Home » Posts tagged 'Iron Ore Prices'

Tag Archives: Iron Ore Prices

Iron ore price firm after BHP confirms lower exports – Financial Times

Price surge of steelmaking ingredient has created a huge cash windfall for big producers

Price surge of steelmaking ingredient has created a huge cash windfall for big producers

The price of iron ore remained above $120 a tonne on Wednesday after BHP Group, one of the world’s biggest suppliers of the steelmaking ingredient, revealed annual exports had declined for the first time this century.

In a trading update, the Anglo-Australian miner said it had shipped 270.5m tonnes of iron ore in the 12-months to June, down from 273.2m tonnes in 2018 — the first year-on-year decline in sales since at least 2000. Supply disruptions in Australia and Brazil and record steel production in China has seen the price of iron ore climb by almost 67 per cent this year to more than $120 a tonne, a level it last traded at in 2019.

The price surge has created a huge cash windfall for big producers like BHP and Rio, which at current prices are making more than $100 on every tonne of the commodity they ship to China, the world’s biggest consumers.

Both companies are tipped to announce big dividends when the announce results next month. At the start of its 2018/19 fiscal year, BHP expected to ship between 287m and 283m tonnes of iron ore but was forced to lower guidance after its mines in Western Australian were hit by a tropical cyclone and a major train derailment.

Rival Australian producer Rio has also suffered disruptions and has lowered its production forecasts twice since January. It expects to ship between 320m-330m tonnes of iron ore in 2019, down from 338.2m in 2018. Brazil’s Vale is also shipping less ore following a deadly dam disaster in January.

With BHP and Vale planning major maintenance programmes in September and October respectively, analysts reckon the iron ore market will remain tight. “BHP are expecting a modest production increase of 1 per cent to 6 per cent in 2020 [273m to 286m)”, said Paul Gait, an analyst at Bernstein Research.

“A planned maintenance programme . . . aimed at improving productivity has temporarily put a pause on any potential volume growth in the system.” In a report issued this week, analysts at Deutsche Bank said iron ore prices would not “break” sustainably below the $100 a tonne level until the first half of next year and then remain around $80 until 2021.

“One of the key takeaways from our [recent] China trip regarded clear evidence of a positive trajectory for infrastructure investment activity in the second half of the year, and only a modest deceleration in new [housing] starts during the same timeframe,” wrote analyst Nick Snowdon. “This points to a relatively healthy demand setting for iron ore in the second half of the year.”

In its trading update, BHP said it was likely to record $600m of exceptional items or charges to cover the costs of decommissioning a tailings dam in Brazil and redundancy costs. The company also flagged a $1bn hit from the impact of declining copper grades and the train derailment.

Iron Ore Is On A Hot Roll – Seeking Alpha

Summary

Summary- The S&P GSCI Iron Ore has been on a tear this year, up 72.47% YTD as of June 13, 2019, breaking through the previous high from May 22, 2019.

- Iron ore supply is concentrated in a handful of geographic regions and controlled by a small number of players, and demand is dictated by one major end-user (China).

- Both supply and demand are subject to shocks caused by geopolitical events, unforeseen natural disasters, and policy decisions, as well as the actions of individual asset owners.

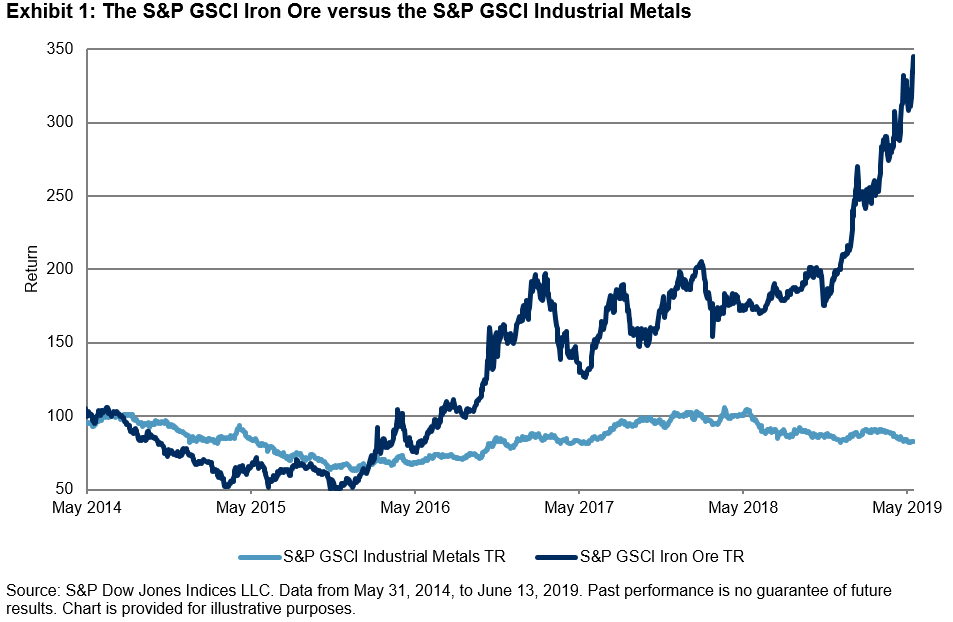

The S&P GSCI Iron Ore has been on a tear this year, up 72.47% YTD as of June 13, 2019, breaking through the previous high from May 22, 2019. It had by far the best YTD performance out of any of the commodities indices in the S&P GSCI Series. This bullish performance during the first half of 2019 is a good example of how using commodities in a tactical way can boost returns for investors. The S&P GSCI Iron Ore was able to distance itself from other metals. For example, the S&P GSCI Industrial Metals was flat over the same period.

Prior to the recent rally, the S&P GSCI Iron Ore was relatively range-bound for two years due to competing macro themes. There are several factors to point to when explaining the recent YTD performance. First, the challenging risk-off environment in Q4 2018 left most assets finishing the year in the red. This allowed for neutral-to-bearish investor positioning entering 2019, especially for those commodities with a high beta to global markets and specifically to Chinese economic activity.

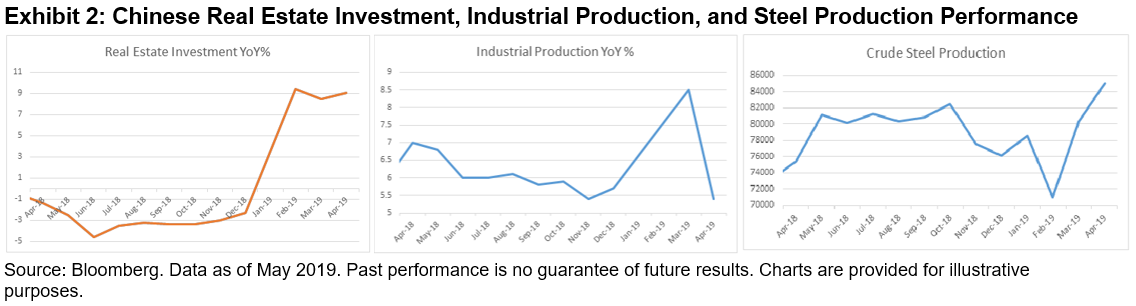

Second, to ease the burden of U.S. tariffs and to support the slowing economy, Beijing announced a variety of stimulus measures focused on boosting its industrial complex. China currently purchases approximately two-thirds of seaborne iron ore. As has been seen in the last few years with each China hard landing or global growth scare, the People’s Bank of China has not hesitated to turn on its most-adored stimulus levers. Those levers have historically been ways to increase funding for construction and infrastructure projects. While the planned move away from manufacturing to a more consumer-based economy continues to creep along in China, it will likely take a long time to implement this plan, and the Chinese administration appreciates that the current most effective way to support economic growth remains via these industrial support levers. The S&P GSCI Iron Ore is highly correlated to Chinese economic indicators such as real estate investment, industrial production, and steel production. Several of these indicators spiked in Q1 2019 just as iron ore prices started to rise (see Exhibit 2). It is worth noting that the most recent industrial production number dropped to a five-year low of 5%.

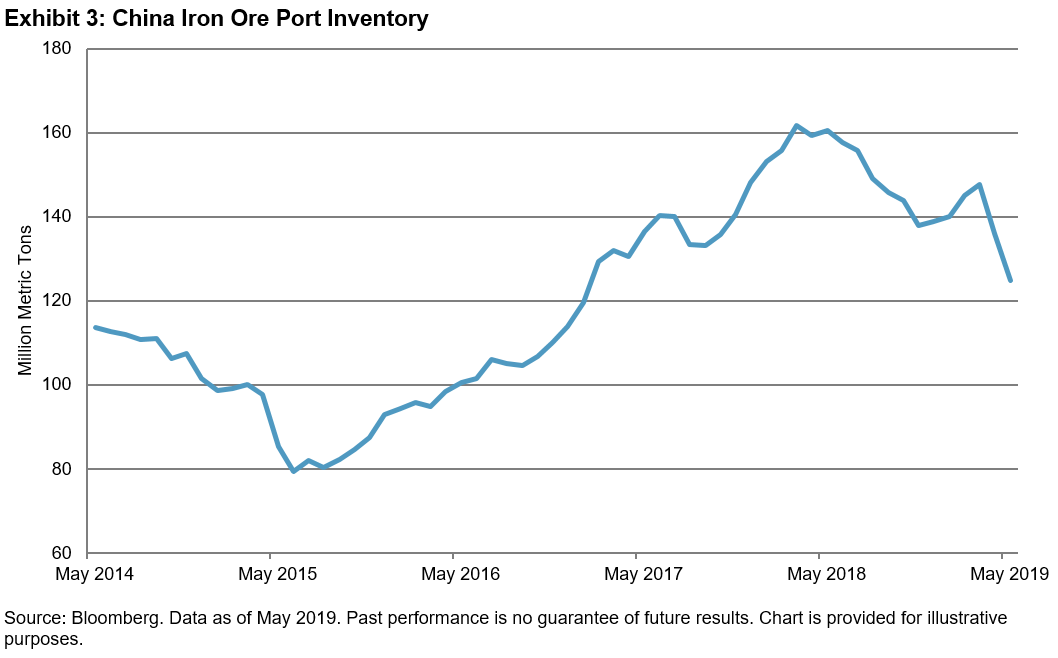

Third and most important, supply has been drastically curtailed in recent months. Inventories held globally have been reduced and are on pace to fall to five-year lows within the next few months. The Vale dam collapse in Brazil in late January 2019 and a cyclone in Australia in March 2019 reduced supply from the world’s two largest iron ore exporters. Shipments from Australia have largely returned to normal, but it is likely that Brazilian iron ore exports will be constrained for an extended period of time. Imported iron ore stock at Chinese ports fell to a 2.5-year low of 121.6mm metric tons in mid-June 2019 according to Steelhome.

The iron ore market has a number of characteristics that make it distinctive as an investable asset, but these characteristics are relatively common among commodities; iron ore supply is concentrated in a handful of geographic regions and controlled by a small number of players, and demand is dictated by one major end-user (China). Both supply and demand are subject to shocks caused by geopolitical events, unforeseen natural disasters, and policy decisions, as well as the actions of individual asset owners. However, with unique characteristics can come unique tactical investment opportunities for investors.

Disclosure: Copyright © 2018 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. This material is reproduced with the prior written consent of S&P DJI. For more information on S&P DJI please visit www.spdji.com. For full terms of use and disclosures please visit www.spdji.com/terms-of-use.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Iron ore prices surge on renewed uncertainty over Brazilian and Australian supply

![]()

Article by Business Insider – April 1st 2019

- Iron ore spot markets rose strongly across the board on Friday.

- Uncertainty over supply disruptions in Brazil and Australia, along with firmer steel prices, likely explain the size of the gains recorded during the session.

- China’s official manufacturing and non-manufacturing PMIs both improved in March compared to the levels reported in February.

- The Caixin-IHS Markit China manufacturing PMI report for March will be released on Monday.

Iron ore prices rallied on Friday, supported by renewed uncertainty over Brazilian and Australian supply.

According to metal Bulletin, the spot price for benchmark 62% fines jumped 2.5% to $86.81 a tonne, logging its largest gain in two weeks.

The gains in higher grades were even larger with 65% fines soaring 3% to $99.30 a tonne, leaving it just below the multi-year highs struck in early February.

Lower grades also rallied with 58% fines adding 1.6% to $72.14 a tonne.

The across the board gains coincided with renewed uncertainty over the outlook for Brazilian and Australian iron ore supply, two of the largest seaborne exporters globally.

On Thursday, Brazilian miner Vale lowered its iron ore sales forecasts to a range of 307 to 322 million tonnes this year, down from an earlier estimate of 382 million tonnes.

“The price implications from Vale’s guidance and commentary are significant,” said Vivek Dhar, Mining and Energy Commodities Analyst at the Commonwealth Bank.

“Given the physical nature of iron ore markets, the impending physical tightness to face iron ore markets strengthens our conviction that iron ore prices will rise above to over $90 a tonne in the short term.”

Daniel Hynes, Senior Commodities Strategist at ANZ Bank, is another who expects iron ore prices will remain supported in the period ahead.

“We see a sizable disruption lingering over the market for the near future,” he said, referring to supply disruptions in Brazil.

“Supply-side responses are likely, but will be far short of what is required to meet the needs of the market in 2019. As a result, iron ore exports will fail to meet expected demand by around 35–40 million tonnes in 2019.

“This should keep prices well supported in 2019.”

Along with uncertainty over the outlook for Brazilian supply, news of operational disruptions at facilities owned by Rio Tinto in Western Australia was another factor that helped to propel prices higher during the session.

On Friday, the miner issued force majeure notices to some iron ore customers due to damage from tropical cyclone Veronica, which hit Western Australia earlier this week, according to Reuters.

Rio said that it was “currently assessing the impact of the damage sustained at the Cape Lambert A port facility and is working with its customers to minimise any disruption in supplies”.

A force majeure is invoked when a miner cannot perform an obligation under a contract due to circumstances outside of its control.

Like spot markets, the news helped to spark a rally in Chinese iron ore futures on Friday.

In Dalian, the most actively traded May 2019 contract jumped to as high as 638.5 yuan before closing the session at 631.5 yuan. That was well above the 613.5 yuan level it finished on Thursday evening.

Stronger steel prices also helped to support iron ore futures at the margin with rebar and hot-rolled coil finishing trade at 3,758 and 3,741 yuan respectively, up from 3,695 and 3,673 yuan on Thursday evening.

As seen in the scoreboard below, those moves were largely sustained in overnight trade on Friday.

SHFE Hot Rolled Coil ¥3,732 , 0.67%

SHFE Rebar ¥3,754 , 0.72%

DCE Iron Ore ¥632.50 , 1.85%

DCE Coking Coal ¥1,229.00 , -0.08%

DCE Coke ¥1,980.00 , 0.23%

Trade in Chinese commodity futures will resume at midday AEDT on Monday.

In news that will likely bolster sentiment across the steel and bulk commodity complex further, activity levels across China’s manufacturing and non-manufacturing sectors improved in March, driven in part by booming construction activity.

The government’s manufacturing and non-manufacturing PMIs rose to 50.5 and 54.8 respectively in March, up from 49.2 and 54.3 in February.

A reading above 50 indicates that activity levels improved from a month earlier. The distance away from 50 reveals how fast the improvement occurred.

The separate Caixin-IHS Markit China manufacturing PMI report for March will be released today. In the past, markets have tended to pay more attention to this report than the official government release.