Home » Posts tagged 'IRON' (Page 3)

Tag Archives: IRON

#SVML Sovereign Metals moving rapidly ahead with what’s likely to become the largest rutile deposit in the world

Kasiya has significant green credentials, and plenty of goodwill locally too

It’s quite a selling point.

From an initial exploration programme designed to work up an attractive graphite play, Sovereign Metals Limited (ASX:SVM, AIM:SVML) is now well on the way to proving up what could shortly become the largest rutile deposit anywhere in the world.

For anyone not familiar with the mineral sands business, rutile is a significant source of titanium, a metal widely used in aerospace, clean-tech and medical applications, but which is mainly an essential component in paint pigments.

You can get titanium from ilmenite too, and in some cases rutile and ilmenite are found together. But the kicker is that it’s much more carbon and energy intensive to extract titanium from ilmenite than it is for rutile.

Sovereign’s Kasiya deposit in Malawi already boasts a resource of 605mln tonnes of ore grading 0.98% rutile, with significant graphite credits.

There are also areas of higher grade, which may well end up being mined first, and a sizeable and ongoing exploration programme which is likely to push the resource base from its current status as the world’s second largest rutile deposit to the world’s largest.

What’s more, just over half of that total resource has been booked in the indicated category, which adds a welcome a robustness to the modelling undertaken in the scoping study Sovereign completed at the end of last year.

This study envisaged an operation that would process 12mln tonnes of ore per year to produce 122,000 tonnes of rutile as well as 80,000 tonnes of graphite over a 25 year mine life.

That in turn would generate life of mine revenues of US$6.26bn, or US$251mln per year.

What’s more, the study was to a degree moderated by what can realistically be achieved by Sovereign itself as a junior to mid-tier miner. Accordingly, the capex for the operation as planned rings in at less than US$350mln.

What’s the likelihood that if a major company swooped in and bought Sovereign out it would create a still larger operation with bigger up-front costs and greater returns? Pretty good.

But at this stage, although there’s plenty of interest across the industry – how could there not be, with the world’s second largest rutile deposit? – there are no plans to sell.

For one thing, in its management team, Sovereign has a group of people who are more than capable of getting a mine built for themselves and, which is no small point, who have the in-country experience to do it.

For another, there’s still plenty more value to be added yet.

“We know we’ve got an eminently saleable and desirable product,” says Sovereign’s chairman Ben Stoikovich.

Indeed, that’s one of the first things he made sure got checked even before the resource base got built up. On his line of thinking, there was no point building a big resource if some serious testing of the material hadn’t been done first.

To that end he had a couple of tonnes of ore shipped out from Kasiya to Perth early in the process, and the results from the tests that were conducted ticked all the right boxes.

“Potential end-users and off-takers came to us as we published the specs,” he said. And from that point the company really knew it was onto something.

At the moment, there’s 129 square kilometres of known mineralization around Kasiya, although it could go bigger in due course. But there’s already so much of it that where mineralization occurs beneath or near known settlements, the current mine plan just carves out those areas and goes round them. Not too many mines can afford that kind of luxury, but in the case of Kasiya, social licence and economics aren’t really in conflict.

In fact, in Malawi, there’s a general hunger for major projects of the kind that Kasiya looks like developing into. Not too many junior miners operate there at the moment, but the ones that do – and investors will be particularly aware of Mkango – have found the jurisdiction to be welcoming and easy to work in.

The green credentials of the process of mining rutile help too, of course. Although the ground will be disturbed as the rutile is dug up, it will be returned in essentially the same form minus the rutile after the mining is complete. Rehabilitation in this way of doing things is a constant and ongoing process.

What’s more, because natural rutile is the purest natural form of titanium and requires very little processing after extraction, its carbon footprint is much smaller. From an ESG point, that’s a major tick. But it also works from the point of view of the economics too.

Typically at the moment, rutile sells for around US$1,350 per tonne, whereas ilmenite sells for just US$200 per tonne. The reason? – buyers know they’ll incur significant processing costs when they buy ilmenite that they won’t incur when buying rutile.

So why doesn’t everyone just mine rutile?

The answer is that there aren’t that many pure rutile deposits around. Sierra Rutile has one, but are there any others? Not really.

“It’s hugely rare,” says Stoikovich.

And that’s all to the good.

“We only know of one other deposit like this,” he adds.

“And for each tonne of rutile you’re saving up to 2.8 tonnes of carbon. So if a paint producer bought our product they could literally claim that what they are selling is low carbon paint. Rio Tinto is one of the biggest participants in this market. They produce predominantly ilmenite, which they smelt in South Africa using coal-fired power.”

So, with all this potential the plan is now to complete a pre-feasibility study by the end of this year, a process which will also run in parallel with environmental and social impact assessment programmes.

And while all that’s going on, guess what? – analysts expect the global supply of rutile to decline by 70% between 2017 and 2030 – or 8% per year. The timing couldn’t be better for a project like this, and it will be interesting to watch it run.

Read here – https://www.proactiveinvestors.com.au/companies/news/974623/sovereign-metals-moving-rapidly-ahead-with-what-s-likely-to-become-the-largest-rutile-deposit-in-the-world-974623.html

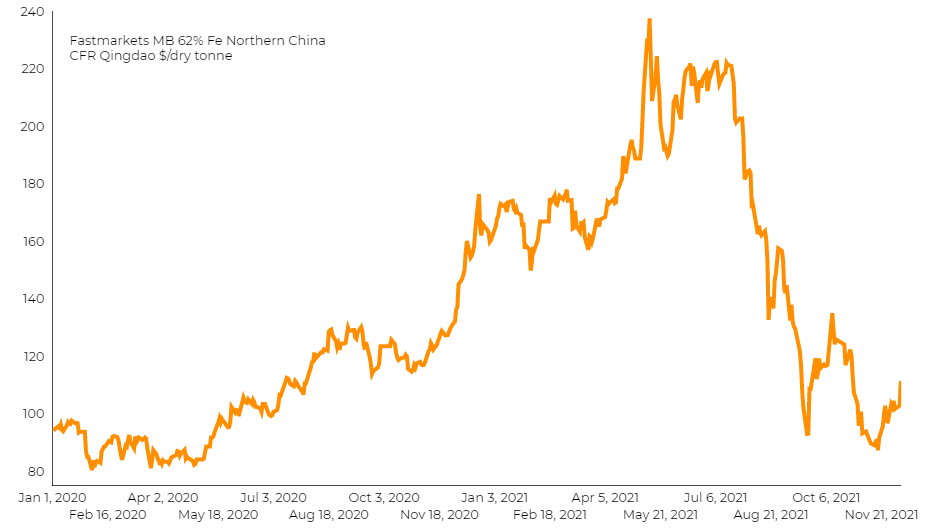

#KDNC Cadence Minerals – Iron ore price rockets as China imports hit highest in 16 months – Mining.com

Iron ore price surged on Tuesday after customs data showed China’s iron ore imports rose 14.6% in November from a month earlier to hit their highest since July 2020.

The world’s biggest consumer of iron ore brought in 104.96 million tonnes last month, up from October’s imports of 91.61 million and were also up 6.9% from November 2020, data from the General Administration of Customs showed.

According to Fastmarkets MB, benchmark 62% Fe fines imported into Northern China were changing hands for $111.34 a tonne, up 8.8% from Monday’s closing.

“November imports data could be affected by the customs clearance factor,” said Tang Binghua, an analyst with Founder CIFCO Futures in Beijing, adding that shipments and arrivals of iron ore did not change significantly in recent months.

“But it is unlikely that high levels of imports will continue, as consumption is weak after China stepped up output controls on mills during the heating season and ahead of the Winter Olympics.”

“The surprise in import growth was driven by a rebound in commodity volume, probably reflecting improving infrastructure capex demand as local governments stepped up stimulus toward the turn of the year,” said Michelle Lam, greater China economist at Societe Generale SA in Hong Kong.

Stocks of imported iron ore at Chinese ports grew for 10 straight weeks, jumping last week to 155.5 million tonnes, the highest since mid-2018, data from consultancy Mysteel showed.

In the first 11 months of the year, China imported 1.04 billion tonnes of iron ore, down 3.2% from the corresponding period a year earlier.

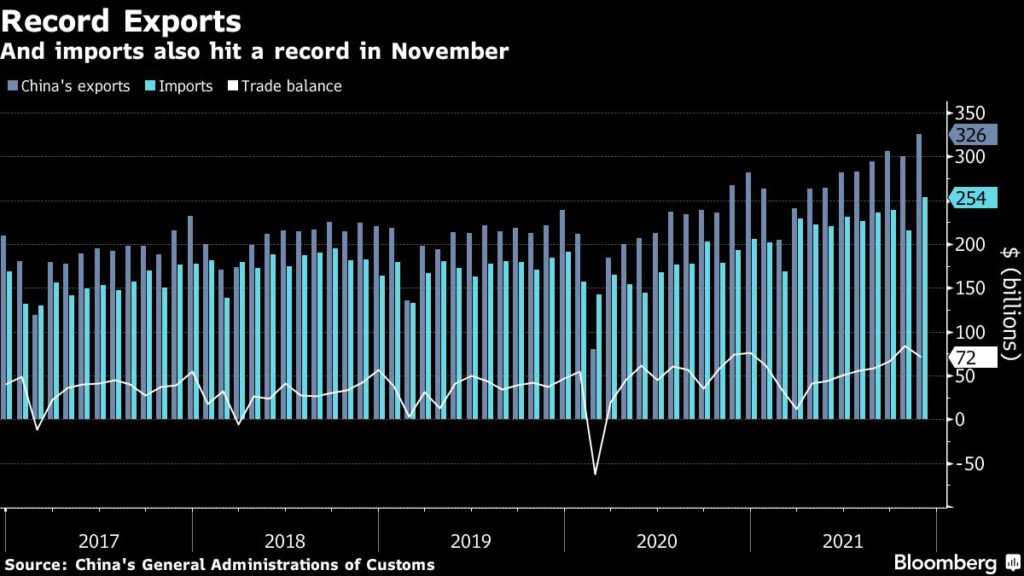

China’s total imports grew almost 32% to about $254 billion. Economists had forecast imports to increase by 21.5%.

Exports also rose 22% in dollar terms from a year earlier to almost $326 billion.

Read the article on Mining.com

Quoted Micro 31 October 2016

ISDX

ISDX

Via Developments (VIA1) says the Canal Street project in Manchester should be completed next March, while another Manchester site is attempting to gain enhanced planning permission that would enable 71 apartments to be built. Via expects deposits of 15% of the purchase price of the eight flats in Canal Street before the end of 2016 and this should generate £329,000. The Napier House project in Luton has been granted permitted development for 26 one-bedroom apartments. Additional planning permissions for an extra floor and a change to the facade of the building have been submitted. Via has received firm commitments for £1m of additional 7% debenture stock. This will take the debentures in issue to £4.5m.

Ganapati (GANP), the developer of apps for social media and games, reported an increase in its interim loss from £7.47m to £8.41m following the opening of a London office. Revenues fell from £2.3m to £1.34m. A unrealised foreign exchange loss of £5.71m on Yen borrowings. Management hopes that the Yen bonds in issue will be extended when they come up for repayment. There was £1.5m in the bank at the end of July 2016 but Ganapati wants to raise more money via a share issue to invest in further research and development. .

Ashford Borough Council has granted planning permission for the new Curious Brewery on a 1.6 acre site in the town centre. The Chapel Down Group (CDGP) brewing subsidiary raised money to build the brewery through crowd funding.

Miton Asset Management has increased its stake in rail safety products developer Wheelsure Holdings (WHLP) to 10.2% following the latest share subscription. WB Nominees has increased its stare to 9.2%, while JM Finn Nominees has raised its holding to 8.5%. Chief executive Gerhard Dodl increased his shareholding by 500,000 to 4.215 million shares, giving him 2.4% of Wheelsure.

AIM

Symphony Technology increased its offer for the remaining subsidiaries of Bond International Software (BDI) and the 121p a share bid by Constellation Software Inc has lapsed after gaining total acceptances of 47.4%. Constellation says that it will vote in favour of the disposal to Symphony for £22.8m. The proceeds and the other cash held by Bond will be distributed to shareholders as part of a liquidation process. Between 127p a share and 129.5p a share should be distributed with an initial distribution of at least 126p a share. Constellation originally bid 105p a share and it had acquired the majority of its 29.9% stake in Bond at 75p a share back in 2010.

Cyprotex (CRX) is recommending a bid from German drug discovery firm Evotec AG. The 160p a share cash bid values the contract pharma research services business at £41.7m. The share price has not been at the level of the bid since 2014. Cyprotex believes that it needs a partner to help it grow its operations further and Evotec will help it to grow in Europe.

Sunrise Resources (SRES) has revealed details of the results for the phase 2 drilling at the Bay Street silver project in Nevada. There was no positive news from this drilling and further exploration and drilling is required.

Eastern Europe-focused oil and gas explorer Ascent Resources (AST) has raised £3.5m via a placing at 1p a share and a further £1m via a loan note issue. Some of the cash will be used to repay a £871,510 loan facility from Henderson, which has also deferred the redemption of £8.2m of loan notes to 19 November 2019. The rest of the cash will complete the drilling of two wells and connect them with a refurbished central treatment station. This should enable Ascent to commence gas production by next spring and the gas will be initially be sold to Croatia.

South Africa focused miner Ironveld (IRON) is raising £1.8 at 4.5p a share with some of the cash going towards the development of the 15MW DC smelter for the iron, vanadium and titanium project in the Bushveld complex. The cash should last until next June and the shares come with a warrant to subscribe for another share at 6.75p for 12 months after the shares are issued. The Industrial Development Corporation has approved facilities of R244m for the project and negotiations continue for the remaining debt requirements. The total finance required is R841m. An offtake agreement has been finalised for the high purity iron powder that will be produced over a five year period from the commencement of production. Offtake agreements were already secured for titanium and vanadium.

Workforce optimisation software provider eg solutions (EGS) has won its first direct contract in Asia. The £500,000 contract is with a Singapore-based financial business and 50% of this will be recognised in the year to January 2017. This underpins the current expectations.

There has been further good drilling news concerning the Hot Maden project in Turkey, including some improvements in grade, and Mariana Resources (MARL) expects to report the preliminary economic assessment in late November. This assessment will provide the first guidance about the economics of the project.

Futura Medical (FUM) has raised £12m at 57p a share in order to fund the development of its portfolio of products. This includes the commercialisation of erectile dysfunction treatment MED2002 and trials for pain relief products TPR100 and TIB200. There was £2.9min the bank at the end of June 2016. Henderson will maintain its stake in Futura at just below 20%. The CSD500 condom has received European approvals for an extended shelf life of 18 months for the products manufactured in India. The European supplier has applied for the same shelf life extension.

Arian Solver Corporation (ACQ) has extended the exclusivity period for the Notche Buena gold silver tailings project in Mexico until 27 December. Recovery levels have been poor even though gold grades have been commercial so more tests are required. Arian is assessing an advanced silver exploration project in the US.

Share (SHRE) has made another add-on acquisition of customer accounts and the existing business is trading in line with expectations. The purchase of a book of 8,000 customer accounts with £200m under administration should be completed in April 2017. The Share Centre has maintained its market share of a peer group of brokers revenues, excluding interest, at more than 10%. In the third quarter, revenues were 7% ahead, while customer assets have increased by one-third to £3.6bn. Dealing commission and fee income have both grown but interest income fell by more than one-third. Share is still expected to make a small underlying loss this year.

MAIN MARKET

Nasdaq OMX-quoted AB Traction has increased its stake in engineering and environmental consultancy Waterman Group (WTM) to 14.3%. AB Traction went above 3% in April 2013 and has been building up the stake since then. AB Traction (www.traction.se) is an active long-term investor which does not focus on any particular sector. The strategy is to grow NAV.

Andrew Hore