

Cadence also has a stake (c1%) in ASX and TSX listed Macarthur Minerals, owner of the Lake Giles Iron Project near Kalgoorlie in Western Australia. The Lake Giles project consists of the Moonshine magnetite deposit and the Ularring hematite deposit, which together have an indicated Mineral Resource Estimate of 218Mt grading 27.5% Fe in the Indicated category.

Lake Giles and Amapa share many similarities in regard to facilities and production routes, and with the Feasibility Study already underway, Lake Giles has a 3.4 Mt per annum production target with potential to scale-up operations.

Lithium

A recent paper published by commodities expert Fastmarkets FB noted that global lithium supply was developing at accelerating pace due to strong and continually growing demand. In particular the demand for compounds used in lithium-ion (li-ion) batteries such as lithium carbonate and lithium hydroxide has prompted lithium producers to expand total production while diversifying their investments in different lithium operations to ramp up production and diminish asset risk.

Despite an effective over supply in 2018-2019 that saw a price moratorium and a 50% fall in the price of battery-grade lithium carbonate in China, the subsequent seismic shift to bring forward EV production and commitments from major automotive manufacturers around the world saw the price of Lithium in China surge to an 18 month high of $9450 per tonne in January 2021.

Despite an effective over supply in 2018-2019 that saw a price moratorium and a 50% fall in the price of battery-grade lithium carbonate in China, the subsequent seismic shift to bring forward EV production and commitments from major automotive manufacturers around the world saw the price of Lithium in China surge to an 18 month high of $9450 per tonne in January 2021.

The Fastmarkets’ research team expects global lithium demand to grow to at least 1.1 million tonnes per year of lithium-carbonate equivalent (LCE) by 2025 from an expected 300,000 tonnes of LCE in 2019, with Global lithium producers set to boost output year on year to maintain pace with growing demand. Despite this, as can be seen from the table above the numbers still don’t add up, with massive shortfalls projected by Benchmark Intelligence in lithium and other key constituent metals by 2030.

Over 2018, China emerged as the world’s leading lithium-processing hub with the rapid growth of companies like Ganfeng Lithium, which specialise in converting lithium concentrate from hard rock.

Cinovec – European Metals Holdings

The Cinovec project is the largest hard rock lithium resource in Europe and 4th largest non-brine resource in the world. Perfectly located to become the central lithium supply hub for the European EV industry, Cadence owns a 12% stake in AIM listed European Metals Holdings (EMH), which in turn owns 49% of the Cinovec project, (51% owned by utilities giant CEZ Group).

The Cinovec project is the largest hard rock lithium resource in Europe and 4th largest non-brine resource in the world. Perfectly located to become the central lithium supply hub for the European EV industry, Cadence owns a 12% stake in AIM listed European Metals Holdings (EMH), which in turn owns 49% of the Cinovec project, (51% owned by utilities giant CEZ Group).

Cinovec is a potential low-cost producer at the bottom of the cost curve, and will sustainably supply 25,267 tpa lithium hydroxide or 22,500 tpa lithium carbonate into the European battery market.

Sonora Lithium Project

Cadence is a 30% joint venture partner with Bacanora Lithium (BCN) on the Fleur Lease (Mexalit & Megalit) at the Sonora Lithium Project in Mexico. A completed feasibility study values Sonora Mexico at US$1.25bn NPV, with some of the lowest production costs at $4,000/t in the industry.

AIM listed Bacanora is focused on building a 35,000 tpa lithium carbonate operation at Sonora with 50% owner and take off partner Ganfeng Lithium.

Australia Hard Rock Lithium Projects

Cadence owns three dormant hard rock lithium assets in Australia. These are Picasso (Western Australia – WA), Litchfield (Northern Territories – NT) and Alcoota (NT) all of which are in regions with proven lithium mineralisation and supportive mining infrastructure.

The Litchfield project, located near Darwin (NT), has an exploration license granted and is contiguous to Core Lithium’s (ASX: CXO) territory. Core has a JORC compliant mineral resource of 8.55Mt @ 1.33% Li2O for its Finnis project (for all six deposits).

Yangibana Rare Earths Project

Operated by ASX listed Hastings Technology Metals, Yangibana is a substantial Rare Earths deposit near Gascoyne in Western Australia. Drilling and sampling have revealed high concentrations of Neodymium and Praseodymium (NdPr), essential components in permanent magnets used in electric vehicles.

Operated by ASX listed Hastings Technology Metals, Yangibana is a substantial Rare Earths deposit near Gascoyne in Western Australia. Drilling and sampling have revealed high concentrations of Neodymium and Praseodymium (NdPr), essential components in permanent magnets used in electric vehicles.

Cadence is a 30% joint venture partner with Hastings on part of the Yangibana Rare Earth Element Project. Probable Ore Reserves within the tenements held by Cadence are just over 2m tonnes with TREO of 1.66%.

The current mine plan anticipates production to start from the joint venture areas (Yangibana) in year 6.

A Key Role?

Around the world today there are countless mining exploration companies, commodity investors and mine operators with projects offering scope for development and potential for investment. The challenge with any project of this nature is matching the opportunity with the macro backdrop, projected demand for the commodity alongside capex vs. return, production routes, shipping and completion of cycle to bring the product to the customer.

Rarely if ever has the industry been presented with so compelling a backdrop for the commodity market as a whole. The significant global resurgence seen in the mining sector at present given is entirely sustainable given the level of asset purchases and spending by Governments to rejuvenate damaged economies and the inevitable resulting erosion in fiat currency value.

As economies emerge from the havoc wrought by the COVID virus and restrictions on spending are lifted, it is clear that in many cases demand will outstrip availability. This will apply almost without exception across the commodity spectrum – iron ore for steel to fund reconstruction – lithium, nickel, cobalt, graphite and rare earths to address the burgeoning demand for lithium-ion battery production.

![]() There is no doubt that the recovering global economy is embarking on the next great Commodity Supercycle. Many mining groups and commodity project investors will benefit from this phenomenon by owning the right projects, at the right stage of evolution at the right time. On the evidence available today, Cadence Minerals is certainly one of them.

There is no doubt that the recovering global economy is embarking on the next great Commodity Supercycle. Many mining groups and commodity project investors will benefit from this phenomenon by owning the right projects, at the right stage of evolution at the right time. On the evidence available today, Cadence Minerals is certainly one of them.

Mining.com – Lithium price in China surges 40% to 18-month high

Lithium prices are soaring in China on the back of heavy demand for lithium iron phosphate (LFP) batteries, a new report by battery supply chain research and price reporting agency Benchmark Mineral Intelligence shows.

Cadence Minerals #KDNC – European Metals #EMH – Cinovec Project – Measured Resource Drilling Update.

Cadence Minerals (AIM/NEX: KDNC; OTC: KDNCY) is pleased to note that European Metals Holdings Limited (“European Metals” “EMH” or “the Company”) has today announced initial results from its current nineteen hole resource drilling programme at the Cinovec Project. The current programme of work was announced by the Company on 10 August 2020 (Measured Resource Drilling Commenced). Drilling of twelve of the nineteen holes has been completed and the thirteenth hole is currently underway. Analytical results for first six of the drill holes from the Cinovec South deposit are reported.

Highlights:

- Completion of 12 of a total of 19 hole programme at the Cinovec Project.

- Interim results from first 6 holes in line with or better than expectations

- Cinovec contains the largest hard rock lithium deposit in Europe

- Cinovec is fully funded to final investment decision with approximately EUR 26.7m in Project Company currently

- EMH intending to become one of the lowest carbon footprint producers of battery grade Lithium Hydroxide and lithium carbonate in Europe

- Cinovec is situated within 250 km of numerous existing or proposed end users of battery grade Lithium chemicals

Given the relative ease of beneficiation of the Cinovec deposit through wet magnetic separation it was decided that it was important to report the drill results and the “in lab” beneficiation results. As reported to the market 21 October 2016 (Outstanding Lithium Recoveries at Coarse Grind) wet magnetic separation (“WMS”) achieved a near pure lithium mica concentrate grading 2.85% Li2O with a lithium recovery of 92%.

Results:

- Resource drill holes CIS-18, CIS-19, CIS-20, CIS-21, CIS-22 and CIS-23 have been completed including analytical reports.

- Resource drill holes CIS-24, CIS-25, CIS-26, CIS-28, CIS-29 and CIS-30 have been drilled with analytical results pending.

- Drilling of resource hole CIS-27 is currently underway.

- Hole CIS-18 returned 57m averaging 0.41% Li2O, incl. 5m @ 0.96% Li2O, 3 m @ 1.13% Li2O, 0.12% Sn (Tin) and 0.104% W (Tungsten), and 7 m @ 0.136% W.

- Hole CIS-19 returned 68.9m averaging 0.45% Li2O and 0.11% Sn, incl. 10.8m @ 0.75% Li2O, 10m @ 0.13% Sn, 2.25m @ 0.54% Li2O, 0.15% Sn and 0.13% W, 4m @ 0.95% Sn, and 2m @ 0.15% Sn.

- Hole CIS-20 returned 82.8m averaging 0.41% Li2O, incl. 8.9m @ 0.66% Li2O.

- Hole CIS-21 returned 76.3m averaging 0.55% Li2O, incl. 12m @ 0.81% Li2O.

- Hole CIS-22 returned 115.5m averaging 0.47% Li2O, incl. 3m @ 0.91% Li2O and 3m @ 0.87% Li2O, and 28m @ 0.27% Sn.

- Hole CIS-23 returned 98.6m averaging 0.51% Li2O, incl. 9.7m @ 0.92% Li2O, 1m @ 1.49% Li2O, and 2.9m @ 1.31% Li2O.

In all of the six holes, the upper section of the drilled ore body is elevated in tin. The best intercept was returned from the hole CIS-22, with an interval of 28m averaging 0.27% Sn. If considered no cut-off and internal waste, following tin intercepts were recorded: 29 m @ 0.1% Sn in CIS-18, 52m @ 0.14% Sn in CIS-19, 74m @ 0.06% Sn in CIS-20, 37m @ 0.1% Sn in CIS-21, 50.5m @ 0.17% Sn in CIS-22, 71.5m @ 0.09% Sn in CIS-23.

The current drill programme has been planned to define blocks of resource for the first 5 years of mining within the Cinovec-South area, with a goal to convert the resource from indicated to measured category. The holes have been terminated in ore consistent with the aim of targeting the first 5 years of resource blocks for the mine.

Link here for the full EMH announcement, detailed mineralized intercepts and lithology, and project background: https://www.londonstockexchange.com/news-article/EMH/drilling-report/14848789

European Metals Executive Chairman Keith Coughlan commented; “We are pleased to report that these interim results of the current drilling programme at Cinovec are either in line with, or better than our expectations. The primary purpose of the programme is to convert a larger portion of the resource to the measured category to provide greater certainty of the financial model and security to the financiers we are currently in discussions with. It is important to note that the first stage of the proposed process, the wet magnetic separation has the effect of greatly increasing the grade of lithium oxide in the concentrate to approximately 2.85%.

The zinnwaldite concentrate produced from Cinovec requires only roasting, compared to the calcination and roasting required of processing spodumene. The combined effect of not requiring calcination, energy intensification and use of natural gas is expected to considerably reduce greenhouse gas emissions of the Project when compared to existing spodumene projects.”

Cadence CEO Kiran Morzaria added; “These strong drilling results serve to highlight the overall quality of the Cinovec project, and the reason EMH has attracted a partner of the calibre and size of CEZ Group. With Cinovec set to play a key role in as a battery grade lithium supplier to the lithium market in Europe and Worldwide, Cadence are pleased to remain shareholders and supporters of EMH, and we look forward to further developments.”

Cadence Minerals Holding in EMH

Cadence holds approximately 12% percent of the equity in European Metals, which owns 49% of Geomet s.r.o. (“Geomet”), controls the mineral exploration licenses awarded by the Czech State over Cinovec.

– Ends –

For further information:

| Cadence Minerals plc | +44 (0) 7879 584153 |

| Andrew Suckling | |

| Kiran Morzaria | |

| WH Ireland Limited (NOMAD & Broker) | +44 (0) 207 220 1666 |

| James Joyce | |

| James Sinclair-Ford | |

| Novum Securities Limited (Joint Broker) | +44 (0) 207 399 9400 |

| Jon Belliss |

Qualified Person

Kiran Morzaria B.Eng. (ACSM), MBA, has reviewed and approved the information contained in this announcement. Kiran holds a Bachelor of Engineering (Industrial Geology) from the Camborne School of Mines and an MBA (Finance) from CASS Business School.

Forward-Looking Statements:

Certain statements in this announcement are or may be deemed to be forward-looking statements. Forward-looking statements are identified by their use of terms and phrases such as ‘‘believe’’ ‘‘could’’ “should” ‘‘envisage’’ ‘‘estimate’’ ‘‘intend’’ ‘‘may’’ ‘‘plan’’ ‘‘will’’ or the negative of those variations or comparable expressions including references to assumptions. These forward-looking statements are not based on historical facts but rather on the Directors’ current expectations and assumptions regarding the Company’s future growth results of operations performance future capital and other expenditures (including the amount. nature and sources of funding thereof) competitive advantages business prospects and opportunities. Such forward-looking statements reflect the Directors’ current beliefs and assumptions and are based on information currently available to the Directors. Many factors could cause actual results to differ materially from the results discussed in the forward-looking statements including risks associated with vulnerability to general economic and business conditions competition environmental and other regulatory changes actions by governmental authorities the availability of capital markets reliance on key personnel uninsured and underinsured losses and other factors many of which are beyond the control of the Company. Although any forward-looking statements contained in this announcement are based upon what the Directors believe to be reasonable assumptions. The Company cannot assure investors that actual results will be consistent with such forward-looking statements.