Home » Posts tagged 'lithium market'

Tag Archives: lithium market

Europe Thinks Like China in Building Its Own Battery Industry – Bloomberg

Article by Bloomberg – July 3rd 2019

- Governments working with industry and banks to spur technology

- At least $113 billion to be invested in battery supply chain

The European Union is starting to act like China when it comes to building the batteries that will drive the next generation of cars and trucks.

In the past few months, government officials led by European Commission Vice President Maros Sefcovic have joined with manufacturers, development banks and commercial lenders on measures that will channel more than 100 billion euros ($113 billion) into a supply chain for the lithium-ion packs that will power electric cars.

Germany and France are prodding for action out of concern that China is racing ahead in new technologies sweeping the auto industry. With 13.8 million jobs representing 6.1% of employment linked to traditional auto manufacturing in the EU, authorities want to ensure that manufacturers can pivot toward supplying electric cars and batteries.

“We are walking the talk,” Sefcovic said in remarks to Bloomberg. “We have overcome an initial resignation that this battle would be a lost one for Europe.”

A number of trends are catalyzing the program, starting with the determination by EU nations to rein in greenhouse gases and fight climate change. They’re increasingly focused on reducing pollution from diesel engines and alarmed at the head start Chinese companies have in greener technologies. French President Emmanuel Macron in February said he “cannot be happy with a situation where 100% of the batteries of my electric vehicles are produced in Asia.”

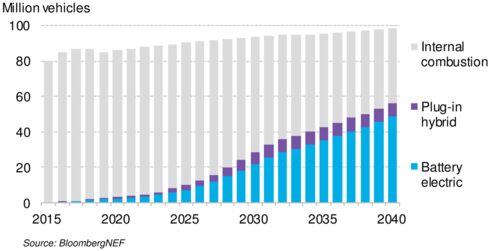

Drive Trains Go Electric

About 57% of cars will be driven by batteries by 2040, according to BloombergNEF research.

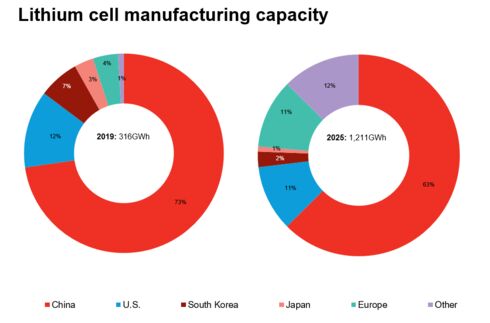

So far, the EU’s program is starting to work and putting Europe on track to wrest market share away from China. By 2025, European companies that currently lack a single large battery maker will rival the U.S. in terms of capacity, according to forecasts from BloombergNEF. Measures that will spur investment include:

- France and Germany are working on measures to channel billions of euros into the battery industry. Sefcovic has said the EC may be able to embrace the state-aid proposal as a special project by the end of October. The two nations are seeking to draw in additional support from Spain, Sweden and Poland.

- The European Investment Bank gave preliminary approval in May to a 350 million-euro loan supporting NorthVolt AB’s bid to build a battery gigafactory in Sweden after the company completed a fund raising.

- The EIB along with the European Bank for Reconstruction & Development are working on a “raw materials investment facility” that will help to build a supply chain for rare Earth metals needed for batteries, according to Sefcovic who says he hopes the program will be launched by the end of the year.

- The EU in May started a 100 million-euro Breakthrough Energy Ventures fund with Microsoft Corp. founder Bill Gates and other investors to advance the energy transition, which is likely to include batteries.

- The EC has gathered at least 260 industrial companies including Peugeot SA, Total SA and Siemens AG in an alliance aimed at building capacity to make the energy storage devices in Europe.

“A year or two ago, everyone was under the impression that it was already too late for Europe,” said James Frith, an energy storage analyst at BloombergNEF in London. “But they’ve made a commitment, and Europe is in a strong position now.”

By 2025, Europe may control 11% of global battery cell manufacturing capacity, up from 4% now, according to Frith. That will pare back China’s market share and rival the U.S. command of the industry. The EC estimates the battery market may be worth 250 billion euros a year by then. It estimates at least 100 billion euros already has been committed to battery factories or their suppliers in Europe.

Europe’s market share in battery making is set to grow to 11% by 2025 from 4% this year. Source: BloombergNEF

The goal is to build enterprises in Europe that could supply the region’s automakers without requiring imports from the major battery manufacturing centers in Asia. Currently, Contemporary Amperex Technology Co., or CATL, and BYD Co. dominate production in China. Elon Musk’s Tesla Inc. is also building battery gigafactories in the U.S.

So far, Europe has no established battery supply chain, though it has drawn investment in local factories from Korean firms including LG Chem Ltd. and Samsung SDI Co.as well as CATL.

The new ambition of the commission is to stimulate companies big enough to supply the likes of BMW AG and Volkswagen AG, which plan a massive increase in electric car production. Across the industry, the outlook is for a rising portion of cars to run on batteries in the coming years.

No single company will get the lion’s share of the investment or aid. Instead, dozens will benefit in addition to Peugeot and Total, which are building a cell plant in Kaiserslautern, Germany. Funds will also trickle into suppliers of parts or raw materials including Siemens, Umicore SA, Solvay SA and Manz AG.

Scarred by losing control of the solar industry in the last decade, Germany is leading the push. The nation was the biggest producer of solar cells in the early 2000s before Chinese companies backed by government loans took the lead.

When it comes to batteries, Economy and Energy Minister Peter Altmaier is focused on the 800,000 jobs in Germany tied directly to car manufacturing. Batteries account for about a third of the value of an electric car, and without facilities to make those in Europe, more jobs will go to Asia, Altmaier has said.

“There’s going to be huge demand in Europe for battery cells,” Altmaier said on ARD Television in June. “We must have the ambition to build the best battery cells in the world in Europe and Germany.”

Sefcovic envisions 10 or 20 “gigafactories” making battery cells across Europe and with his support the European Battery Alliance is seeking to coordinate research that will be the foundation of the plan. NorthVolt intends to be one of the major battery makers, feeding BMW and other major automakers.

“If we want to be one of the major manufacturers in Europe by 2030 we need to build about 150 gigawatt-hours of capacity,’’ said NorthVolt Chief Executive Officer Peter Carlsson. “The customer demand is so strong that we are accelerating our plans. We have taken a huge step on the way to create a new Swedish industry that will have a big impact in cutting our dependence of fossil fuels.’’

Lithium Boom – The World’s Hottest Commodity Just Got Hotter – Cadence Minerals (KDNC)

Lithium Boom – The World’s Hottest Commodity Just Got Hotter

Lithium Boom – The World’s Hottest Commodity Just Got Hotter

![]() Article includes excerpts from Oilprice.com, Lithium Investing news & other sources:

Article includes excerpts from Oilprice.com, Lithium Investing news & other sources:

Lithium is the hottest commodity on the planet right now. It is the most important component of electric vehicles, high-energy batteries, power storage, a vast menu of consumer electronics—and even Nirvana-reaching drugs.

Even today’s hyper-growth EV industry is just the tip of the iceberg compared with where it’s headed.

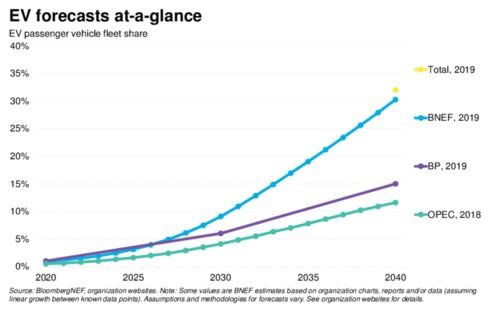

Bloomberg New Energy Finance predicts that 35% of all new vehicle sales by 2040 will be EVs, equivalent to 100 million units every year.

Tesla’s “halo effect” will make astute investors lifetime riches because that’s 100 times greater than current production.

All that growth will present some serious supply chain challenges. But in this massive opportunity, the key to everything is GRADE. Not all lithium is equal.

The majors can increase production, but only to a certain degree–and not nearly fast enough to meet growing demand. If you are looking for outsized gains on your lithium investment, you need to expand your horizon to new entrants with high-quality reserves.

High-grade lithium producers are where EVERY EV manufacturer will be looking as they seek to keep battery production costs low.

Below is a list of the top eight lithium-producing countries in the world.

- Australia – Mine production: 14,300 MT

- Chile – Mine production: 12,000 MT

- Argentina – Mine production: 5,700 MT

- China – Mine production: 2,000 MT

- Zimbabwe – Mine production: 900 MT

- Portugal – Mine production: 200 MT

- Brazil – Mine production: 200 MT

- United States – Mine production: Unknown

Prices of battery-grade lithium in China, the biggest Li-ion battery producer, surged above $20,000 per tonne in 2016–much higher than the global average.

Now, China has traditionally sourced its lithium from Australia, but increasing competition in the EV space and falling prices of EVs has forced it to look elsewhere for cheaper sources. Chile for example mines lithium from brines located just below easily accessible salt flats. The Atacama salt flat in Chile is the source of 37 percent of the world’s entire lithium production.

Chinese and Korean investors are already engaged in advanced talks with the Chilean government to open up a huge $2 billion Lithium battery plant to feed on the country’s rich lithium reserves. This could kick off an even more ferocious scramble for the precious metal–especially if China starts hoarding and puts further pressure on already constrained supplies.

But with rocketing demand, pressure is on to identify and exploit new resources. Plenty of opportunities exist. Japanese company Hanwa is a cornerstone investor into the Sonora lithium Project in Mexico to supply the fast-growing Asian battery market.

And operated by European Metals Holdings, the Cinovec lithium resource in the Czech Republic is expected to become the central lithium supply hub for European EV industry.

Low production costs are extremely important for EV manufacturers, now more than ever.

Batteries and power trains account for the biggest chunk of EV manufacturing costs. The high cost of these line items is the #1 reason why EVs have remained pricier than they could be. But advancements in battery technology have helped bring costs down–so much so that Tesla can now afford to offer the Model 3 for just $35,000, or half the price of an entry-level Model S.

Near-future demand is so overwhelming that we are in real danger of massive deficits. Current global Lithium-ion cell production can only supply 900,000-1 million electric vehicles.

Tesla is on course to kick off production of its first mass-produced vehicle–the Model 3– in July, and has already amassed 373,000 reservations. That’s five times the company’s 2016 sales.

Tesla has a goal to produce 500,000 Model 3s per year by the end of 2018, and could hit a million units as early as 2020. The company also sells home and industrial energy products, including Powerwalls. About 51Kg of Lithium goes into each Model S, while each Powerwall 2.0 unit packs 10Kgs of the metal.

Source: Visual Capitalist

Global production will ramp up more than 500 percent between 2016 and 2020, and while China will be doing much of the heavy lifting, the emerging resources in USA and Europe will all have a key role to play too.

Source: Visual Capitalist

By 2025, the battery market alone will be twice as big as today’s entire lithium market.

Therein, of course, lies the massive opportunity. Investors will want to identify owner / operator companies, and investment vehicles involved in a spread of risk – ranging from early stage resources to assets close to / in production. Time is of the essence though: these heady growth projections will be mirrored in stock price gains.

Excerpts from Oilprice.com article. Other sources Lithium Investing news:

Cadence Minerals (KDNC.L) is a unique early investment strategy & development firm, within the mineral resource sector. We identify undervalued assets, with irreplaceable strategic advantages. We invest in them and help turn them into powerhouses. Lithium and other technology minerals must get to market in order to achieve the global green revolution. We uncover new ways and places to extract and process these minerals, so that burgeoning demand is met; and our tomorrow is better.

Bonnie Hughes of Northland Capital Partners discusses Cadence Minerals (KDNC) on the Vox Markets podcast

Bonnie Hughes, Mining Specialist at Northland Capital Partners talks about Cadence Minerals (KDNC) with Justin Waite on the Vox Markets podcast.

Lithium market report 10-24 April – IndMin

![]()

By MARTIM FACADA

First published: Monday, 24 April 2017

The lithium market across the three major regional markets – the US, Europe and China – has been relatively stable in April so far, supported by continuous growth in the Chinese battery sector.

The Chinese domestic market – which has higher spot market activity than the other two western regions – continues to report high levels of activity due to demand from the booming domestic battery sector.

Lithium carbonate spot prices (min. 99-99.5% Li2CO3, CIF China) remain between $18-21/kg for lots of 20 tonnes of material while lithium hydroxide (56.5-57.5% LiOH, CIF China) continues to trade at $20.50-24/kg.

In the US and Europe, the market has remained fairly stable in April although it should be noted that lithium carbonate contract prices have moved up slightly on the low end.

Large biannual contracts for lithium carbonate (min. 99-99.5% Li2CO3, del. US and Europe) saw a small increase of $0.50/kg on the low end to $10.50-16/kg from $10-16/kg previously, while large quarterly contracts rose by $1/kg on the low end to $11-18/kg from $10-18 previously.

Persisting higher prices in China, bullish sentiment and tightness of lithium carbonate on the market were the main reasons cited to IM driving the small increase.

Meanwhile, spot sales in the US and Europe are being reported as high as $18/kg for lithium carbonate (min. 99-99.5% Li2CO3, del. US and Europe).

Lithium hydroxide (56.5-57.5% LiOH, del. US and Europe) contract prices remain unchanged at $14-20/kg.

Link to full article at IndMin website here