Home » Posts tagged 'Glencore Mining'

Tag Archives: Glencore Mining

Cadence Minerals Plc (KDNC) Approval of Judicial Restructuring Plan Paves the way for the Restart of the Amapá Iron Ore Project

Cadence Minerals (AIM/NEX: KDNC) is pleased to announce that the judicial restructuring plan (“JRP”) submitted to the commercial court of São Paulo to recover and restart operations at the Amapá iron ore project, was approved by over 90% of the credit value at the JRP meeting held in São Paulo and Macapá, Brazil and was homologated by the courts on the 29 August 2019.

Cadence Amapá Project stake

Once the preconditions relating to the railway licenses and bank creditor arrangements have been met, the US$2.5 million investment placed in the judicial trust account will be released, and Cadence will own 20% of the Amapá iron ore project. Cadence’s next stage of investment will be a further investment of US$3.5 million on the grant of all operational and environmental licenses for the Amapá Project, at which point Cadence will own 27%. Cadence also has first right of refusal to increase its stake to 49% in the Amapá Project.

Amapá Project Operational & Financial Plan Summary

The approval of the JRP and the fulfilment of the preconditions outlined above, will result in Cadence’s and IndoSino’s joint venture company Pedra Branca Alliance Pte Ltd. (“PBA”) owning 99.9% of DEV Mineração S.A. (“Amapá”). DEV Mineração S.A. is the owner of the Amapá iron project. The JRP approval will also allow Amapá to start operations at the project.

The approval of the JRP was a key step to Cadence’s investment into the Amapá iron ore project. The project was formerly owned by Anglo American plc (“Anglo American”) and Cliffs Natural Resources (“Cliffs”) and consist of a large-scale iron ore mine, beneficiation plant, railway and private port (“Amapá Project”). Before its sale in 2012 Anglo American valued its 70% stake at US $462m in its 2012 Annual Report (100% US $600m)

As part of the JRP Amapá submitted an outline of an operational and financial plan that Amapá intends to implement to bring the project back into production, which included the following

- The sale of approximately of 1.39 million tonnes (“Mt”) of stockpiles currently held at the port owned by Amapá. Planned shipment of stockpile commencing in December 2019.

- It is estimated that these stockpiles have a net realisable value of approximately US$ 60 million, which will be reinvested in the restart of the Amapá Project.

- Further capital investment of approximately US$168 million, of which it is estimated US$61 million will be spent on port rehabilitation and US$47 million to be spent on plant recommissioning.

- Rehabilitation to be completed by the end of 2021 with new production in 2022. Full production by 2024 of 5.3 million tonnes (“Mt”) of iron ore per annum.

- At full production and using US$61 per tonne of 62% Fe Amapá is forecast to have:

- an average net revenue after shipping of US$266 million per annum,

- and an average EBITDA of US$136 million per annum.

Next Steps

Cadence and IndoSino will continue their work to secure all the operating and environment licenses required to operate the Amapá Project. Initially this will focus on the reinstatement of the railway concessions and finalising negotiations with the secured bank creditors.

At site Amapá will put in place the company structures and controls required to start operations and recruit key personnel to implement the operational plan. Over the next four months our key targets will the start of detailed recommissioning studies and the start shipment of the stockpiles by the end of December 2019.

Cadence Non-Executive Chairman Andrew Suckling commented; “In my time working with commodity projects around the world, I have rarely if ever seen a lapsed mining project with this sort of potential. The JRP has provided a comprehensive framework to rehabilitate the Amapá Project from milling and crushing to transportation and final export. Without all these elements combined and packaged together by the JRP, rehabilitation would be impossible. On a global comparison, the rehabilitated mine is expected to be competitive and cash generative with conservative assumptions.”

“Cadence management, headed by Kiran have secured an opportunity to return this former Anglo American iron ore mine to production at a level enthusiastically supported by our board and institutional investors. There is a tangible sense of excitement and anticipation around our company and boardroom as we look forward to seeing the Amapá iron ore mine come back to life.”

Cadence CEO Kiran Morzaria commented; “For Cadence this a major step forward in the redevelopment of the fully integrated Amapá iron ore project. The overwhelming approval by the creditors for the operational and financial plan presented by Amapá, IndoSino and Cadence, was both gratifying to our team and a reflection of the strong underlying support experienced at numerous meetings with key stakeholders, creditors and state officials.”

“I would personally like to thank all involved including the legal teams*, engineers, state authorities and creditors who have worked together tirelessly to achieve this incredible first step. Cadence and IndoSino will now work on fulfilling the remaining preconditions, and I look forward to being continually and directly involved day to day as we move towards the restart of operations at the Amapá iron ore project.”

“As part of our desire to attract institutions to our Company and after positive discussions with our current institutional shareholder base, we announced, earlier this week, a proposed consolidation of our share capital”

*For Cadence Hill Dickinson LLP & Thomas Bastos Waisberg Kurzweil, for Amapá Donelli, Abreu Sodré e Martins Advogados and for IndoSino ACPA Advogados.

Details of the JRP

The information, assumptions and financial model, were prepared for the JRP only and are based on historical analysis of the costs and the review of two technical independent engineers reports published 2013 and 2015. It should be noted that this review provides a basis for a preliminary assessment of the project and its potential but further, more detailed reviews and analysis would be required to provide a Feasibility Study level report. This would include amongst other things, providing a current Mineral Resource Estimate and/or Ore Reserves, updated capital and operating costs and an independent assessment of key economic drivers and returns.

Cadence, IndoSino and Amapá submitted a JRP to the Commercial Court of São Paulo in May of this year. This plan set out a financial and operational plan to restart operations at the Amapá Project and under what terms Cadence and IndoSino will invest via its joint venture company in Amapá Project.

The creditors meeting was held on the 22 August 2019. The creditors approved the JRP and the results o were homologated by the commercial court of São Paulo on the 29 August 2019. The JRP is part of a regulated process under the laws of Brazil, in which the company under judicial review and investors can submit a recovery plan which will allow the company under judicial review, in this case, the Amapá, to trade under a protected status while it recovers from its financial difficulties.

The JRP has several key preconditions to the investment by PBA into Amapá; the first was the approval of the JRP, the others are the reinstatement of the railway concession to Amapá and the conclusion of an agreement with the secured bank creditors of payments from free cash flow. On the completion of these two remaining preconditions US$2.5 million (deposited by Cadence as part of the investment agreement with IndoSino) will be released from the judicial account to pay historic employee and small trade creditors. These conditions being fulfilled PBA will own 99.9% of the Amapá Project.

The JRP schedule contemplates the majority of the historic liabilities will be paid from free cash flow in years 5 to year 17 of operations, which represents a discounted NPV10 debt value of approximately US$106 million. The JRP also caps the trade creditor liabilities.

JRP Operational Plan

The JRP provides an operational and financial strategy for the redevelopment and restart of operations at the Amapá Project. The plan is based on historical minerals resource estimates and management estimates of operational and capital costs.

The key stages and economics of the redevelopment strategy are summarised below:

Recommissioning Studies

- Amapá will start the relevant resource, engineering studies required for banking finance of the project.

- It is anticipated that this will commend in the first quarter or second quarter of 2020 with completion in the second or third quarter of 2020.

- The commissioning of these studies will commence only after the grant of all operational and environmental licenses.

Reinvestment of Iron Ore Stockpile Sales.

- Amapá will begin shipping of the iron ore at stockpile as soon as possible. Based Amapá’ s current understandings this is targeted to start by the end of 2019 and take between 18 to 24 months to ship.

- An independent survey of these stockpiles indicates some 1.39 Mt (+/- 10%) of iron ore in three stockpiles with an average Fe grade of 62.12% (+/ 10%), which based a US$80 per tonne of 62% Fe would net Amapá a forecast US$60 million net of costs.

- These funds are to be reinvested in the capital development of the Amapá Project

Capital Investment

- Amapá’s current estimates of capital costs, which are based on 2013 engineering studies, is anticipated to be a total of US$168 million. This sum includes all the capital investment required to bring the mine, rail and port into full production.

- A summary of the key capital expenditure centres are outlined below

| Capital Item | US$ Millions |

| Processing Plant | 47.0 |

| Fleet Contract | 13.0 |

| Power (Transmission Line) | 5.0 |

| Overland Conveyor | 15.0 |

| Tailings Dam | 7.0 |

| Railway | 4.5 |

| Port Re-Construction | 61.0 |

| Environment | 2.3 |

| Contingency | 13.5 |

| Total | 168.3 |

- The above capital investment will occur after the completion of the recommissioning studies.

- The reconstruction is estimated to take approximately 18 months, which based on current estimates would mean the start of full operations in the fourth quarter of 2021 or first quarter of 2022.

Operational Plan

- Based on available historical mine plans and the independent engineers review the Amapá current mine plan envisages a mine life of 14 years.

- As mentioned above before the start of mining, the Amapá Project will also ship the iron ore stockpiles held at the dock by the end of December 2019 and continue for between 18 and 24 months.

- The mine is open pit and has a planned strip ratio of 0.9:1.

- The beneficiation plant consists of a crushing circuit followed by screening, flotation, thickener and filtering to produce a 65% Fe Pellet Feed and a 62% Fe Spiral Concentrate.

- The current mine plan would mean that the Amapá Project would produce at steady-state production an estimated 4.4 Mt of 65% Fe and 0.9 Mt of 62% Fe per annum. Currently steady-state production is expected to be reached in 2024.

- The intention is that these products would then be transported from the mine to the railhead by on-highway trucks along an unpaved road, a road haul distance of 13km. From the railhead, the products would then be transported 180km by rail to the port facility at Santana.

- The products would then be stockpiled at the port facility and mechanically loaded onto “Handymax” vessels which navigate the Amazon River out to sea and then transhipped onto larger “Capesize” vessels before the products are sold to the market. The products produced by the Amapá Project are well known in the market, especially in China where most of the historical production was sold.

- It is estimated that at steady-state production of 5.3 Mt of iron ore and utilising a 62% Fe price of US$61 / tonne (27/08/2019 price Fe 62% – US$90 / tonne) Amapá will have an average :

- US$266 million per annum of net revenue after shipping,

- US$90 million per annum in mine, processing and transport costs

- US$48 million per annum in environmental, sales and G&A expenses

- EBITDA of US$136 million per annum.

Details of the Agreement with Indo Sino

The agreement with Indo Sino is to invest in and acquire up to a 27% of a joint venture company PBA. The approval of the JRP will result in the transfer of equity of Amapá to the PBA and PBA will own 99.9% of the Amapá Project. Should Indo Sino seek further investors or an investment in PBA the agreement also provides Cadence with a first right of refusal to increase its stake to 49% in PBA.

To acquire its 27% interest Cadence will invest US$ 6 million over two stages in PBA. The first stage is for 20% of the PBA the consideration for which is US$2.5 million. The second stage of investment is for a further 7% of JV Co for a consideration of US$3.5 million. If Cadence is unable to complete the second stage of the investment or not exercise its right of first refusal under the terms of the Agreement, Indo Sino will have a twelve-month option to buy the shares in JV Co held by Cadence for 1.5 (1 ½) times the price paid by Cadence for such shares.

Cadence’s investment is conditional on several material pre-conditions, which include the grant of key operating licences and the release of bank securities over the asset. On completion of Cadence’s investment (not including the first right of refusal) our joint venture partner Indo Sino will own 73% of JV Co.

The Agreement also contains security and default clauses which if triggered causes an upwards adjustment mechanism to allow Cadence to either receive cash from JV Co or receive additional shares in JV Co. In the latter case Cadence’s shareholding in the JV Co will not go above 49.9%.

On completion of the US$ 6 million investment Cadence will have the right to appoint two members to a five-member board with the remaining three comprising of one member jointly appointed by Cadence and Indo Sino and two appointed by Indo Sino.

This news release is not for distribution to United States Services or for Dissemination in the United States.

– Ends –

For further information:

|

The information contained within this announcement is deemed by the Company to constitute inside information under the Market Abuse Regulation (EU) No. 596/2014

Qualified Person

Kiran Morzaria B.Eng. (ACSM), MBA, has reviewed and approved the information contained in this announcement. Kiran holds a Bachelor of Engineering (Industrial Geology) from the Camborne School of Mines and an MBA (Finance) from CASS Business School.

Forward-Looking Statements:

Certain statements in this announcement are or may be deemed to be forward-looking statements. Forward-looking statements are identified by their use of terms and phrases such as ”believe” ”could” “should” ”envisage” ”estimate” ”intend” ”may” ”plan” ”will” or the negative of those variations or comparable expressions including references to assumptions. These forward-looking statements are not based on historical facts but rather on the Directors’ current expectations and assumptions regarding the Company’s future growth results of operations performance future capital and other expenditures (including the amount. nature and sources of funding thereof) competitive advantages business prospects and opportunities. Such forward-looking statements reflect the Directors’ current beliefs and assumptions and are based on information currently available to the Directors. Many factors could cause actual results to differ materially from the results discussed in the forward-looking statements including risks associated with vulnerability to general economic and business conditions competition environmental and other regulatory changes actions by governmental authorities the availability of capital markets reliance on key personnel uninsured and underinsured losses and other factors many of which are beyond the control of the Company. Although any forward-looking statements contained in this announcement are based upon what the Directors believe to be reasonable assumptions. The Company cannot assure investors that actual results will be consistent with such forward-looking statements.

Cadence Minerals Plc (KDNC) – Macarthur Minerals (TSX-V: MMS) Closes Fully Subscribed Private Placement.

Cadence Minerals (AIM/NEX: KDNC; OTC: KDNCY) is pleased to note the announcement today from Macarthur Minerals (TSX-V: MMS) (“Macarthur”) that it has closed the previously announced private placement offering (the “Offering”) of US$6 million of secured Convertible Note (“Note”) on conditional acceptance.

Cadence Minerals (AIM/NEX: KDNC; OTC: KDNCY) is pleased to note the announcement today from Macarthur Minerals (TSX-V: MMS) (“Macarthur”) that it has closed the previously announced private placement offering (the “Offering”) of US$6 million of secured Convertible Note (“Note”) on conditional acceptance.![]()

The total placement closed with subscriptions totalling 600 Notes for gross proceeds of US$6,000,000 with attaching warrant offered for one fourth of the Commitment amount.

All securities issued under the Offering are subject to a restricted (or “hold”) period of four months and one day following the distribution date of the Note and Warrant, under applicable Canadian securities legislation.

Cadence holds approximately 9.8% of the issued equity interest in Macarthur, which is an Australian mining exploration company focused primarily on iron ore, nickel, lithium and gold in Western Australia. It also has a lithium project in Nevada, USA.

The full release can be found at: https://web.tmxmoney.com/article.php?newsid=8438990672161293&qm_symbol=MMS

This news release is not for distribution to United States Services or for Dissemination in the United States.

– Ends –

For further information:

|

Qualified Person

Kiran Morzaria B.Eng. (ACSM), MBA, has reviewed and approved the information contained in this announcement. Kiran holds a Bachelor of Engineering (Industrial Geology) from the Camborne School of Mines and an MBA (Finance) from CASS Business School.

Forward-Looking Statements:

Certain statements in this announcement are or may be deemed to be forward-looking statements. Forward-looking statements are identified by their use of terms and phrases such as ”believe” ”could” “should” ”envisage” ”estimate” ”intend” ”may” ”plan” ”will” or the negative of those variations or comparable expressions including references to assumptions. These forward-looking statements are not based on historical facts but rather on the Directors’ current expectations and assumptions regarding the Company’s future growth results of operations performance future capital and other expenditures (including the amount. nature and sources of funding thereof) competitive advantages business prospects and opportunities. Such forward-looking statements reflect the Directors’ current beliefs and assumptions and are based on information currently available to the Directors. Many factors could cause actual results to differ materially from the results discussed in the forward-looking statements including risks associated with vulnerability to general economic and business conditions competition environmental and other regulatory changes actions by governmental authorities the availability of capital markets reliance on key personnel uninsured and underinsured losses and other factors many of which are beyond the control of the Company. Although any forward-looking statements contained in this announcement are based upon what the Directors believe to be reasonable assumptions. The Company cannot assure investors that actual results will be consistent with such forward-looking statements.

Iron Ore Is On A Hot Roll – Seeking Alpha

Summary

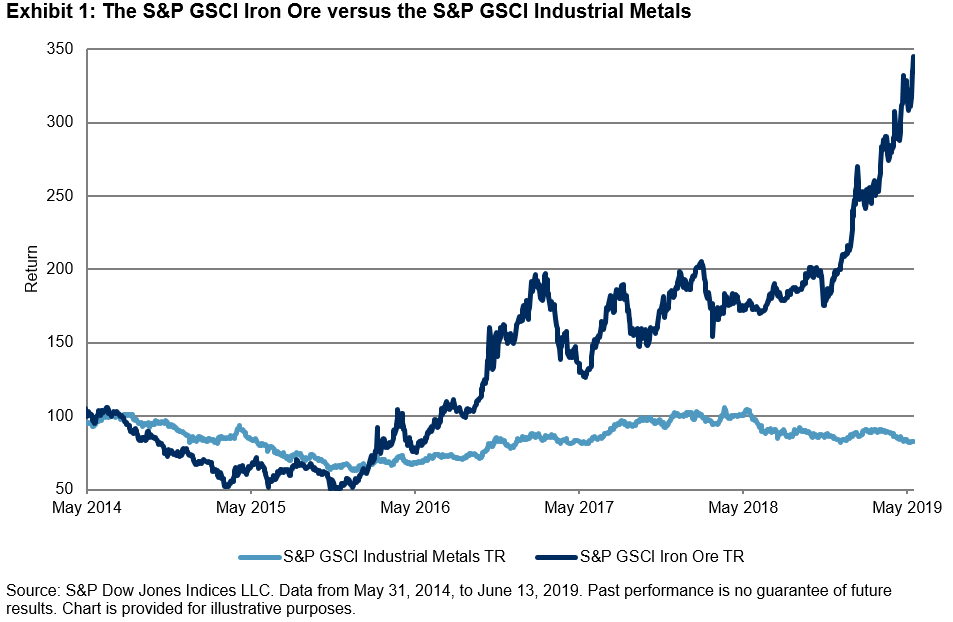

Summary- The S&P GSCI Iron Ore has been on a tear this year, up 72.47% YTD as of June 13, 2019, breaking through the previous high from May 22, 2019.

- Iron ore supply is concentrated in a handful of geographic regions and controlled by a small number of players, and demand is dictated by one major end-user (China).

- Both supply and demand are subject to shocks caused by geopolitical events, unforeseen natural disasters, and policy decisions, as well as the actions of individual asset owners.

The S&P GSCI Iron Ore has been on a tear this year, up 72.47% YTD as of June 13, 2019, breaking through the previous high from May 22, 2019. It had by far the best YTD performance out of any of the commodities indices in the S&P GSCI Series. This bullish performance during the first half of 2019 is a good example of how using commodities in a tactical way can boost returns for investors. The S&P GSCI Iron Ore was able to distance itself from other metals. For example, the S&P GSCI Industrial Metals was flat over the same period.

Prior to the recent rally, the S&P GSCI Iron Ore was relatively range-bound for two years due to competing macro themes. There are several factors to point to when explaining the recent YTD performance. First, the challenging risk-off environment in Q4 2018 left most assets finishing the year in the red. This allowed for neutral-to-bearish investor positioning entering 2019, especially for those commodities with a high beta to global markets and specifically to Chinese economic activity.

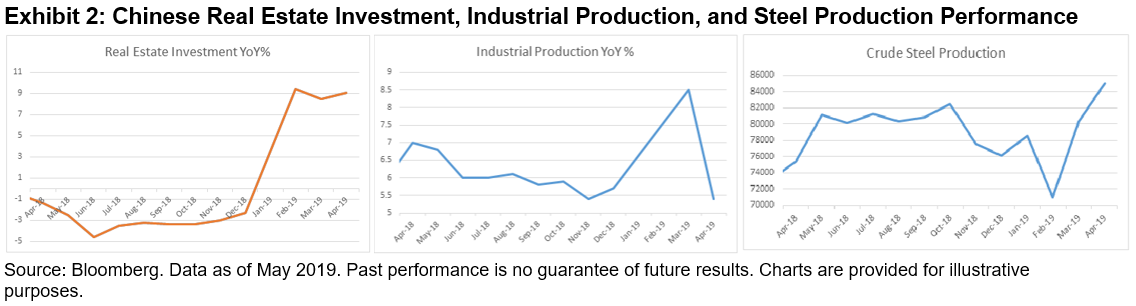

Second, to ease the burden of U.S. tariffs and to support the slowing economy, Beijing announced a variety of stimulus measures focused on boosting its industrial complex. China currently purchases approximately two-thirds of seaborne iron ore. As has been seen in the last few years with each China hard landing or global growth scare, the People’s Bank of China has not hesitated to turn on its most-adored stimulus levers. Those levers have historically been ways to increase funding for construction and infrastructure projects. While the planned move away from manufacturing to a more consumer-based economy continues to creep along in China, it will likely take a long time to implement this plan, and the Chinese administration appreciates that the current most effective way to support economic growth remains via these industrial support levers. The S&P GSCI Iron Ore is highly correlated to Chinese economic indicators such as real estate investment, industrial production, and steel production. Several of these indicators spiked in Q1 2019 just as iron ore prices started to rise (see Exhibit 2). It is worth noting that the most recent industrial production number dropped to a five-year low of 5%.

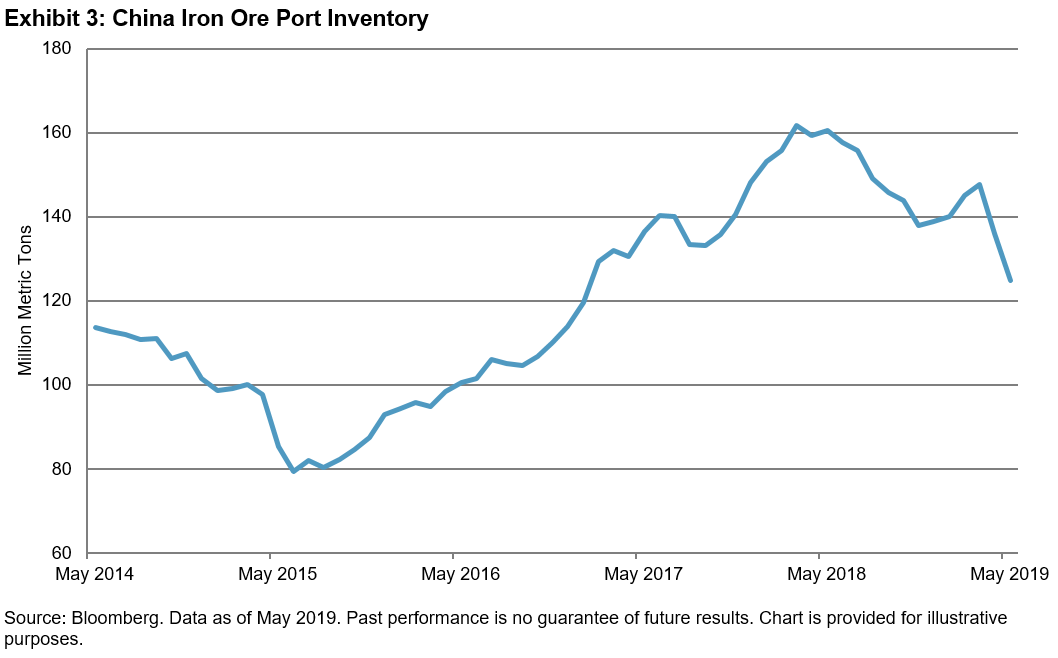

Third and most important, supply has been drastically curtailed in recent months. Inventories held globally have been reduced and are on pace to fall to five-year lows within the next few months. The Vale dam collapse in Brazil in late January 2019 and a cyclone in Australia in March 2019 reduced supply from the world’s two largest iron ore exporters. Shipments from Australia have largely returned to normal, but it is likely that Brazilian iron ore exports will be constrained for an extended period of time. Imported iron ore stock at Chinese ports fell to a 2.5-year low of 121.6mm metric tons in mid-June 2019 according to Steelhome.

The iron ore market has a number of characteristics that make it distinctive as an investable asset, but these characteristics are relatively common among commodities; iron ore supply is concentrated in a handful of geographic regions and controlled by a small number of players, and demand is dictated by one major end-user (China). Both supply and demand are subject to shocks caused by geopolitical events, unforeseen natural disasters, and policy decisions, as well as the actions of individual asset owners. However, with unique characteristics can come unique tactical investment opportunities for investors.

Disclosure: Copyright © 2018 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. This material is reproduced with the prior written consent of S&P DJI. For more information on S&P DJI please visit www.spdji.com. For full terms of use and disclosures please visit www.spdji.com/terms-of-use.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Mining Journal – Iron ore price to incentivise swing production, says BMO

Current iron ore prices of US$100/tonne should be enough to spark activation of about 60 million tonnes of swing production to “balance the market”, according to BMO, with perhaps 40Mt of that coming from China.

Current iron ore prices of US$100/tonne should be enough to spark activation of about 60 million tonnes of swing production to “balance the market”, according to BMO, with perhaps 40Mt of that coming from China.

BMO director, equity research, metals & mining – international, Edward Sterck, said a restart of Vale’s stalled 30Mtpa Brucutu mine in Brazil could restore 15Mt of production in the second half of this year. But there was no sign of a restart yet.

Global iron ore production has been impacted in the first half of 2019 by Vale’s dam failure at Brumadinho in Brazil, and the continuing legal issues around Brucutu, as well as weather and fire disruptions affecting Rio Tinto and BHP in Western Australia. BMO says shipping data suggests Rio Tinto and BHP are back on track, but Vale continues to struggle.

A need for 60Mt of swing production – US$6 billion of iron ore sales – could open up opportunities for Australian and other producers, though Sterck suggested to Mining Journal that higher production and earnings were “already baked in” to valuations.

“The iron ore price remains above our forecasts, suggesting upside potential to estimates,” he said.

“The high price should outweigh the supply disruption/shortfall [in the first half].”