Home » Posts tagged 'Australia gold mining'

Tag Archives: Australia gold mining

#POW Power Metal Resources PLC – Molopo Farms Complex Project Update

Power Metal Resources PLC (LON:POW), the London listed exploration company seeking large-scale metal discoveries across its global project portfolio announces an update in relation to the Molopo Farms Complex Project (“Molopo Farms” or the “Project”) targeting a large-scale nickel-copper-platinum group element (“PGE”) discovery in southwestern Botswana.

Power Metal Resources PLC (LON:POW), the London listed exploration company seeking large-scale metal discoveries across its global project portfolio announces an update in relation to the Molopo Farms Complex Project (“Molopo Farms” or the “Project”) targeting a large-scale nickel-copper-platinum group element (“PGE”) discovery in southwestern Botswana.

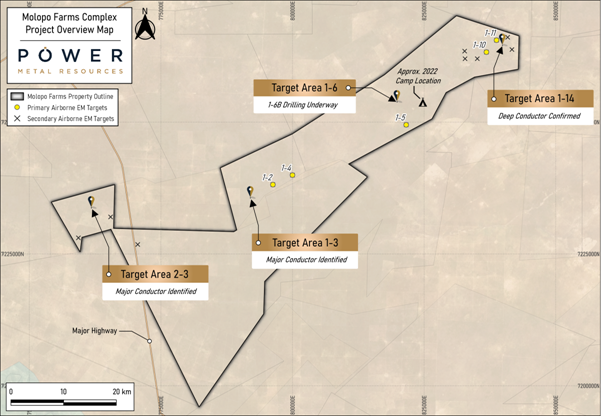

On 28 September 2022 the Company announced an update regarding the delineation of a second major conductor at target area T2-3, as well as an update regarding its ongoing geophysics programme. The link to this announcement is below:

https://www.londonstockexchange.com/news-article/POW/molopo-farms-complex-project-update/15647138

The above update noted that further analyses in respect of target (T1-3) were ongoing, the results of which are now covered below.

KEY HIGHLIGHTS

T1-3 Major Drill Target

– Final compilation and analyses of the ground-based moving loop electromagnetic (“MLEM”) and magnetic geophysical surveys over target area T1-3 are now complete.

– Geophysical inversion of the MLEM data has highlighted a significant ‘jelly-bean’ shaped, geophysical conductor at target area T1-3. This conductor remains open to the east-west and sits within a magnetic trough observed in both the ground and airborne magnetic surveys. No drilling has ever been completed over this target area.

– Historical airborne electromagnetic (“AEM”) data over T1-3 have been further analysed with results showing the MLEM conductor may extend out to 1.6km in an east-west direction, based on coincident airborne/ground survey anomalies.

– The T1-3 conductor has been given a high-priority (A+) ranking by the Company, the same priority attributed to the conductor at T1-6 (where drilling is ongoing) as well as the new conductor identified at T2-3.

– A planned 450m diamond core drillhole, DDH1-3A, has been designed to intersect the T1-3 conductor at approximately 300m downhole depth. The Company has added this hole to the list of holes to be drilled during the ongoing 2022 campaign. Considering the proximity of T1-3 to ongoing drilling at T1-6 (33km southwest), it is possible that T1-3 will be drilled after holes DDH1-6B and DDH1-6C complete, with drilling at T2-3 to follow (see map for relative locations).

Paul Johnson, Chief Executive Officer of Power Metal Resources commented:

“The inventory of high priority A+ ranked drill targets at Molopo are building and we now have the third, T1-3, added to the list. We plan to drill all three high priority targets during the current drill programme.

Our review has also identified further targets which we believe could become additional priority drill targets subject to additional technical work over those areas.

Each priority conductor identified to date, including T1-6, T1-3 and T2-3, are located proximal to a geological feeder zone but each possess unique size and scale dimensions. By drilling all of these targets, the Project becomes inherently de-risked, and the prospect of a discovery or discoveries increases.

Our attention is principally focused on drilling, with our first drill hole into the T1-6 conductor underway and I look forward to providing further updates at the earliest opportunity.”

GEOPHYSICAL SURVEY – OVERVIEW

– Spectral Geophysics have now completed the 2022 Phase I & II exploration programmes which included four MLEM and four magnetic geophysics surveys over targets T1-6, T1-14 and T2-3 and T1-3. The MLEM and magnetic survey results are assisting the company in refining further drill collar locations for the ongoing 2022 diamond drilling campaign.

– To date, the MLEM survey results have now highlighted:

o T2-3 (A+): A flat-lying, slightly concave (downward), conductor which remains open in all directions. Drilling is planned at this target.

o T1-6 (A+): A large, southerly dipping conductor which remains open towards the south, east and west. Drilling is ongoing over this target.

o T1-3 (A+): A ‘jelly-bean’ shaped conductor which remains open towards the east and west. Drilling is planned at this target.

o T1-14 (B): A conductor which is near-to the contact zone with known Transvaal carbonaceous mudstones. Due to the estimated depth required to reach this conductor (approx. 650m) and the geological complexity associated with this area, it has been given a lower priority ranking than T2-3, T1-6 and T1-3.

– The Company has also completed an in-depth review of a historical AEM report covering the majority of the Molopo Farms Complex Project. Considering priority areas T1-6, T2-3 and T1-3 were originally identified by the historical AEM survey results, it was decided that further investigation of the targets identified by this report were warranted. Significantly, five of the strong AEM conductors, including T1-2, T1-4, T1-5, T1-10 and T1-11 have been upgraded and are now classified as priority airborne targets by the Company. At T1-11, a 2020/2021 drillhole (KKME1-11) completed by the previous operator was determined to not have adequately targeted this conductor. The Company is in ongoing discussions with its geophysical contractor to determine next steps over these target areas.

FURTHER INFORMATION

Figure 1 – Molopo Farms Complex Project Plan Map: A plan map of the Project area, including the location of various elements mentioned above is outlined in Figure 1 below.

Figure 2 – Priority Target Area T1-3 3D View: A 3D view showing the location of the planned drillhole DDH1-3A and the MLEM results (new conductor in blue). The red-pink block model are magnetic inversion results showing the new ‘jelly-bean’ shaped conductor sits within a magnetic trough.

The diagrams and image presented above may also be viewed on the Company’s website through the following link:

https://www.powermetalresources.com/molopo-farms-major-drill-target-t1-3/

Further photographs and videos from the drill programme are and will be available on the Company’s website gallery section, through the following link:

https://www.powermetalresources.com/investors/gallery/molopo-farms-complex-botswana/

PROJECT BACKGROUND AND OWNERSHIP

Power Metal currently has a current circa 53% effective economic interest in Molopo, held through a direct project interest and a shareholding in partner Kalahari Key Mineral Exploration (Pty) Ltd (“KKME”). On 18 May 2022 Power Metal announced a conditional transaction that would see its interest in Molopo Farms increasing to 87.71% (the “Transaction”). The announcement may be viewed through the following link:

https://www.londonstockexchange.com/news-article/POW/kalahari-key-botswana-acquisition/15458701

As part of the Transaction, Power Metal will become the Project operator and in advance of completion the Company is working with the team at KKME to maintain momentum with regard to Project exploration.

Work streams are also in process to secure Botswana regulatory approvals enabling the Transaction to complete.

QUALIFIED PERSON STATEMENT

The technical information contained in this disclosure has been read and approved by Mr Nick O’Reilly (MSc, DIC, MIMMM, MAusIMM, FGS), who is a qualified geologist and acts as the Qualified Person under the AIM Rules – Note for Mining and Oil & Gas Companies. Mr O’Reilly is a Principal consultant working for Mining Analyst Consulting Ltd which has been retained by Power Metal Resources PLC to provide technical support.

REFERENCES

1: Power Metal PLC announcement, Molopo Farms Complex Project, Botswana – Major Drill Target T2-3

(https://www.londonstockexchange.com/news-article/POW/molopo-farms-complex-project-update/15647138)

This announcement contains inside information for the purposes of Article 7 of the Market Abuse Regulation (EU) 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 (“MAR”), and is disclosed in accordance with the Company’s obligations under Article 17 of MAR.

For further information please visit https://www.powermetalresources.com/ or contact:

|

Power Metal Resources plc |

|

|

Paul Johnson (Chief Executive Officer) |

+44 (0) 7766 465 617 |

|

SP Angel Corporate Finance (Nomad and Joint Broker) |

|

|

Ewan Leggat/Charlie Bouverat |

+44 (0) 20 3470 0470 |

|

SI Capital Limited (Joint Broker) |

|

|

Nick Emerson |

+44 (0) 1483 413 500 |

|

First Equity Limited (Joint Broker) |

|

|

David Cockbill/Jason Robertson |

+44 (0) 20 7330 1883 |

Mining Maven: Gold Nuggets, Discoveries, and Greenstone Potential: A Breakdown of ECR Minerals’ Australia Drilling Progress

Download the report here: ECR Report – Jun 2019

Download the report here: ECR Report – Jun 2019

Introduction

This year has seen ECR Minerals (LSE:ECR) launch an extensive exploration campaign across the highly popular Australian state of Victoria as it continues its search for multi-million-ounce gold deposits. Early signs of success have supported a substantial increase in the company’s share price from 0.75p to 1p, despite a harsh commodity market backdrop and weak investor sentiment in the UK, where it is based. Here, we break down ECR’s progress and plans at each of its Victoria prospects and outline its activity across the rest of Australia.

Gold Keeps Climbing – Mining Beacon

Mining Beacon April 17 2019

Recent research reports from S&P Global Market Intelligence highlight record gold production in 2018, and outline some of the reasons for the increased appetite for gold mergers and acquisitions.

Global gold production increased in 2018 for the 10th consecutive year to reach a total of 107.3 Moz, according to a recent report from S&P Global Market Intelligence (SPGMI). As signaled in the recent HindeSight bog, although the year-over-year increase of just under 1% was the smallest in the past decade, output of the precious metal has now risen 40% since 2008.

SPGMI forecasts further growth, of 2.3 Moz, this year. If so, it will be the strongest growth of the past three years. As the report’s author, Chris Galbraith, wrote; it will debunk the commentary of “peak gold”.

Looking at the current project pipeline, and without large-scale moves in the gold price or any speculative estimates on additions through exploration activity, SPGMI expects gold output to stay steady until 2022 and decline thereafter. Indeed, more than 15% of gold production by 2024 will be coming from mines that are not yet producing.

More than half of this year’s increase is projected to come from mines that are expected to come on stream in 2019. Examples of those include the Gruyere JV in Western Australia (Gold Fields Ltd and Gold Road Resources Ltd), Meliadine in Nunavut (Agnico Eagle Mines Ltd), Sigma-Lamaque in Quebec (Eldorado Gold Corp.), and the restarted operations at Obuasi in Ghana (AngloGold Ashanti Ltd) and Aurizona in Brazil (Equinox Gold Corp.), both of which have been idle since 2015.

SPGMI notes that the ramp-up at PJSC Polyus’s Natalka operation and commissioning at Nord Gold SE’s Gross mine are significant contributors to a continued increase in Russia’s gold production. The country’s production is expected to equal Australia’s gold output in 2020, and then surpass it. In Canada, the startup of Meliadine and continued ramp-up of Rainy River, Eleonore and Hope Bay, among others, will drive amongst the fastest national growth over the next few years. This year, Canada is projected to pass the US in national gold production to become the fourth-largest gold producing country.

Although SPGMI expects global production to start declining after 2022, not all jurisdictions will have shrinking production. Of the 99 gold-producing countries monitored, 49 are expected to produce less in 2024 compared with 2018, 27 to produce more and 23 are expected to maintain production.

Australia’s production is expected to fall the most. The current second-largest gold producing nation, behind China, is expected to fall to fourth place globally by 2024. The underlying reason for Australia’s fall is the depletion of several long-lived assets, such as St Ives, Paddington, Telfer, Edna May, Southern Cross and Agnew/Lawlers. The expected commissioning of Mt Todd and reactivation of Union Reefs Operations Centre will only partly mitigate the loss from existing operations.

Although Indonesia’s gold production will be substantially lower in 2024 than it was last year, the country’s production in 2018 was anomalously high primarily due to the unusually large output at Grasberg. Peru’s production, however, is clearly trending downward, with Orcopampa, La Zanja and Tambomayo all facing depletion before 2024. With closure only a few years further out, SPGMI notes that Lagunas Norte and Yanacocha will also be producing far less gold in 2024 than they have historically.

Grades are Key

From 2014 through 2018, ore throughput at primary gold mines rose 1.2% but the weighted-average gold grade increased 4.5%. As a result, gold production from primary gold mines increased by 6% during the period.

The increase in grade is projected to continue through 2020 but in 2021 SPGMI expects ore throughput to remain steady and grade to fall by 2% year over year. These two factors are expected to account for around 1.6 Moz in reduced production. By 2024, around 241 Mt less ore is expected to be fed through gold mills compared with 2019, while the gold grade will be almost 2% higher overall. Owing to that drop in throughput, the related drop in production from primary gold mines will be almost 9 Moz.

SPGMI estimates that 11% of global gold production came from polymetallic base metal mines in 2018. Gold production from those mines will fall this year and in 2020 but the share from polymetallic mines is expected to increase gradually thereafter. With falling production from primary gold mines after 2020, and minor increases from polymetallic mines, a growing share of the world’s gold production will come from sources where gold is a byproduct. Less than 10% of the world’s production is expected to come from secondary sources in 2020, but this amount is expected to grow to more than 11% again by 2024.

Reason for Gold M&A

In a separate SPGMI article on April 3, Richard Foy commented that the market capitalisation of gold-mining companies has halved since 2012. This devaluation, and a recent push for consolidation, has increased M&A activity, with majors capitalising on the reduction in enterprise value (EV) in 2018.

Recent M&A deals have reflected this theme as companies look to unlock synergistic cost savings. This has seen gold production remain relatively constant among the top 30 listed gold-mining equities between 2014 and 2018, at about 43 Moz/y, with a 3% increase expected in 2019. The consensus earnings margin outlook of 30% for gold-mining equities is supported by SPGMI’s view on 2019 all-in sustaining cost margins at 33%.

In 2019, the ratio of the EV to EBITDA of the 30 largest gold miners is expected to go below 7.0 for the first time in six years, according to SPGMI. This is the result of a modest decline in EV (due to declining net debt offsetting a rise in market capitalisation) along with an expected increase in earnings. This drop in the ratio could explain the heightened M&A activity among the gold majors.